Your credit report shapes your financial life in South Carolina. Lenders, landlords, and employers all check it before making decisions about you.

At Hays Cauley, P.C., we help people understand South Carolina credit reporting and fix the problems that hold them back. This guide covers what appears on your report, how to spot errors, and what steps to take when something goes wrong.

How Credit Reports Work in South Carolina, Serving South Carolina, Including Greenville, Columbia and Charleston

What Information Actually Appears on Your Credit Report

Your credit report contains four distinct sections that lenders, landlords, and employers review. The first section lists your personal information: name, address, Social Security number, and date of birth. This data comes directly from credit applications you submit. The second section details your credit accounts, including credit cards, mortgages, auto loans, and other debts. For each account, the report shows the creditor’s name, account number, opening date, credit limit or loan amount, current balance, and payment history for the last seven years. The third section reports negative marks like late payments, collections, charge-offs, and bankruptcies. Late payments stay on your report for seven years from the original delinquency date, while bankruptcies can remain for up to ten years. The final section shows inquiries into your credit file. Hard inquiries from lenders or employers appear when you apply for credit and typically stay visible for two years. Soft inquiries from companies checking your report for marketing purposes or your own checks don’t affect your credit score and don’t appear to lenders.

Three Major Bureaus Control Your Credit Data

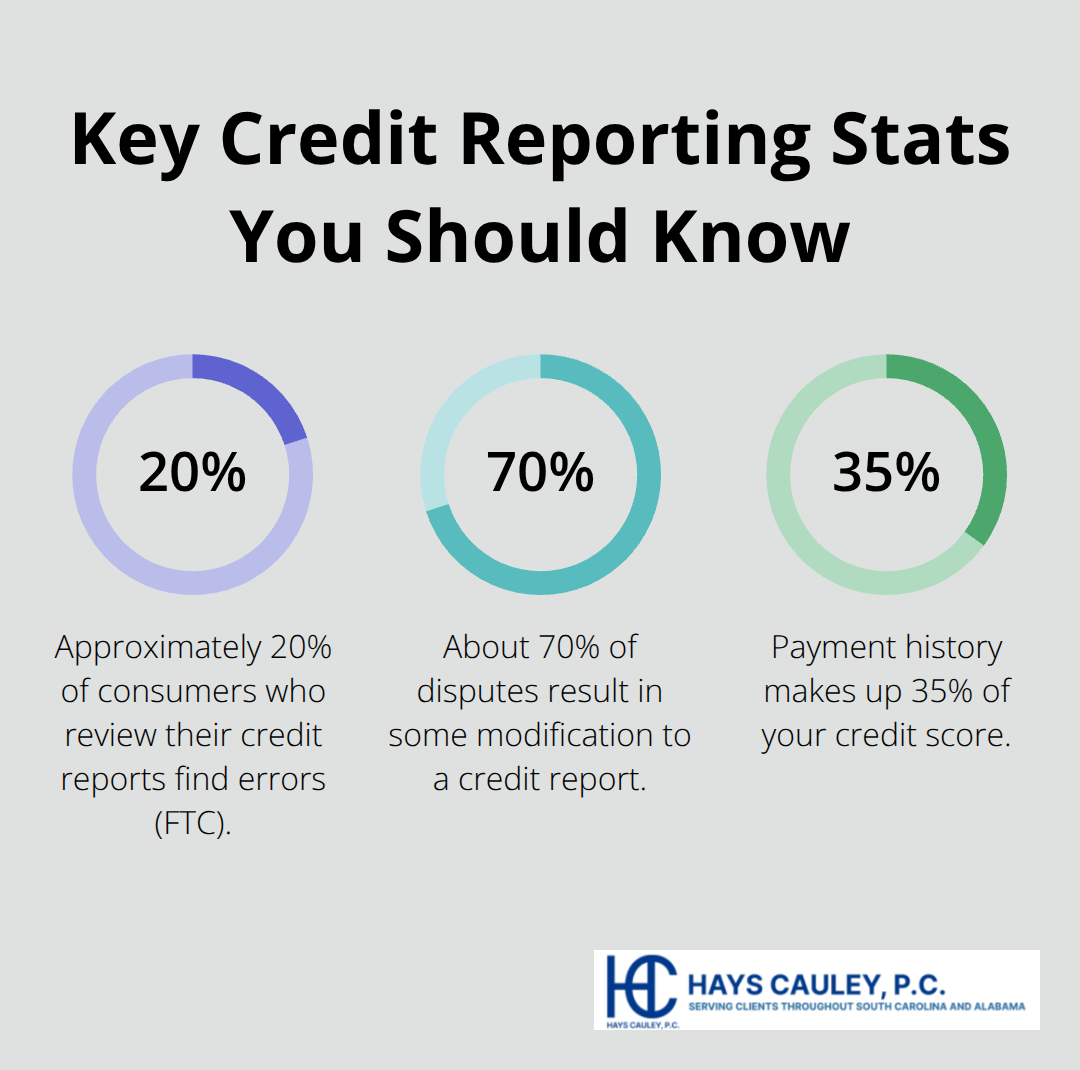

Equifax, Experian, and TransUnion collect, maintain, and report your credit information. These companies gather data from creditors, collection agencies, courts, and public records. They build profiles on millions of consumers and sell credit reports to lenders, landlords, and employers. The Federal Trade Commission reported that approximately 20% of consumers who review their credit reports discover errors on at least one of the three major bureaus. This is why checking all three reports matters.

You can access one free report from each bureau every 12 months through AnnualCreditReport.com, a site authorized by federal law. Many South Carolina residents rotate which bureau they pull every four months to monitor their credit more frequently without paying fees. Each bureau operates independently, meaning errors can appear on one report but not the others. When you dispute an error with one bureau, that correction doesn’t automatically apply to the other two.

Your Legal Rights in South Carolina and Beyond

South Carolina law and the federal Fair Credit Reporting Act give you concrete rights to access, dispute, and correct your credit information. Under Section 609 of the FCRA, you can obtain your free annual reports and see exactly who has accessed your credit file in the last year, or two years for employment inquiries. If a creditor denies you credit, housing, or employment based on your report, they must provide you with a free copy of the report they used. When you dispute inaccurate information, the credit bureau must reinvestigate your claim within 30 days and notify you of the results in writing. If the bureau finds an error, they must correct it and send corrected reports to anyone who received your file in the last six months. South Carolina’s Consumer Protection Code Title 37 reinforces these protections and applies to consumer credit transactions made in the state. If a bureau or furnisher violates your rights, you can sue for actual damages, statutory damages of at least one thousand dollars per violation, and attorney fees. Willful violations can result in treble damages. The statute of limitations for an FCRA lawsuit in South Carolina is two years from discovery or five years from the violation date, whichever comes first.

Now that you understand how your credit report works and what rights protect you, the next step involves recognizing when errors appear on your file and taking action to fix them.

Common Credit Reporting Errors and How to Fix Them, Serving South Carolina, Including Greenville, Columbia and Charleston

Errors Cost You Real Money

Errors on your credit report are common and costly. The Federal Trade Commission found that about one in five consumers discovers an error on at least one of their three credit reports. These mistakes range from simple data entry errors to serious fraudulent accounts opened in your name. A single error can lower your credit score by 50 points or more, which translates directly into higher interest rates on loans and mortgages. For example, moving from a 650 to a 750 credit score on a $200,000 thirty-year mortgage could save approximately $68,000 in interest over the life of the loan.

Types of Errors That Appear on Your Report

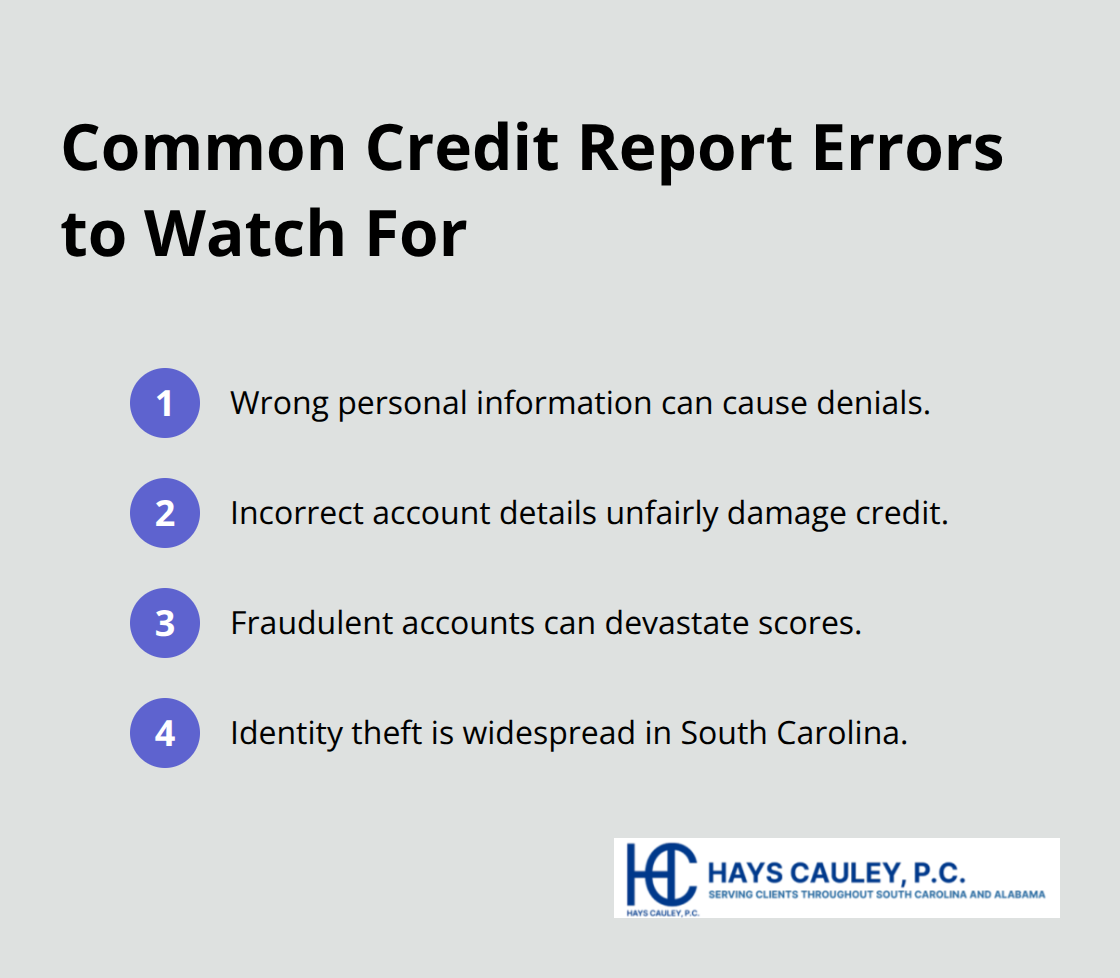

Wrong personal information like an outdated address or misspelled name seems minor until a creditor uses it to deny you housing or employment. Incorrect account details, such as a balance that should be zero or a payment marked late when you paid on time, damage your creditworthiness unfairly. Fraudulent accounts opened by identity thieves are even worse-they tank your score and can trigger collection calls for debts you never incurred.

South Carolina residents reported 18,935 identity theft cases in 2022 according to the Federal Trade Commission, so this threat is real and widespread in your state.

How to Gather Evidence and Build Your Case

The dispute process is straightforward but requires precision and documentation. Start by collecting evidence for each error: bank statements showing you paid on time, creditor correspondence confirming account closure, or a police report if identity theft is involved. Create a separate file for each error to keep your evidence organized. Draft a clear dispute letter for each error, identifying the specific account or item and explaining exactly why it’s wrong. Send your dispute to the credit bureau via certified mail with return receipt requested-this creates a paper trail that protects you legally. The Consumer Financial Protection Bureau offers dispute templates and resources to help you craft effective letters.

What Happens During the Investigation

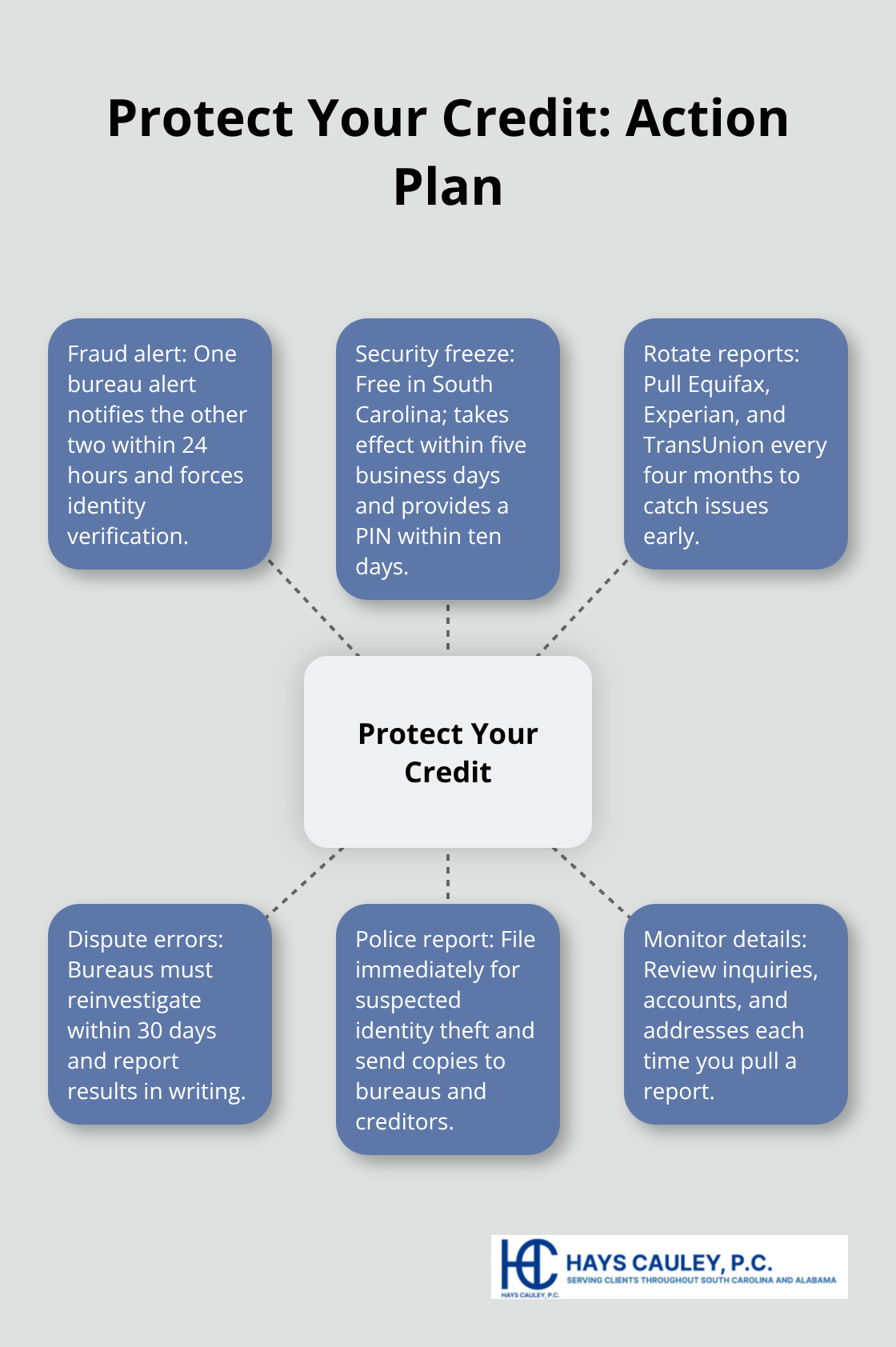

The bureau must investigate within thirty days and notify you in writing of the results. If they find the error, they correct it and send updated reports to anyone who received your file in the last six months. Monitor the investigation closely and request an updated copy of your report after corrections are made to confirm the changes took effect. If the bureau refuses to correct a verified mistake, you can dispute directly with the furnisher (the creditor or lender reporting the information) and, if necessary, pursue legal action under the Fair Credit Reporting Act. About seventy percent of disputes result in some modification to a credit report, though many issues remain unresolved for consumers who don’t follow up aggressively.

When You Need Professional Help

If disputes stall or when bureaus and furnishers refuse to correct clear errors, a consumer protection law firm can help you enforce your credit reporting rights. The statute of limitations for legal action is two years from discovery or five years from the violation date, whichever comes first, so acting promptly preserves your options. Once you understand how to fix errors on your existing report, the next step involves taking action to prevent new problems from appearing in the first place.

Protecting Your Credit in South Carolina, Serving South Carolina, Including Greenville, Columbia and Charleston

Monitor Your Credit Every Four Months

Check your credit reports every four months instead of waiting for the annual free pull. Rotate through Equifax, Experian, and TransUnion every four months to catch errors faster and spot identity theft before damage spreads. Pull one bureau’s report in January, another in May, and the third in September using AnnualCreditReport.com or calling 1-877-322-8228. This approach costs nothing and gives you continuous visibility without paying for monitoring services. When you review each report, look beyond the numbers and scrutinize every account listed, every inquiry, and every address on file. The Federal Trade Commission data shows one in five consumers finds errors, so assume you will too and search methodically.

Act Fast When You Spot Fraud

If you spot unfamiliar accounts or inquiries you didn’t authorize, act immediately by placing a fraud alert with one of the three bureaus, which then notifies the other two within 24 hours. This one phone call restricts access to your credit file and forces creditors to verify your identity before opening new accounts. File a police report the same day you discover potential identity theft, then request a copy from law enforcement to send to credit bureaus and creditors. South Carolina recorded 18,935 identity theft cases in 2022, so this isn’t theoretical risk.

Use a Security Freeze for Maximum Protection

Place a security freeze on your credit file if you want maximum protection, especially if you’re not actively seeking new credit. In South Carolina, placing a freeze is free, takes effect within five business days, and you’ll receive a unique PIN within ten business days. A frozen file stops most fraudulent account openings cold because creditors cannot access your report without your explicit authorization.

Build Credit Strength Through Smart Habits

Payment history drives 35 percent of your credit score, so a single late payment costs you 50 to 100 points depending on your current score. Set up automatic payments for at least the minimum due on every account to eliminate missed deadlines. Keep old accounts open even after you pay them off because account age matters for your score, and closing accounts raises your credit utilization ratio. Try to keep credit card balances below 30 percent of your limits and maintain a mix of account types (credit cards, installment loans, mortgages). If you carry debt, paying down balances faster than minimum payments required accelerates score recovery after errors are corrected. Many South Carolina consumers overlook their reports until applying for a mortgage or car loan, then discover errors that delay approval or cost thousands in higher interest rates. Proactive monitoring and swift dispute action prevent this scenario entirely.

Final Thoughts

Your credit report controls access to mortgages, jobs, and housing in South Carolina. Pull your free reports from all three bureaus today and review them carefully-one in five consumers finds errors worth correcting. If you spot inaccurate information, send a dispute letter via certified mail and track the investigation closely, since most disputes result in some modification to your report and correcting errors can improve your score by 50 points or more.

Place a fraud alert or security freeze if identity theft concerns you, especially after the 18,935 cases reported in South Carolina in 2022. These protections cost nothing and take effect within days, while strong credit habits like paying on time and keeping balances low compound over time. When disputes stall or bureaus refuse to correct clear mistakes, legal action becomes necessary-the statute of limitations for an FCRA lawsuit is two years from discovery, so acting promptly protects your rights.

We at Hays Cauley, P.C. help South Carolina residents enforce their credit reporting rights and recover damages when agencies violate the law. Contact us if you need guidance navigating disputes or pursuing legal remedies for South Carolina credit reporting violations.