Identity theft happens fast, and your response time matters. The first hours after discovering fraudulent activity determine how much damage you’ll face.

We at Hays Cauley, P.C. have helped South Carolina residents recover from identity theft, and we know what works. This guide covers identity theft reporting tips and the concrete steps you need to take immediately.

What To Do Right Now After Identity Theft, Serving South Carolina, including Greenville, Columbia and Charleston.

Report to the Federal Trade Commission First

Stop everything else and report to the Federal Trade Commission immediately. The FTC operates IdentityTheft.gov, a centralized portal where you file your report and receive a personalized recovery plan. This step matters because the FTC aggregates data from millions of reports, helping law enforcement identify patterns and shut down operations. When you report, you create an official record that credit bureaus and financial institutions recognize. More than 1 million people reported identity theft to the FTC last year, and the agency uses this volume to track emerging threats and hold bad actors accountable.

File a Police Report and Contact Your Financial Institutions

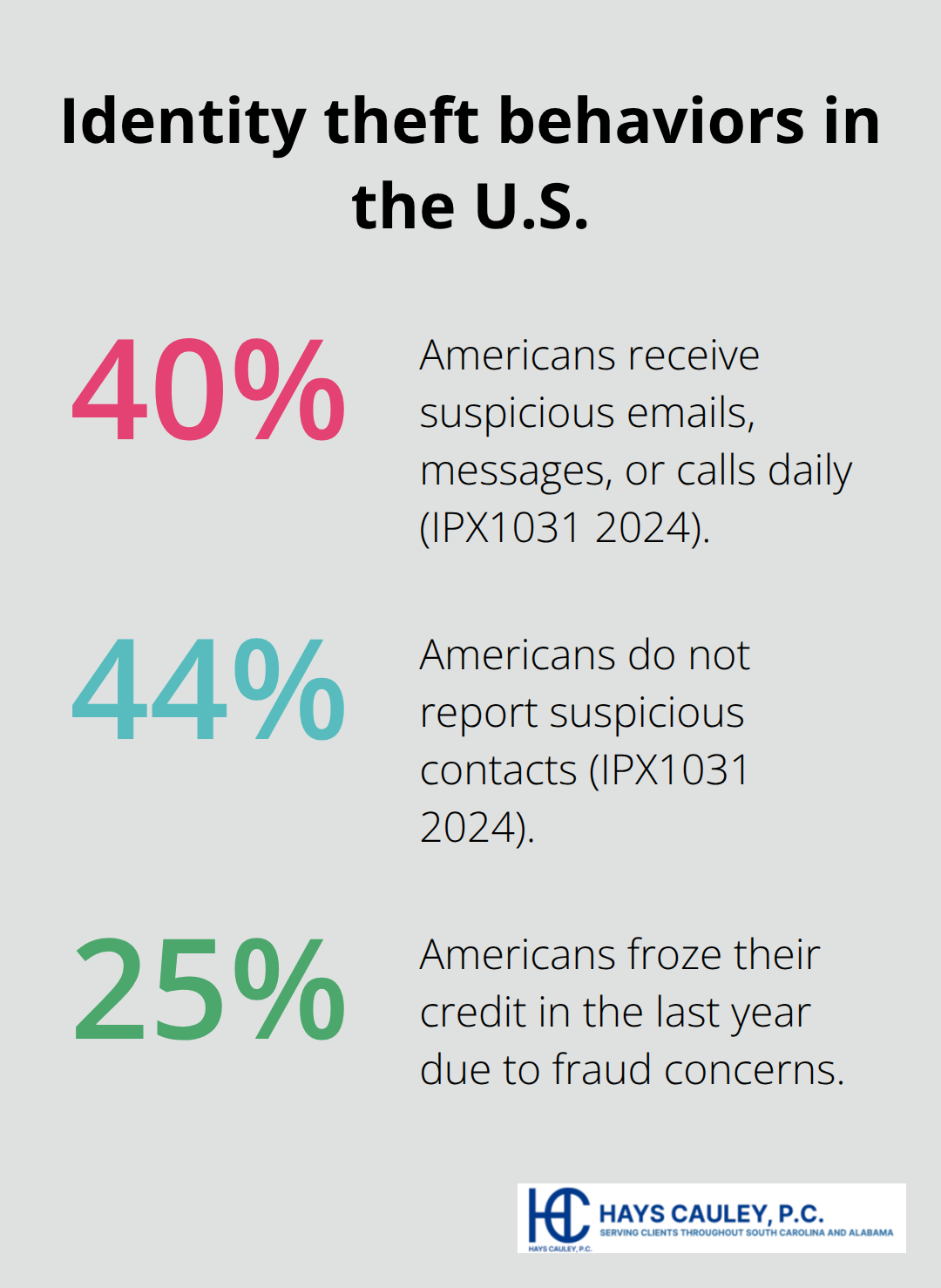

After filing with the FTC, contact your local police department and file a report there as well. Give them your FTC report number and any documentation you have. Police reports create a paper trail that helps when you dispute fraudulent accounts later. Then call your banks and credit card companies immediately, even if you’re still investigating. Tell them you suspect fraud and ask them to freeze your accounts or issue new cards. Most banks can stop transactions within hours. According to the IPX1031 2024 survey, 40 percent of Americans receive suspicious emails, messages, or calls daily, yet 44 percent don’t report them.

Don’t become part of that statistic. Report what you see. Your speed here prevents additional damage because thieves move fast once they gain access to your information.

Place a Fraud Alert and Credit Freeze

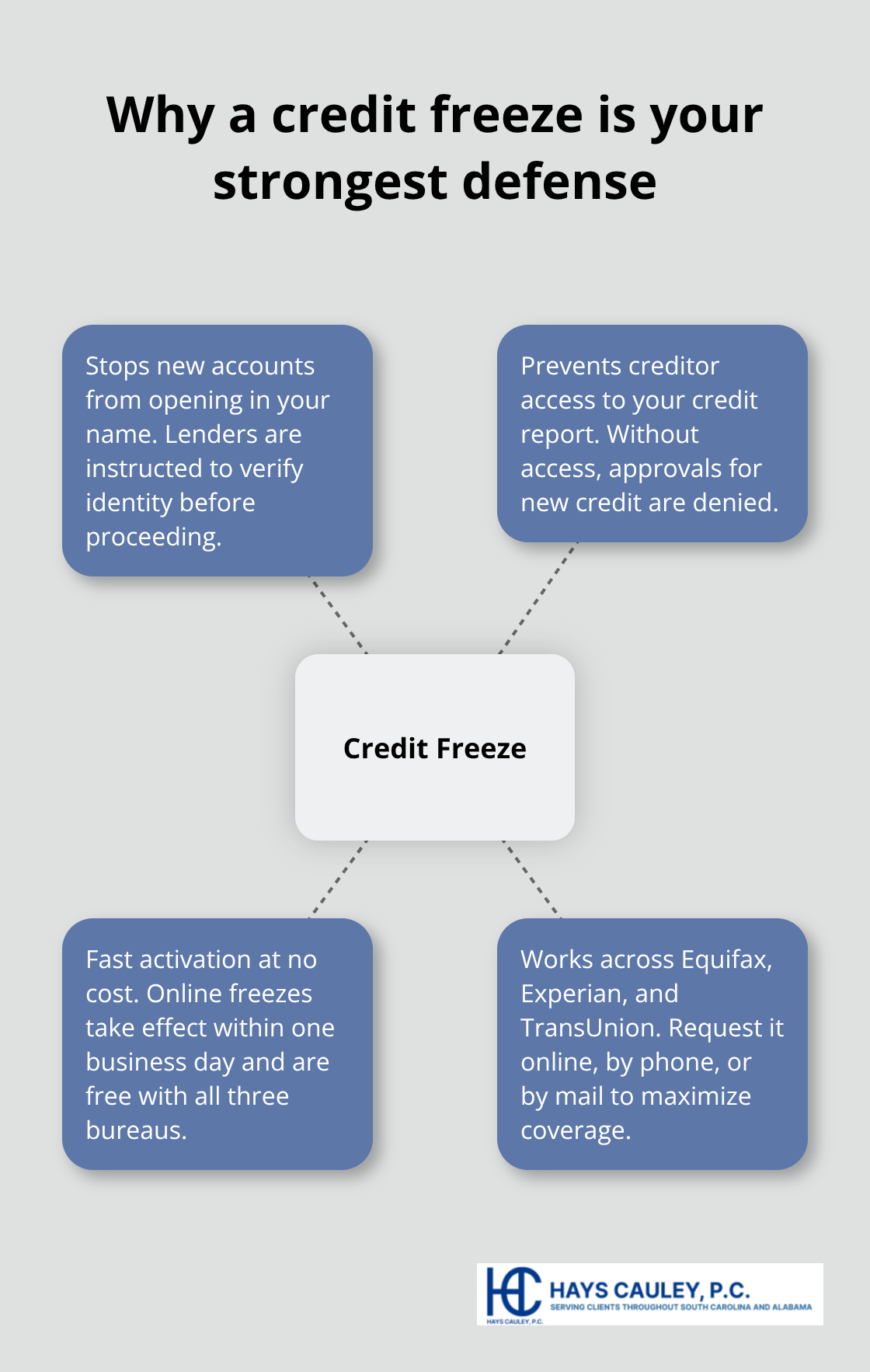

Contact the three major credit bureaus-Equifax, Experian, and TransUnion-and place a fraud alert on your file. A fraud alert tells lenders to verify your identity before opening new accounts in your name. You can do this online, by phone, or by mail. The initial alert lasts one year and is free. After placing the fraud alert, get a credit freeze, which stops credit bureaus from releasing your information to anyone trying to open accounts. About 25 percent of Americans have frozen their credit in the last year due to fraud concerns, according to IPX1031’s data. This step is stronger than a fraud alert because it blocks access entirely.

Protect Your Tax Account and Document Everything

Get an Identity Protection PIN from the IRS to prevent someone from filing taxes in your name. This PIN protects your tax account from unauthorized filings and is one of the most effective defenses against employment-related identity theft. Document everything you do, including dates, times, names of people you speak with, and what they told you. Keep copies of letters, emails, and call logs. This documentation becomes critical if you need to work with a consumer protection attorney later. The more detailed your records, the faster your recovery moves and the stronger your position when disputing fraudulent charges or accounts.

Watch Your Credit and Accounts Like a Hawk

Pull Your Credit Reports Immediately

Start checking your credit reports from Equifax, Experian, and TransUnion within the first week, not months later. You can access one free report from each bureau annually through AnnualCreditReport.com, the only authorized source for free reports. Pull all three at once rather than spacing them out-this gives you a complete snapshot of fraudulent accounts opened in your name. Look for accounts you didn’t open, inquiries from creditors you never contacted, and incorrect personal information. The IPX1031 2024 survey found that about one-third of identity theft victims saw their credit score drop, so speed matters here.

Dispute Fraudulent Activity and Set Up Alerts

Once you spot fraudulent activity, contact the creditor immediately and file a dispute with the credit bureau. Most bureaus process disputes within 30 days, though complex cases take longer. Set up fraud alerts with each bureau after you’ve reviewed your reports-this costs nothing and lasts one year initially. After that year, consider a credit freeze if you’re not actively applying for credit, since 22 percent of Americans don’t know how to freeze their credit, leaving themselves vulnerable to repeat attacks.

Monitor Bank and Credit Card Statements Weekly

Monitor your bank and credit card statements weekly, not just monthly when your bill arrives. Many identity theft victims wait for their statement, missing weeks of fraudulent charges. Log into your accounts online and review transactions as they post. If you spot unfamiliar charges, contact your bank immediately and request a new card or account number. Your bank can reverse fraudulent transactions, but only if you report them promptly. Keep detailed records of every unauthorized charge, including the date, amount, and merchant name.

Document Fraud and Use Official Resources

If the fraud is extensive, ask your bank about placing a temporary hold on your account while you investigate. The South Carolina Department of Consumer Affairs Identity Theft Unit recommends using their step-by-step checklists for specific fraud categories-whether it’s checks, credit cards, or government-issued ID-to guide your response. These resources help you address the exact type of theft you’re facing rather than taking a generic approach. Set phone reminders to review statements on a specific day each week, making this part of your routine rather than an afterthought. Once you’ve stabilized your accounts and documented the damage, you’ll need to understand what legal protections exist and how to pursue them.

Freeze Your Credit and Know When to Call a Consumer Protection Attorney, Serving South Carolina, including Greenville, Columbia and Charleston

Place a Credit Freeze Immediately

A credit freeze stops thieves dead in their tracks because it prevents new accounts from opening in your name. Contact Equifax, Experian, and TransUnion to place a freeze on your credit file. You can do this online, by phone, or by mail, and it costs nothing. The freeze takes effect within one business day for online requests. Once frozen, creditors cannot access your credit report to approve new accounts, which means a thief cannot open credit cards, take out loans, or establish utilities in your name. The FTC found that 25 percent of Americans froze their credit in the last year due to fraud concerns, but many wait too long to take this step.

Place your freeze immediately after discovering identity theft, not weeks later when damage spreads.

Recognize When You Need Legal Help

When fraud is extensive or involves multiple accounts, a consumer protection attorney becomes necessary. If a thief opened accounts in your name, obtained government-issued identification under your identity, or filed taxes using your Social Security number, you need legal guidance to navigate disputes with creditors and credit bureaus. An attorney helps you file disputes correctly, respond to collection notices, and hold creditors accountable if they fail to investigate your claims. The South Carolina Department of Consumer Affairs provides step-by-step checklists for specific fraud categories, but an attorney interprets these resources within your unique situation and ensures you meet critical deadlines.

Build Your Documentation Arsenal

Documentation becomes your strongest weapon throughout recovery. Keep every letter, email, and call log related to identity theft. Record the date, time, person’s name, and what they told you during phone calls. Take screenshots of fraudulent accounts and unauthorized charges. Save copies of your FTC report, police report, and credit freeze confirmation letters. This documentation proves you acted quickly and reported the fraud, which strengthens your position if you dispute charges or need legal representation. Without detailed records, creditors argue they never received your dispute, and credit bureaus claim they have no evidence of fraud. Your documentation forces them to investigate and removes fraudulent accounts from your credit file.

Final Thoughts

The first 24 hours after discovering identity theft determine your recovery timeline and the damage you’ll face. Report to the FTC immediately, file a police report, contact your banks, place a fraud alert, and get an Identity Protection PIN from the IRS. Document everything with dates, names, and details so you create the official records you’ll need later.

Long-term protection requires weekly monitoring of your credit reports and bank statements. Check your accounts every seven days rather than waiting for monthly statements to arrive, and set up fraud alerts with the three credit bureaus. Review your credit reports from Equifax, Experian, and TransUnion at least quarterly during the first year after identity theft so you catch new accounts, inquiries from unfamiliar creditors, and incorrect personal information before secondary fraud attempts escalate.

If fraud is extensive or involves multiple accounts, contact Hays Cauley, P.C. for guidance on your consumer protection rights and options. We help South Carolina residents navigate identity theft recovery and hold creditors accountable when they fail to investigate your claims properly. Our team applies identity theft reporting tips to your specific situation and fights to restore your financial standing.