A mistake on your credit report can tank your score and cost you thousands in higher interest rates. Yet millions of Americans have errors on their reports right now, many without realizing it.

The good news: you can dispute credit report errors and get them removed. We at Hays Cauley, P.C. help people fight back against inaccuracies every day, and this guide walks you through exactly how to do it.

Common Credit Report Errors and Why They Matter

Identity Errors Signal Serious Problems

A misspelled name, wrong address, or incorrect phone number might seem minor, but these identity errors signal that the bureau has confused your file with someone else’s. The consequences extend far beyond embarrassment-lenders pull your report and see accounts that don’t belong to you, making approval decisions based on false information. These errors happen frequently because credit bureaus process millions of records daily with minimal human oversight, relying on automated systems that flag discrepancies poorly.

Duplicate Accounts and Mixed Files

Duplicate accounts represent another common problem where the same debt appears twice under slightly different names or account numbers, artificially tanking your score. Mixed files occur when accounts belonging to someone with a similar name get merged into your report-a problem serious enough that the Consumer Financial Protection Bureau recognizes it as warranting fraud-alert procedures. One in five consumers discovered errors on their credit reports, with roughly half of those errors serious enough to affect lending decisions.

Other Frequent Errors That Damage Your Score

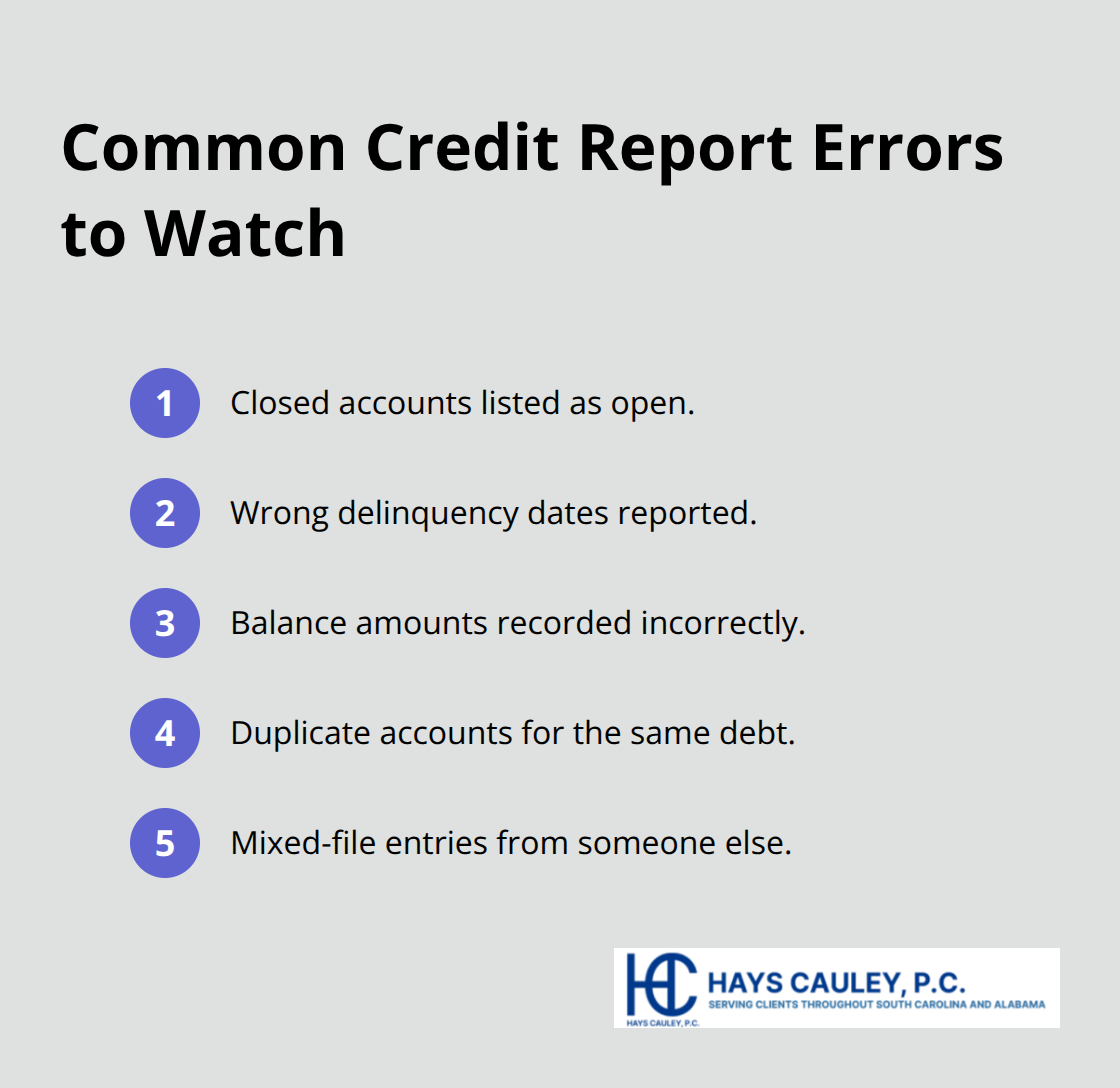

Closed accounts incorrectly listed as open, delinquency dates recorded wrong, and balance errors also plague credit reports regularly. A furnisher might report a payment as late when it arrived on time, or fail to update a closed account. The system assumes accuracy until proven wrong, which means your credit score takes the hit first and correction comes later, if at all.

The Financial Impact of Inaction

A single error can cost you thousands in higher interest rates or rejection from credit applications altogether. Missing a mortgage approval because of a debt that isn’t actually yours represents a tangible, life-altering consequence. The Fair Credit Reporting Act protects you with the right to dispute, but that protection only works if you act on it. The Fair Credit Reporting Act requires furnishers-banks, credit card companies, landlords-to investigate disputed information within 30 days, yet many errors persist because consumers never challenge them.

Why Speed Matters

Starting your dispute immediately after spotting an error gives you the advantage of the 30-day investigation window that the Fair Credit Reporting Act mandates, preventing months of damage to your financial standing. The longer an error sits on your report, the more it compounds through missed opportunities and higher borrowing costs. Now that you understand what errors look like and why they hurt, the next step involves pulling your actual credit report and identifying which inaccuracies affect you.

How to Pull Your Report and File a Dispute That Works

Access Your Credit Report From All Three Bureaus

Visit annualcreditreport.com-the only official source mandated by federal law-to access your credit report from Experian, Equifax, and TransUnion. Each bureau maintains separate files, and errors appear on one, two, or all three depending on which furnisher reported the information. Pull your reports and circle every inaccuracy, noting the exact account number and the specific error. Common mistakes include closed accounts listed as open, wrong delinquency dates, balances that don’t match your records, and accounts belonging to someone else entirely. Write down what’s wrong and why before you file anything.

Identify Exactly What Needs Correction

Take time to compare your actual account statements against what the bureaus report. Look for closed accounts that still show as active, delinquency dates that don’t align with your payment history, balance amounts that differ from your records, and accounts you never opened. The more specific you are about the error, the faster the investigation moves. Vague disputes get ignored or dismissed, while precise ones force action.

File Disputes With Both the Bureau and the Furnisher

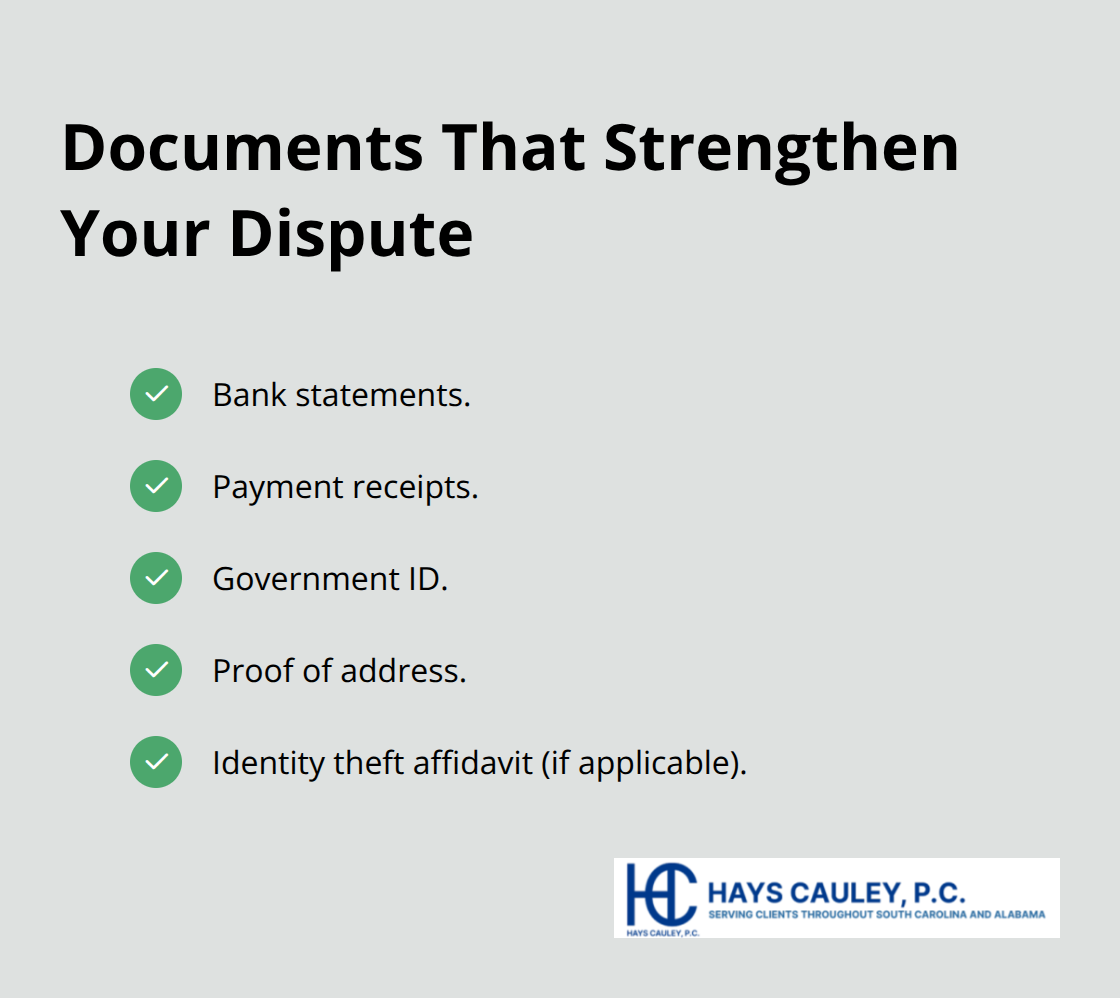

Send your dispute to the credit reporting company through their online portal if speed matters, or mail a certified letter if you want a paper trail. Online disputes through Experian take under ten minutes, though mailing creates documented proof that holds weight later if you need to escalate. Include copies of supporting documents that prove the error: bank statements, payment receipts, government ID, proof of address, or identity theft affidavits if the account isn’t yours. Keep your written dispute statement under 150 words and reference the specific line item number from your report.

After filing with the bureau, send a separate dispute letter to the furnisher using certified mail within the same week, again keeping it concise and document-heavy. The furnisher has 30 days to investigate and report back to the bureau, so track your submission dates carefully and note the confirmation numbers.

Monitor Your Dispute Status and Push for Resolution

Check your dispute status daily through the bureau’s portal and call the bureau directly if you haven’t received acknowledgment within five business days. Experian’s phone line is 888-397-3742, Equifax is 866-349-5191, and TransUnion is 800-916-8800. Mark your calendar for 30 days after filing to send a follow-up letter if the dispute remains unresolved, pushing the bureau to complete their investigation on time. The Fair Credit Reporting Act’s 30-day timeline is your legal weapon here, and staying on top of deadlines forces action rather than passive delays.

What happens next depends on how the bureau and furnisher respond to your dispute-and what you should do if they deny your claim.

What Happens After You File a Dispute

The 30-Day Investigation Timeline Starts Immediately

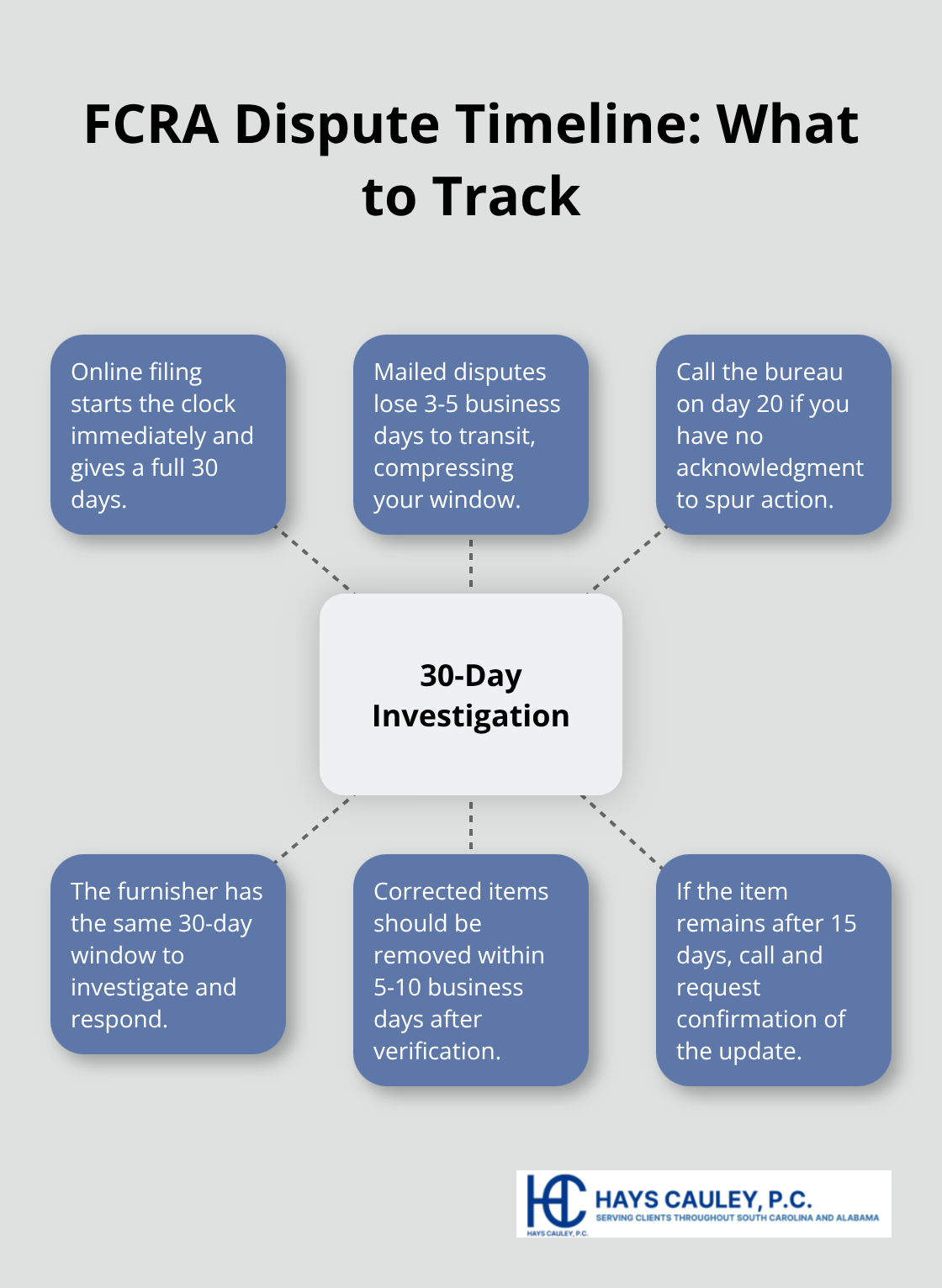

The 30-day investigation period mandated by the Fair Credit Reporting Act starts the moment the credit bureau receives your dispute, not when you file it. This distinction matters because mailed disputes take 3-5 business days to arrive, which eats into your timeline. If you filed online through Experian, Equifax, or TransUnion, the clock starts immediately, giving you a genuine 30-day window. If you mailed your dispute, those transit days compress your actual investigation period, so tracking your submission date and the bureau’s acknowledgment date becomes critical.

Push the Bureau to Act Within the Legal Deadline

The bureau must investigate within 30 days and report results back to you in writing, but many bureaus operate on the assumption that consumers won’t follow up, meaning your dispute sits in a queue until you push. Call the bureau on day 20 if you haven’t received an acknowledgment, using the phone numbers from your dispute confirmation. This single call often accelerates processing because it signals you’re monitoring the timeline.

The bureau contacts the furnisher with your dispute details, and the furnisher has the same 30-day window to investigate and respond. If the furnisher verifies the information is accurate, the bureau reports back that the item remains on your report. If the furnisher cannot verify the information or determines it was reported incorrectly, they must notify the bureau immediately, and the bureau removes or corrects the item within a few business days.

Respond Immediately if the Bureau Denies Your Dispute

When a bureau denies your dispute and keeps the item on your report, your response determines whether the error stays permanent or gets removed. Do not accept the denial as final. Instead, file a complaint with the Consumer Financial Protection Bureau immediately, which creates an official record and forces the bureau to respond to a government agency. The CFPB takes complaints seriously because violations of the Fair Credit Reporting Act carry significant penalties, and the bureau knows this. Include your dispute documentation, the bureau’s denial letter, and a clear explanation of why their investigation was insufficient.

Simultaneously, contact the furnisher directly and request written confirmation that they verified the information as accurate. Many furnishers rubber-stamp verifications without actually investigating, and a direct call asking specific questions about their verification process sometimes reveals they never conducted one. If the furnisher admits they didn’t investigate properly, file a second dispute immediately with updated documentation showing their failure.

Handle Identity Theft and Mixed-File Disputes as Fraud Cases

For identity theft or mixed-file situations where accounts genuinely don’t belong to you, file an identity theft report through IdentityTheft.gov and attach that report to your CFPB complaint. This escalates the case from a simple dispute to a fraud matter, which receives higher priority. The fraud designation forces both the bureau and furnisher to treat your claim with greater urgency than standard disputes.

Monitor Progress and Document Everything

Monitor your credit reports weekly after filing a dispute by logging into each bureau’s portal or pulling updated reports through annualcreditreport.com every 30 days. Corrected items should disappear within 5-10 business days after the furnisher notifies the bureau. If the item remains after 15 days, call the bureau again and request confirmation that they received the furnisher’s correction notice.

Document every call with the date, time, name of the representative, and what they said. This activity log becomes your evidence if you need to escalate to small claims court or file a complaint with your state attorney general. Keep copies of every letter, email, and confirmation number. Persistent errors sometimes require legal intervention to force removal, and we at Hays Cauley, P.C. handle disputes that bureaus wrongly deny.

Final Thoughts

Most errors get corrected through the standard dispute process when you follow the steps outlined in this guide. However, some bureaus and furnishers ignore disputes, deny them without proper investigation, or fail to update corrections after verification. When persistence alone doesn’t work, you need legal support to force compliance with the Fair Credit Reporting Act.

We at Hays Cauley, P.C. handle credit reporting disputes that bureaus wrongly deny or ignore. Our team works with consumers who face persistent errors, identity theft complications, or furnishers that refuse to investigate properly. If you’ve filed disputes and hit a wall, contact us to discuss your options.

We’re dedicated to helping consumers dispute credit report errors, identity theft cases, and debt-related issues. We know how to push back against bureaus that violate the Fair Credit Reporting Act and furnishers that fail their legal obligations. Reach out today if standard disputes haven’t worked for you.