Your credit report shapes your financial life, yet errors on it happen more often than you’d think. At Hays Cauley, P.C., we help South Carolina residents understand their FCRA accuracy rights and fight back against mistakes that damage their credit scores.

Inaccurate accounts, wrong payment histories, and duplicate entries can tank your creditworthiness. This guide walks you through your legal rights, how to dispute errors, and what credit bureaus must do to fix them.

What the FCRA Actually Requires from Credit Bureaus

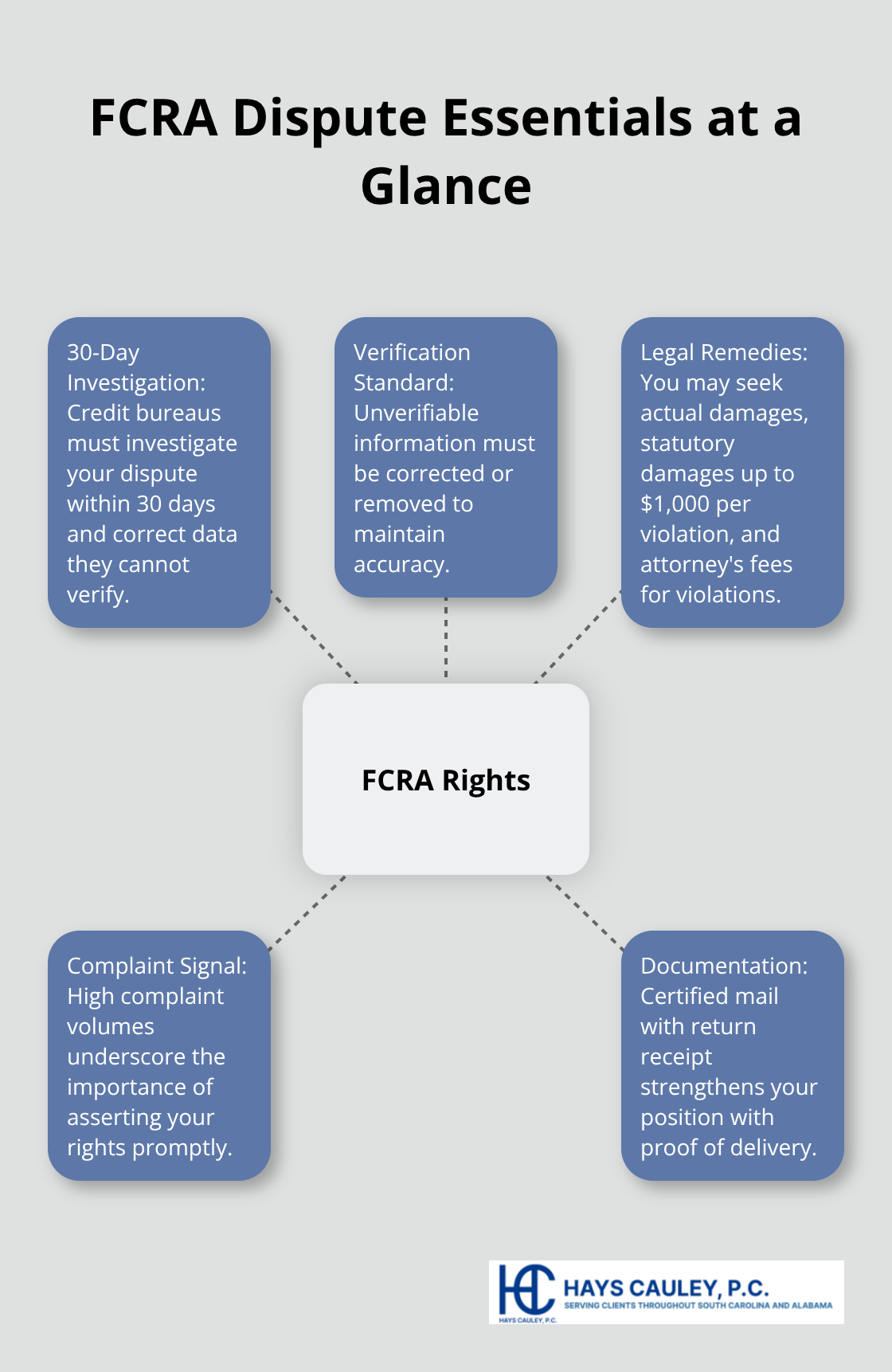

The Fair Credit Reporting Act gives you specific legal weapons to fight inaccurate credit report entries. The law isn’t vague or theoretical-it mandates that credit bureaus must investigate your disputes within 30 days and correct any information they cannot verify. This isn’t a suggestion.

If a bureau fails to investigate properly or ignores your dispute, you can sue for actual damages, statutory damages up to $1,000 per violation, and attorney’s fees. The FTC reported over 175,000 complaints about credit reporting in 2020, which shows how widespread these problems are and how seriously you should take your rights.

Your Dispute Rights Are Stronger Than Most People Think

You can dispute errors directly with the credit bureau or with the furnisher-the creditor or lender who reported the information. The FCRA requires furnishers to investigate your dispute within 30 days and notify the credit bureaus of any corrections. About 1 in 5 consumers finds an error on at least one of their three credit reports from Equifax, Experian, or TransUnion. You’re entitled to one free credit report annually from each bureau through AnnualCreditReport.com. Once you spot an error, the clock starts ticking. You have up to two years from discovery or five years from the violation date to file a lawsuit if the bureaus fail to correct verified errors. Acting quickly matters because delays weaken your position and allow inaccurate information to keep damaging your score.

Documentation and Proof Make the Difference

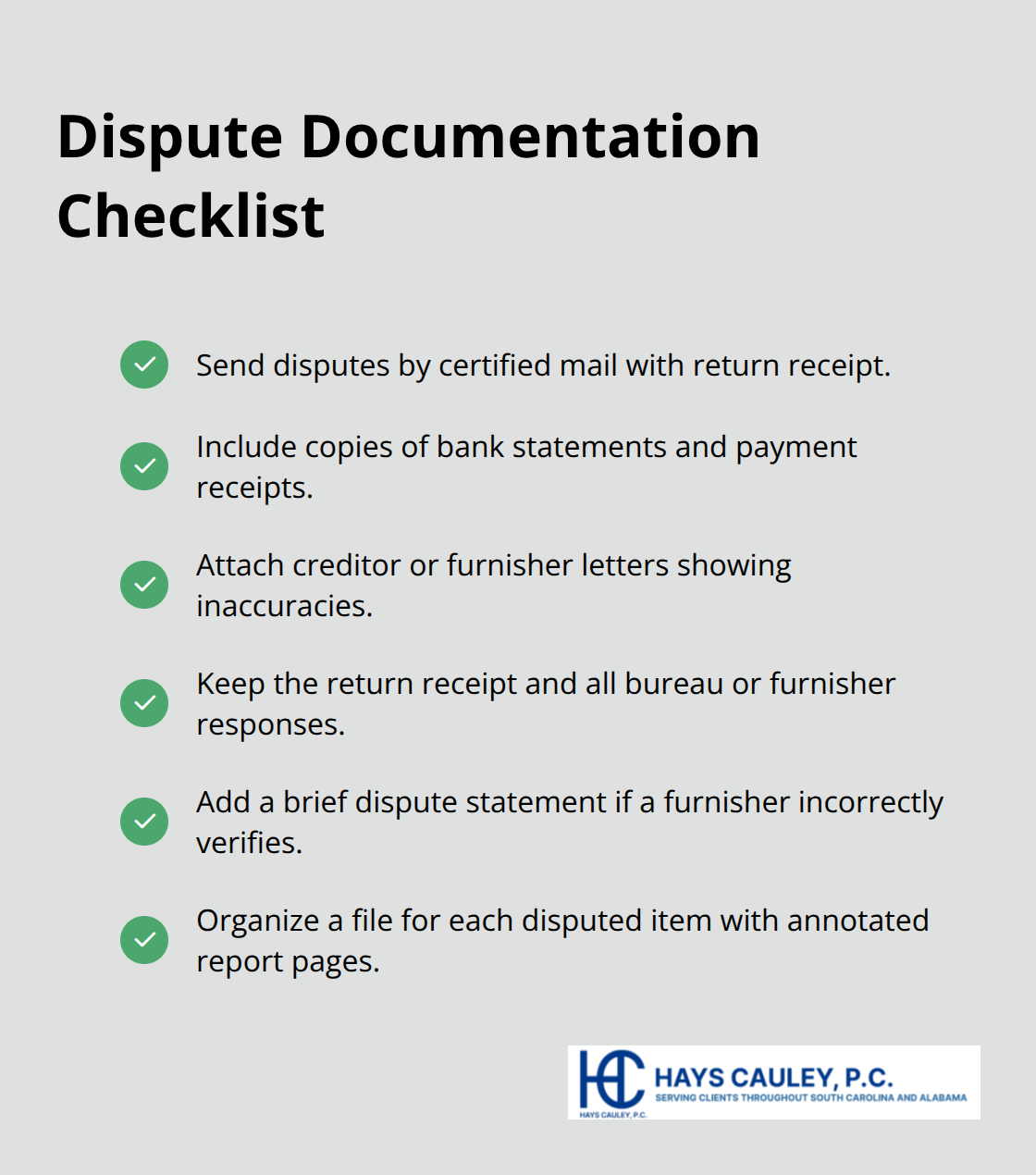

When you file a dispute, you must provide clear evidence of why the information is wrong. Send your dispute by certified mail with return receipt so you have proof the bureau received it. Include copies of supporting documents (bank statements, payment receipts, creditor letters) that show the entry is inaccurate. Furnishers sometimes claim they verified information correctly when they actually conducted no real investigation. If a furnisher verifies information as accurate but you believe it’s still wrong, you can add a brief dispute statement to your file that lenders will see. The South Carolina Consumer Protection Code requires that credit practices be fair and that consumers understand their credit terms.

When Bureaus Refuse to Correct Verified Errors

If a bureau refuses to correct information you’ve proven inaccurate, you have legal recourse. The FCRA allows you to pursue damages against furnishers and credit reporting agencies that violate your rights. A consumer protection law firm can help you navigate these complex disputes and hold bureaus accountable. The next section covers the specific errors that appear most frequently on credit reports and how to identify them.

Common Credit Report Errors That Cost You Money, Serving South Carolina, Including Greenville, Columbia, and Charleston

Unfamiliar Accounts on Your Report

Unfamiliar accounts appearing on your credit report rank among the most damaging errors you’ll encounter. These range from accounts opened fraudulently in your name to legitimate accounts reported under the wrong person’s file due to identity mix-ups or furnisher mistakes. When you spot an account you never opened, pull the account details and contact the furnisher directly in writing. Request that they verify the account is actually yours and demand removal if they cannot provide proof you authorized it. The FTC found that about 1 in 5 consumers discovers at least one error across their three bureau reports, and unfamiliar accounts represent a significant portion of these disputes. Do not wait to challenge these entries because they damage your credit score immediately and stay on your report for seven years unless removed.

Incorrect Payment Histories and Late Payment Marks

Incorrect payment histories cause equal damage but are often easier to prove wrong. Late payment marks, missed payment claims, and wrong balance amounts frequently appear because furnishers fail to update information correctly or report old data repeatedly. Gather your bank statements and payment receipts showing when you actually paid, then dispute both the credit bureau and the furnisher who reported the false information. These documents establish a clear paper trail that contradicts what the bureaus claim. Furnishers sometimes resist correction even when your evidence is solid, which is why sending disputes by certified mail with return receipt matters-you need proof they received your challenge.

Duplicate Accounts and Reporting Errors

Duplicate accounts represent another widespread problem where the same debt appears multiple times under slightly different account numbers or creditor names. This artificially tanks your credit utilization ratio and makes your financial situation look worse than reality. Request that the bureaus investigate and remove the duplicates, and provide documentation showing the accounts are identical. When you file disputes over these three error types, send everything by certified mail with return receipt requested to establish proof of delivery. Include copies of your credit report pages with the disputed items circled, your supporting documents, and a clear letter explaining why each entry is inaccurate.

What Happens After You File Your Dispute

The bureaus must investigate within 30 days and correct verified errors or face potential liability. If a furnisher claims to have verified information that you know is false, document this response because it strengthens your case if you eventually need legal action. South Carolina residents can pursue actual damages, statutory damages up to $1,000 per violation, and attorney’s fees through the courts when bureaus or furnishers violate your FCRA rights. The next chapter covers the practical steps to file disputes and what to do when agencies ignore your requests.

How to Dispute Errors on Your Credit Report, Serving South Carolina, Including Greenville, Columbia, and Charleston

Write a Clear Dispute Letter

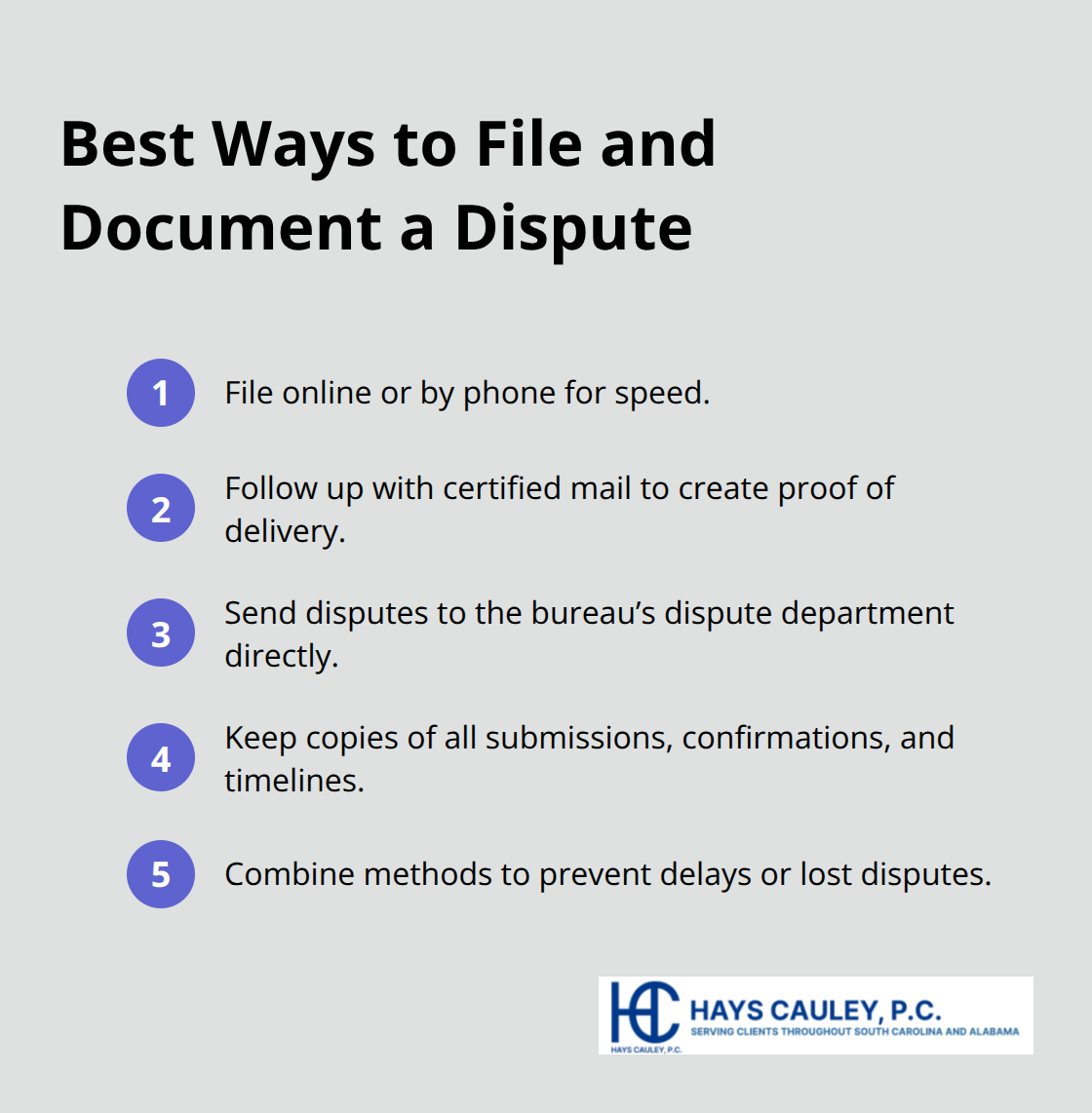

Start your dispute with a letter to the credit bureau that identifies the exact item you’re challenging and explains why it’s inaccurate. Send this letter via certified mail with return receipt requested-this step matters because it creates proof the bureau received your dispute on a specific date. Include a copy of your credit report with the disputed item circled or highlighted, copies of supporting documents like bank statements or payment receipts, and your full name, address, phone number, and the confirmation number from your credit report if available. The CFPB provides dispute letter templates you can use as a model, which saves time and ensures you include all necessary information. Mail your dispute to the credit bureau’s dispute department, not their general mailing address, since disputes routed to the wrong department get delayed.

Choose Your Filing Method

You can file disputes online, by phone, or by certified mail with Equifax, Experian, or TransUnion. Certified mail creates the clearest documentation trail if the bureau later claims they never received your challenge. Online and phone filing offer speed, but they don’t provide the same proof of delivery that certified mail does.

Most consumers benefit from combining methods-file online or by phone for speed, then follow up with certified mail to establish a paper trail. This dual approach protects you if disputes get lost or mishandled.

Dispute Directly with the Furnisher

Simultaneously dispute with the furnisher-the creditor or lender who reported the inaccurate information. Send them a written dispute using their specified mailing address, which you can find on your credit report or the company’s website. Furnishers have 30 days to investigate and must correct or remove information they cannot verify, then notify the credit bureaus of any changes. If a furnisher ignores your dispute or claims to have verified information you know is false, document their response in writing and keep it with your file.

Verify Corrections Were Actually Made

When the credit bureau updates your report following a correction, request an updated copy to confirm the error was actually removed-don’t assume it was fixed. If the bureau refuses to correct a verified error after 30 days, add a brief statement to your file explaining your side of the dispute, which lenders will see alongside your report. File a complaint with the CFPB if bureaus or furnishers fail to investigate properly. If corrections aren’t made or if you need to pursue legal action for damages, contact a consumer protection attorney who can evaluate your case and explain your options under the FCRA.

Final Thoughts on Protecting Your Credit Report

Your credit report won’t fix itself, and credit bureaus won’t voluntarily correct errors without pressure. Check your reports from Equifax, Experian, and TransUnion every four months by rotating through one bureau at a time using AnnualCreditReport.com, which catches errors faster than waiting a full year between checks. When you spot inaccurate information, file disputes immediately with both the bureau and the furnisher, document everything in writing, send by certified mail, and keep copies of all correspondence. The FCRA gives you legal teeth to enforce accuracy, but only if you act within the two-year discovery window or five-year violation window to pursue damages.

Violations by credit bureaus and furnishers carry real consequences under federal law. You can recover actual damages reflecting the harm to your credit score and finances, statutory damages up to $1,000 per violation, and attorney’s fees (with punitive damages possible for willful noncompliance). If a bureau refuses to correct a verified error after 30 days, or if a furnisher falsely claims to have verified inaccurate information, you have grounds for legal action. Many South Carolina residents underestimate their FCRA accuracy rights and accept incorrect reports without challenge, which proves costly.

If you’ve disputed errors without success, or if you need guidance on whether your situation warrants legal action, contact Hays Cauley, P.C. to discuss your options. Your credit report determines your financial opportunities, and inaccurate information shouldn’t control your future.