Credit reporting errors can devastate your financial life, but many people don’t know they have legal protections under the Fair Credit Reporting Act. Understanding FCRA investigation steps helps you recognize when violations occur and what remedies you can pursue.

At Hays Cauley, P.C., we’ve guided countless South Carolina consumers through this process. This guide walks you through how investigations unfold, from the initial complaint through settlement and credit report corrections.

How Your FCRA Investigation Starts

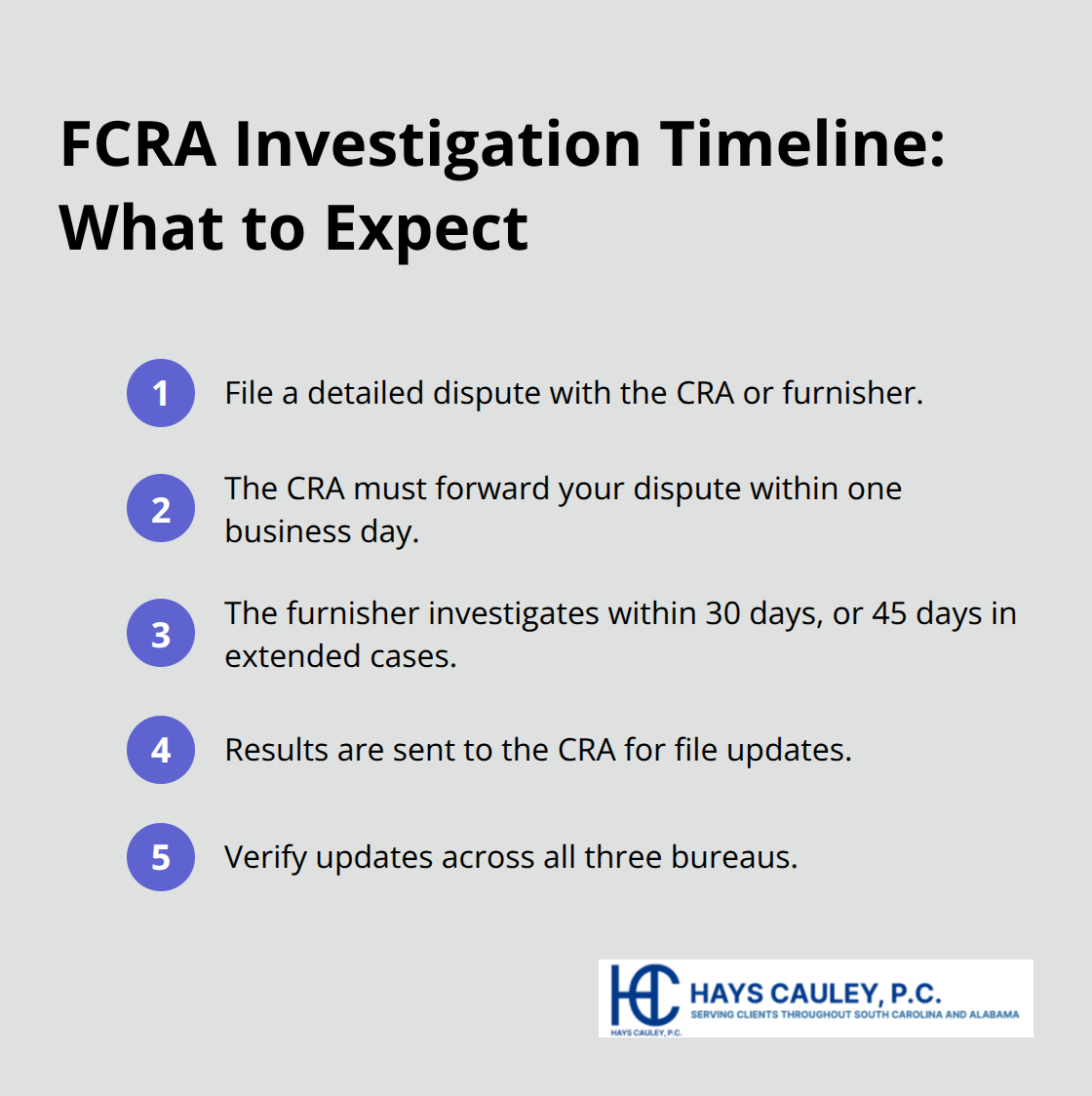

Starting an FCRA investigation means filing a formal dispute with the credit reporting agency or the furnisher directly. You need to be specific about what’s wrong. Instead of saying an account is inaccurate, identify the exact item-the balance, the payment status, the account number-and explain why it’s wrong. Include supporting documents like bank statements, payment receipts, or creditor letters showing the error. The Consumer Financial Protection Bureau found that about 1 in 5 credit reports contain errors, so concrete evidence matters more than a vague complaint. When you file with a credit reporting agency, they must send your dispute to the furnisher within one business day. If you file directly with the furnisher, send your dispute to their specific address or method listed on their website or statements. The furnisher then has 30 days to investigate, or 45 days if you filed after receiving your free annual credit report and submitted additional information during the investigation window.

What Happens After You File

Once the furnisher receives your dispute, they must review all information you provided and search their records for the account. They cannot simply assume the information is correct-they must actually investigate. If they cannot locate sufficient information or determine the account details within their system, they contact you for clarification. The furnisher must complete their investigation and report results back to the credit reporting agency before the 30-day deadline expires. If they find the information inaccurate or incomplete, they must notify all credit reporting agencies that received the incorrect data so corrections spread across all three major bureaus. If the furnisher confirms accuracy after their investigation, the item stays on your report, though the agency may add a notation that the information meets FCRA requirements. This process is not optional-furnishers who ignore disputes or fail to investigate within the legal timeframe violate federal law and expose themselves to CFPB enforcement and consumer lawsuits with penalties reaching up to $4,983 per violation according to current inflation adjustments.

Why Documentation Strength Determines Outcomes

The quality of your supporting evidence directly affects investigation speed and accuracy. Vague disputes receive different treatment than specific ones backed by documents. A bank statement showing you made a payment on a date the furnisher claims you missed it carries weight. A court judgment proving identity theft forces the furnisher to remove fraudulent accounts from your file. A creditor letter admitting they made an error proves far more persuasive than your word alone. Furnishers must apply reasonable procedures to verify information before reporting it, which means they should catch their own errors during investigation if you point them out clearly.

Building Your Evidence Strategy

Strong documentation transforms how furnishers handle your dispute. Concrete documents-bank statements, payment receipts, creditor letters, court orders-create a clear record that furnishers cannot ignore. Dates and amounts should directly connect to the disputed item so the furnisher understands exactly what you challenge. Identity theft cases require additional documentation (police reports, fraud affidavits) that forces furnishers to take immediate action. Weak evidence (vague complaints without specifics) allows furnishers to dismiss disputes quickly and move forward without real investigation. The furnisher’s obligation to investigate reasonably means they must examine what you provide and verify their own records match what they reported.

Moving Forward With Your Investigation

After you file your dispute with proper documentation, the investigation clock starts. The furnisher’s 30-day window (or 45 days in extended cases) determines how quickly you receive results. You should track your dispute confirmation number and follow up if you don’t hear back within the timeframe. Once the furnisher completes their investigation, they report findings to the credit reporting agency, which then updates your file. If corrections occur, your credit report reflects the changes across all three major bureaus. Understanding what happens next-how outcomes unfold and what remedies apply-shapes your path forward when errors persist or violations occur.

What Evidence Furnishers Actually Review During Investigations – Serving South Carolina, including Greenville, Columbia and Charleston

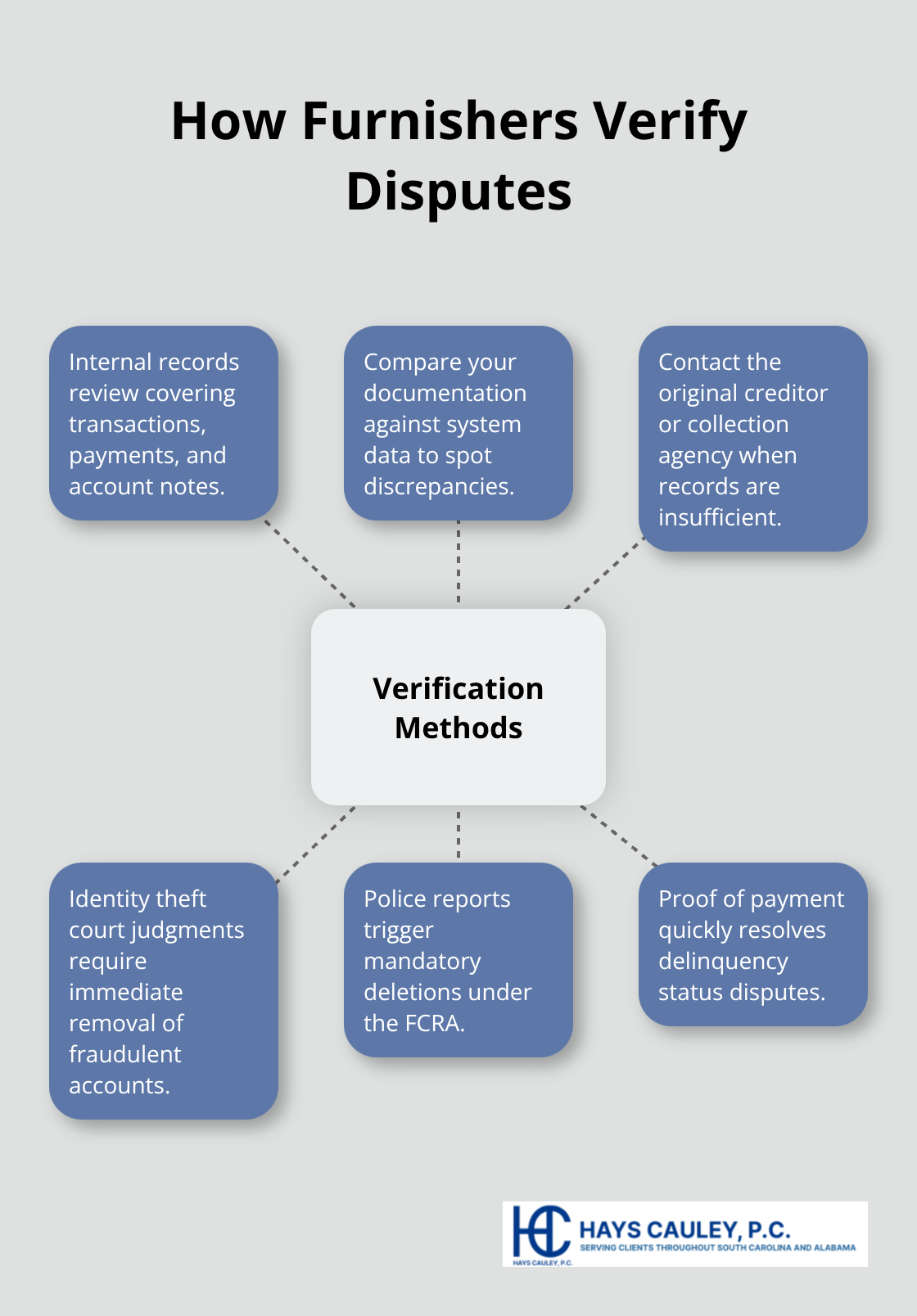

When a furnisher investigates your dispute, they don’t conduct a thorough audit of their entire system. They pull your specific account file and cross-check it against what they reported to the credit reporting agency. The investigation focuses narrowly on whether the disputed item matches their records. If you claim a balance is wrong, they verify the current balance in their system. If you dispute a payment status, they examine their payment ledger for that account.

Your Supporting Documentation Drives Their Investigation Scope

Your supporting documentation must directly address what furnishers can verify. A bank statement showing you made a payment on July 15 forces them to check their records for that same date. A creditor letter admitting they misreported the account status creates a document they cannot ignore during their investigation. The furnisher must apply reasonable procedures to verify accuracy, which the Consumer Financial Protection Bureau interprets as requiring them to actually examine the evidence you provide and compare it to their own records. Furnishers cannot simply rubber-stamp their original report as correct without reviewing what you submitted. Courts have found violations when furnishers conducted investigations so cursory that they clearly didn’t review dispute materials. Your evidence creates the foundation for what they investigate, so weak documentation leads to weak investigations.

How Furnishers Verify Your Claims

Furnishers typically use three verification methods during investigation. First, they search their internal systems for the account and review transaction history, payment records, and account status notes. Second, they compare your dispute materials against what their system shows to identify discrepancies. Third, if they cannot locate sufficient information or if your evidence contradicts their records significantly, they contact the original creditor or collection agency to verify the account details.

This third step matters because furnishers sometimes report information they received from another source without fully verifying it themselves. If a debt collector sold an account to a furnisher, the furnisher may need to contact the original creditor to confirm details. Your evidence expedites this process dramatically. A court judgment proving identity theft eliminates the need for further verification because the furnisher must remove fraudulent accounts immediately. Police reports documenting identity theft trigger mandatory account removal under FCRA rules. Proof of payment stops disputes about delinquency status cold.

What Happens When Furnishers Find Errors

When a furnisher discovers their reported information was inaccurate during investigation, they must notify all credit reporting agencies that received the wrong data. This correction duty applies to every bureau they reported to, not just the one where you filed your dispute. The furnisher must provide corrected information and instruct the bureaus to update or remove the inaccurate item. If they reported the wrong account balance, they provide the correct balance. If they reported a fraudulent account due to identity theft, they instruct the bureaus to delete it entirely. The furnisher cannot selectively correct information at one bureau while leaving inaccurate data at another. Federal law requires consistent reporting across all three major bureaus.

Verifying Corrections Across All Three Bureaus

The correction process typically takes fifteen to thirty days after the furnisher completes their investigation. You should verify that all three bureaus updated your file by pulling fresh credit reports after the investigation concludes. The CFPB found that corrections sometimes fail to propagate to all bureaus, which is why you need to confirm the fix yourself. If one bureau still shows the old inaccurate information after the furnisher sent corrections, contact that bureau directly with proof of the correction notice from the furnisher. Once furnishers complete their investigations and corrections spread across your credit file, the outcomes of those investigations determine what happens next-whether items remain on your report, get corrected, or disappear entirely.

What You Can Actually Recover From FCRA Violations – Serving South Carolina, including Greenville, Columbia and Charleston

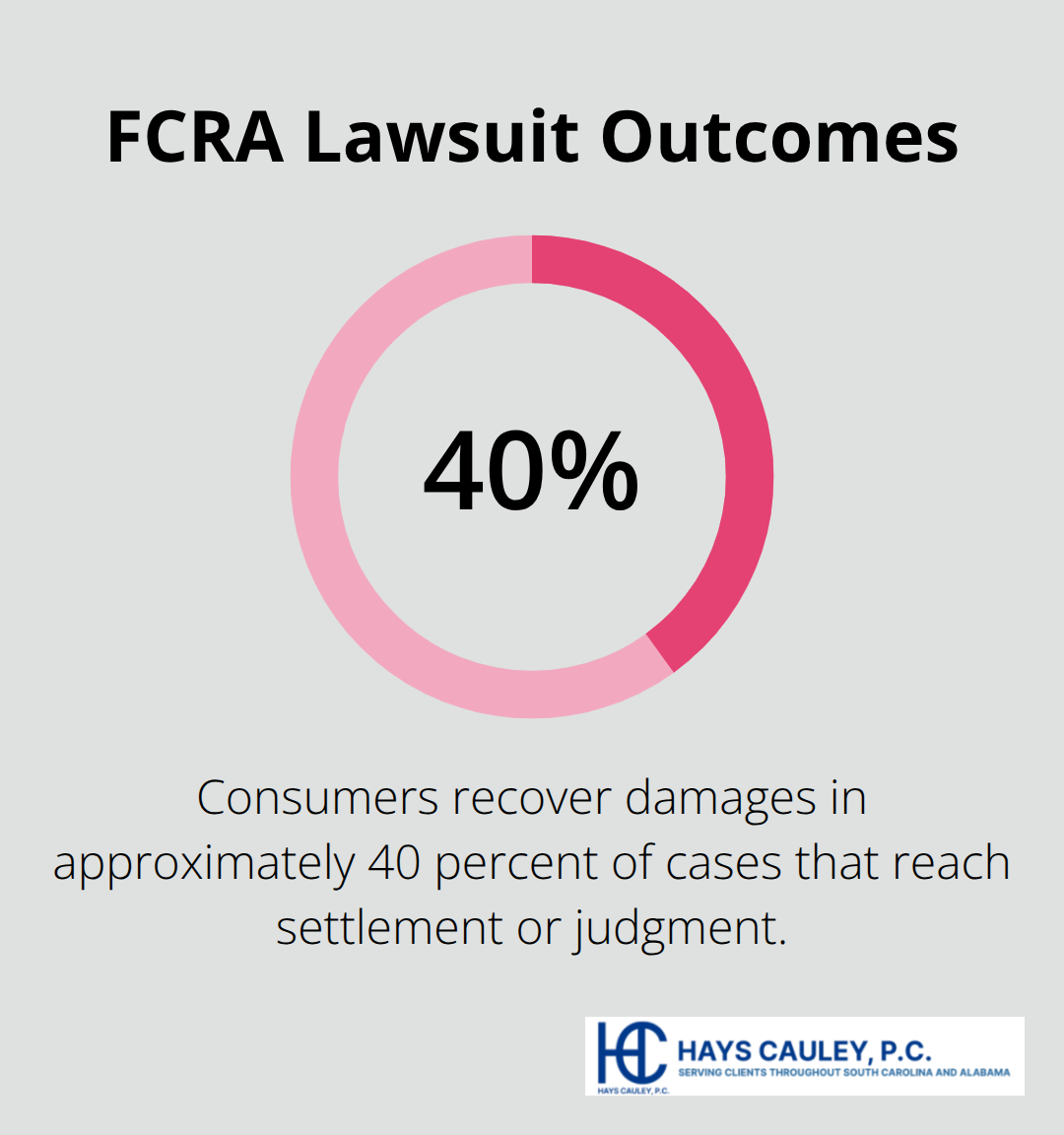

When furnishers or credit reporting agencies violate FCRA rules, you have concrete remedies available beyond simply fixing your credit report. Many consumers stop after their dispute resolves, but violations that occurred during the investigation process itself create separate legal claims. If a furnisher failed to investigate within 30 days, reported information they knew was inaccurate, or refused to correct errors across all three bureaus, those violations trigger compensation rights. The FCRA allows you to recover actual damages (money you lost due to the error), statutory damages between $100 and $1,000 per violation even without proving specific financial harm, and attorney fees if you pursue a lawsuit. The Federal Trade Commission reports that consumers who file FCRA lawsuits recover damages in approximately 40 percent of cases that reach settlement or judgment. The statutory damage provision matters because it means you don’t need to prove you lost $5,000 on a higher mortgage rate or missed a job opportunity-the law presumes harm occurred when violations happen.

How Statutory Damages Work in Your Favor

Statutory damages represent the FCRA’s most powerful tool for consumers. You don’t need receipts proving financial loss or documentation of rejected job applications. The law itself presumes that FCRA violations cause harm, so you recover $100 to $1,000 per violation regardless of whether you can quantify specific losses. A furnisher who failed to investigate your dispute within 30 days commits one violation. A furnisher who reported inaccurate information to all three bureaus commits three separate violations (one per bureau). A furnisher who refused to correct errors across all bureaus after investigation commits additional violations. These violations stack, which means a single case can involve multiple statutory damage claims. Courts have awarded statutory damages ranging from $300 to $750 per violation in settled cases, with some reaching higher amounts when violations were particularly egregious.

Actual Damages You Can Document and Recover

Beyond statutory damages, you can recover actual damages for financial harm the error directly caused. Higher interest rates on loans, denied credit applications, rejected job offers after background checks, increased insurance premiums due to credit score damage-all qualify as actual damages if you can connect them to the FCRA violation. You must document these losses with concrete evidence: loan documents showing the higher rate you paid compared to what you would have received with accurate credit, rejection letters from employers or lenders, insurance premium statements showing increases tied to your credit score. Courts have awarded actual damages ranging from $500 to $15,000 when consumers proved direct financial harm from FCRA violations. The challenge lies in proving causation-that the error specifically caused the financial loss rather than other factors. A rejected job application matters more when the employer’s letter states credit issues as the reason. A higher mortgage rate matters more when you can show lenders offered better terms to applicants with clean credit reports.

Settlement Negotiations and What They Include

Settlement negotiations in FCRA cases typically follow a predictable pattern. Once you file a formal complaint with the Consumer Financial Protection Bureau or initiate a lawsuit, furnishers and credit reporting agencies take violations seriously because CFPB penalties reach $4,983 per violation according to current inflation adjustments. Most cases settle before trial because litigation costs exceed what companies want to spend defending violations. Settlements usually include three components: payment for statutory damages (often $300 to $750 per violation depending on severity), reimbursement for actual documented losses, and a requirement that the defendant correct your credit report across all bureaus and prevent future violations through policy changes. You should document every financial impact the error caused so your attorney can present a complete damages picture during negotiations. The correction piece matters equally because settlements typically require furnishers to remove inaccurate items permanently and implement verification procedures to prevent similar errors. If a furnisher violated FCRA requirements during investigation, the settlement often includes provisions requiring them to conduct better employee training and implement random sampling of disputes to catch compliance problems before they harm consumers again.

Credit Report Corrections as Part of Settlement

Settlements that include credit report corrections require furnishers to notify all three major bureaus of the inaccurate information and instruct them to remove or correct the disputed item. This correction obligation extends beyond the initial settlement-furnishers must stop reporting the inaccurate information going forward and provide only corrected data if they continue reporting on the account. You should verify that all three bureaus updated your file within 30 days after the settlement takes effect. If one bureau still shows the old inaccurate information, contact that bureau directly with proof of the settlement correction notice. The removal of inaccurate items from your credit report can improve your credit score significantly, which translates to lower interest rates on future loans and better approval odds for credit applications. Some settlements include provisions requiring furnishers to add a consumer statement to your file explaining the dispute and correction, though this statement has limited impact on lender decisions compared to actual item removal.

When to Pursue Legal Action

You should pursue legal action when furnishers or credit reporting agencies refuse to correct errors after multiple disputes or when violations clearly occurred during their investigation process. If a furnisher failed to investigate within 30 days, reported information they knew was inaccurate, or ignored your dispute materials entirely, those violations create actionable claims. The FCRA allows you to file lawsuits in state or federal court, and you can recover attorney fees if you prevail, which means you don’t bear the full cost of litigation. Many consumers benefit from consulting with a consumer protection law firm that handles FCRA cases to evaluate whether their situation qualifies for damages and what settlement value their case might command.

Final Thoughts

FCRA investigation steps follow a clear timeline that protects your rights at every stage, from filing your initial dispute with specific documentation through the furnisher’s 30-day investigation window to corrections spreading across all three credit bureaus. Violations at any stage trigger compensation rights-furnishers who fail to investigate within the required timeframe, report information they know is inaccurate, or refuse to correct errors across all bureaus expose themselves to statutory damages between $100 and $1,000 per violation, plus actual damages for financial harm you can document. The Federal Trade Commission reports that consumers who pursue FCRA claims recover damages in approximately 40 percent of cases, which means your violations have real monetary value beyond simply fixing your credit report.

About 1 in 5 credit reports contain errors according to Consumer Financial Protection Bureau findings, so the odds are substantial that inaccurate information affects your file right now. Many consumers accept credit report errors as permanent when they actually have legal remedies available-corrections remove inaccurate items from your file, statutory damages compensate you for violations regardless of specific financial loss, and attorney fees shift litigation costs to the companies that violated your rights. The key is recognizing when violations occurred and taking action rather than accepting the initial outcome.

Start by pulling your credit reports from all three bureaus and identifying specific inaccurate items, then file disputes with detailed documentation supporting your claims. Track your confirmation numbers and follow up if furnishers miss the 30-day deadline, and verify that corrections spread across all three bureaus after investigation concludes. If furnishers refuse to correct errors or violations clearly occurred during their investigation, contact us at Hays Cauley, P.C. to evaluate whether your situation qualifies for damages and what your case might be worth-we help South Carolina consumers, including those in Greenville, Columbia, and Charleston, with credit reporting, identity theft, and debt-related issues.