A single error on your credit report can tank your score and cost you thousands in higher interest rates. We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, understand their rights when fighting inaccurate information.

Learning how to challenge credit report errors isn’t complicated, but it requires knowing the right steps and deadlines. This guide walks you through the entire process, from spotting mistakes to taking legal action if bureaus refuse to correct them.

Understanding Credit Report Errors: Serving South Carolina, Including Greenville, Columbia, and Charleston

What Errors Actually Show Up on Credit Reports

Credit reports contain thousands of data points, and mistakes happen far more often than most people realize. According to the Federal Trade Commission, one in five consumers finds an error on at least one of their three credit reports.

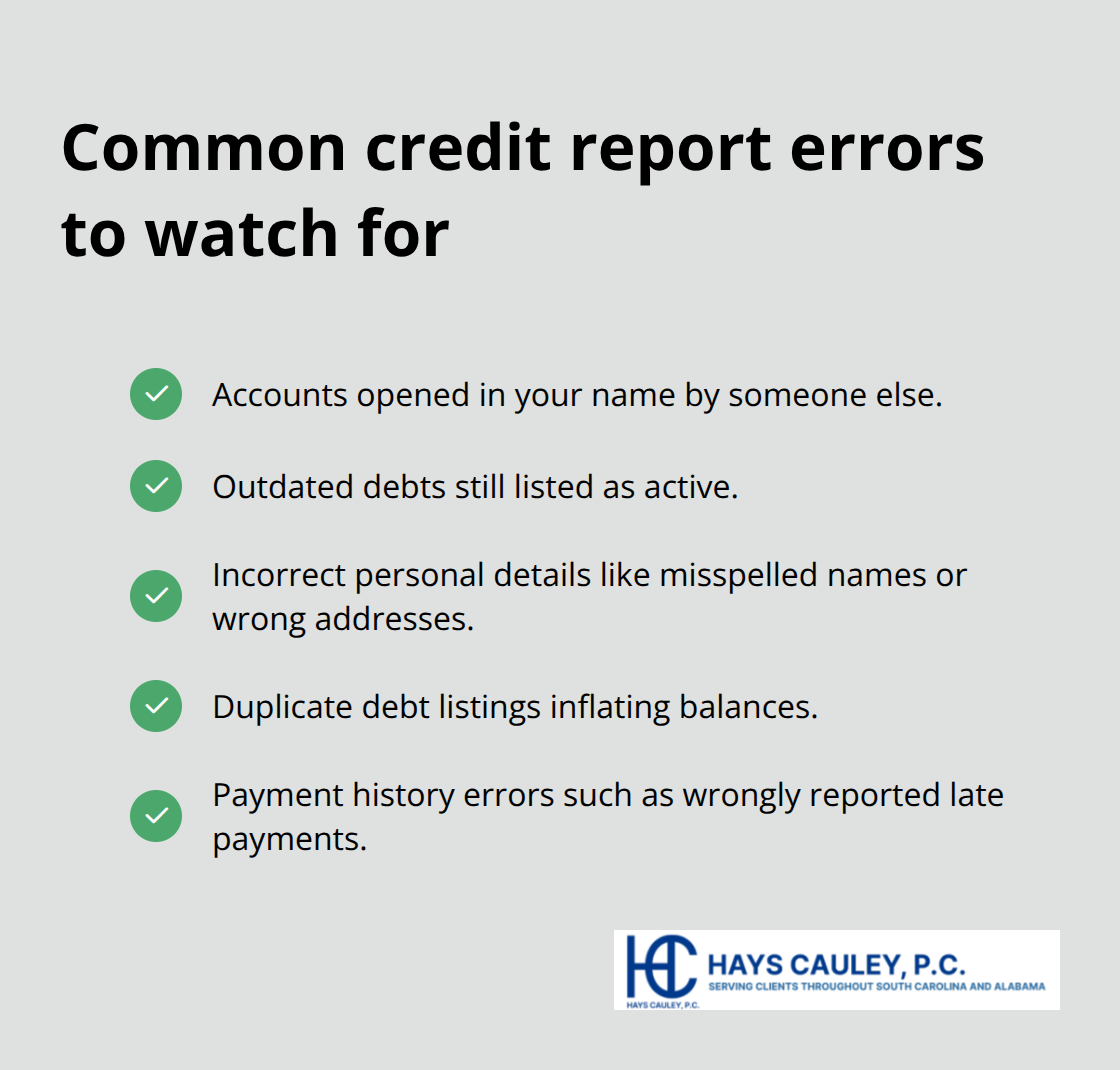

The errors range from minor details to account information that doesn’t belong to you at all. Accounts opened in your name by someone else, outdated debts still listed as active, incorrect personal details like misspelled names or wrong addresses, and duplicate debt listings are the most common problems that appear on reports. Payment history errors also surface frequently-a late payment marked when you paid on time, or a closed account still showing as open. These mistakes matter because they directly affect your credit score and the financial opportunities available to you.

How Errors Tank Your Financial Future

An inaccurate credit report doesn’t just lower your score-it costs you real money across multiple areas of your life. If your report shows negative information that shouldn’t be there, lenders charge higher interest rates because they think you’re a riskier borrower. Insurance companies use credit reports too, and errors can result in higher premiums. Landlords check credit reports before approving tenants, so an error could mean rejection for housing. Some employers pull credit reports during hiring decisions, and inaccuracies could cost you a job. The damage accumulates quickly. Someone with an error showing a missed payment might pay thousands more in interest on a mortgage or car loan compared to someone with a clean report. The Federal Trade Commission emphasizes that correcting these errors should be a priority because the financial consequences compound over time.

Your Legal Right to Demand Accuracy

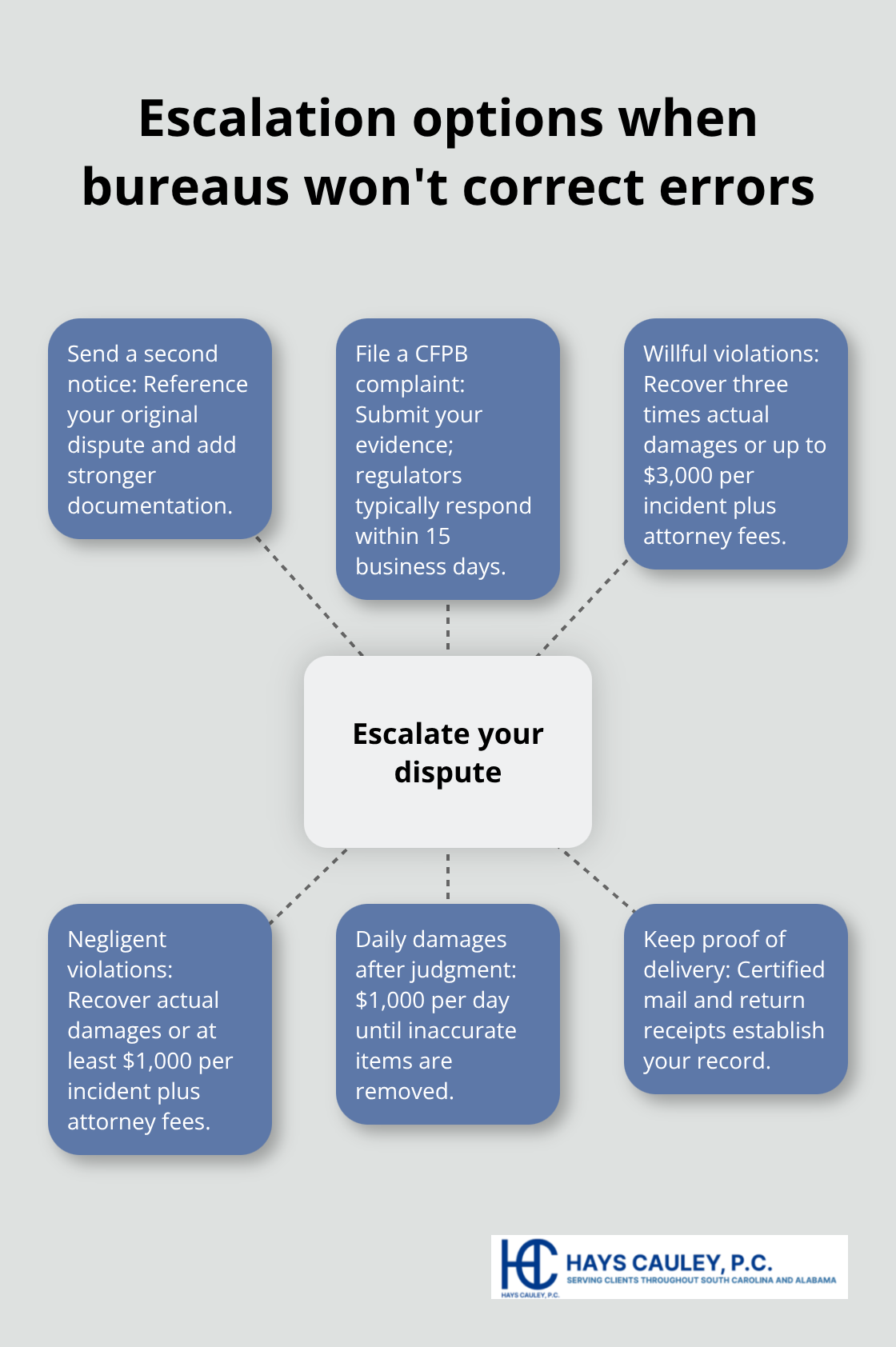

You have concrete legal protections under the Fair Credit Reporting Act that give you power to fight back. Both the credit bureau and the business that reported the information must correct inaccurate data at no cost to you. If a credit bureau ignores your dispute or fails to investigate within 30 days, you can file a complaint with the Consumer Financial Protection Bureau, which received over 175,000 credit reporting complaints in 2020 alone. You can also pursue civil action. Willful violations of credit reporting law can result in three times your actual damages or up to $3,000 per incident (plus attorney fees). Even negligent violations can yield actual damages or at least $1,000 per incident (plus attorney fees). If an inaccurate item harms your creditworthiness and a judgment is entered, damages can accrue at $1,000 per day until the item is removed. These aren’t theoretical protections-they’re enforceable rights that give you leverage to get corrections made.

Taking Action Against Inaccuracies

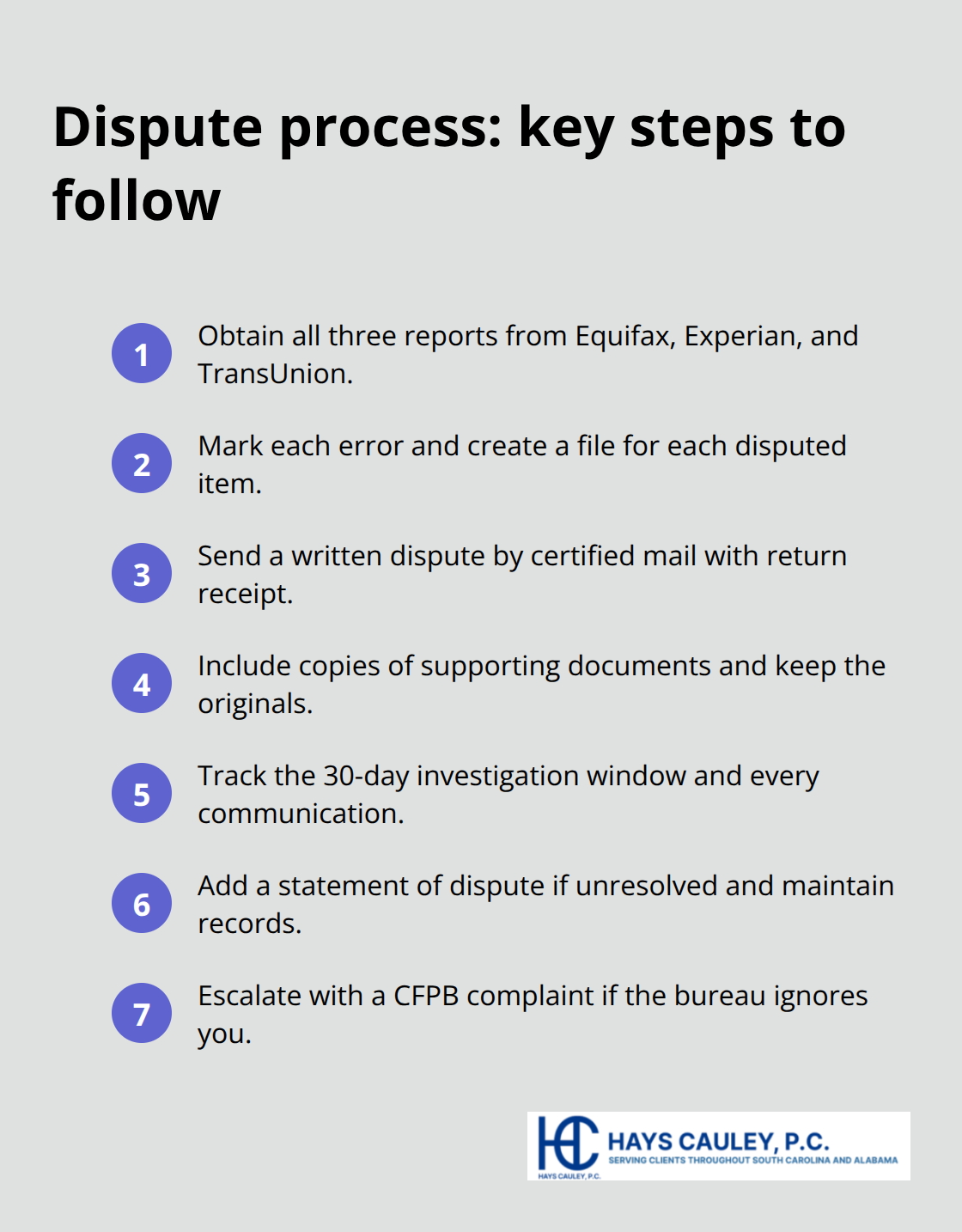

The path forward starts with obtaining your credit reports and identifying which items are wrong. You can access free copies from Equifax, Experian, and TransUnion once every 12 months through AnnualCreditReport.com, or you can check each report for free once a week through the bureaus’ permanent monitoring option. Equifax also provides six free reports per year through 2026. Once you spot an error, the dispute process begins-and knowing how to file that dispute correctly determines whether you succeed or waste months going in circles.

Step-by-Step Process for Disputing Credit Report Errors: Serving South Carolina, Including Greenville, Columbia, and Charleston

Pull Your Reports and Spot the Mistakes

Start by obtaining all three credit reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com, the official source mandated by federal law. You get one free report from each bureau every 12 months, but stagger your requests every four months to monitor accuracy across all three bureaus throughout the year. Equifax offers an additional six free reports per year through 2026, so take advantage of that too. When you receive your reports, search methodically for unfamiliar accounts, incorrect personal details like misspelled names or wrong addresses, outdated negative items still showing as active, and duplicate debt listings.

Circle every error on a printed copy and create a separate file for each disputed item. This organization matters because you’ll need to reference specific account numbers, creditor names, and dates when you file your dispute. A wrong address or misspelled name gives credit bureaus an excuse to dismiss your claim as frivolous, so don’t overlook minor details.

File Your Dispute in Writing with Proof of Delivery

File your dispute in writing and send it by certified mail with return receipt to create a verifiable paper trail that activates your legal protections. Contact information for disputes goes to Equifax at P.O. Box 740256, Atlanta, GA 30348; Experian at P.O. Box 4500, Allen, TX 75013; and TransUnion Consumer Dispute Center at P.O. Box 2000, Chester, PA 19016. You can also dispute online or by phone-Experian at 888-397-3742, TransUnion at 800-916-8800, and Equifax at 866-349-5191-but written disputes create proof that the bureau received your request.

Include copies of supporting documents like bank statements, payment receipts, and creditor correspondence, but never send originals. The Federal Trade Commission provides template letters to help you structure your dispute, and you should itemize each error with the exact account number, creditor name, and a clear reason for your dispute.

Track Progress and Document Everything

The bureau has 30 days to investigate and notify you of results. Keep detailed records of every communication, including dates, names of representatives, and what was discussed. About 70 percent of disputes result in some modification to the credit report, though persistence often separates those who get full corrections from those who see partial results.

If the bureau finds information inaccurate, it must correct your file and notify all three bureaus to update their records. If the investigation doesn’t resolve your dispute, you can add a statement of dispute to your file, and future creditors will see your version of events. When the 30-day window closes without satisfactory results, your next move determines whether you accept a partial correction or escalate to stronger action.

When Credit Bureaus Refuse to Correct Errors: Serving South Carolina, Including Greenville, Columbia, and Charleston

Send a Second Notice with Stronger Documentation

Many people assume that a single dispute automatically fixes the problem, but that’s not how it works in practice. If a credit bureau dismisses your dispute as frivolous, ignores your request entirely, or fails to investigate within the 30-day window, you need escalation strategies that actually work. The first move is sending a second notice directly to the bureau, this time with more aggressive documentation. Include a cover letter stating that this is your second request and reference the date of your original dispute. Attach copies of your supporting documents again, but this time add anything new that strengthens your case-bank statements showing payment dates, creditor correspondence confirming the error, or written confirmation from the business that reported the information. Send this via certified mail with return receipt just like your first dispute.

Some bureaus process second notices faster because they recognize the increased legal exposure.

File a Complaint with the Consumer Financial Protection Bureau

If the bureau still ignores you after 30 days, file a complaint with the Consumer Financial Protection Bureau at consumerfinance.gov. The CFPB received over 175,000 credit reporting complaints in 2020, so they take these cases seriously. Your complaint becomes part of the bureau’s record and triggers investigation by federal regulators. Include your original dispute letter, proof of certified mailing, the bureau’s response (or lack thereof), and a clear explanation of why their investigation was inadequate. The CFPB typically responds within 15 business days and forwards your complaint to the credit bureau for a formal response. When the CFPB gets involved, credit bureaus move faster because regulatory scrutiny carries real consequences.

Pursue Legal Action for Persistent Violations

At this point, if you still haven’t achieved results, legal action becomes your most effective option. Willful violations of the Fair Credit Reporting Act allow you to recover three times your actual damages or up to $3,000 per incident plus attorney fees. Negligent violations yield actual damages or at least $1,000 per incident plus attorney fees. If inaccurate information harms your creditworthiness and a damages judgment is entered, you can recover $1,000 per day until the item is removed. These remedies exist specifically to hold credit bureaus accountable when they refuse to correct verifiable errors. A consumer protection law firm dedicated to credit reporting issues can evaluate your case, identify statutory violations, and determine whether legal action makes financial sense for your situation.

Final Thoughts

Challenging credit report errors requires persistence, documentation, and knowing when to escalate your efforts. The process starts with obtaining your free reports from all three bureaus and identifying mistakes methodically, then filing your dispute in writing by certified mail with supporting documents to track the 30-day investigation window. About 70 percent of disputes result in some modification, but getting full corrections often means sending a second notice or filing a complaint with the Consumer Financial Protection Bureau when bureaus ignore your request.

If a credit bureau refuses to correct verifiable errors after 30 days, legal action becomes your strongest tool for how to challenge credit report errors effectively. Willful violations of the Fair Credit Reporting Act allow you to recover three times your actual damages or up to $3,000 per incident plus attorney fees, while negligent violations yield at least $1,000 per incident plus attorney fees (damages can accrue at $1,000 per day until inaccurate items are removed). Start immediately after spotting errors because negative information stays on your report for seven years, and every month of delay costs you in higher interest rates and missed opportunities.

We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, challenge inaccurate credit information and hold bureaus accountable when they refuse to correct errors. If disputes stall or you face willful violations, contact our consumer protection law firm to evaluate your case and determine whether legal action makes sense for your situation.