Identity theft affects millions of Americans each year, and the financial and emotional toll can be devastating. The Identity Theft Assumption Deterrence Act gives you powerful legal protections and clear steps to recover.

At Hays Cauley, P.C., we help identity theft victims throughout South Carolina, including Greenville, Columbia and Charleston, understand their rights and take action. This guide walks you through what the law protects, how to dispute fraudulent charges, and what to do right now if you’re a victim.

What the Identity Theft Assumption Deterrence Act Actually Does

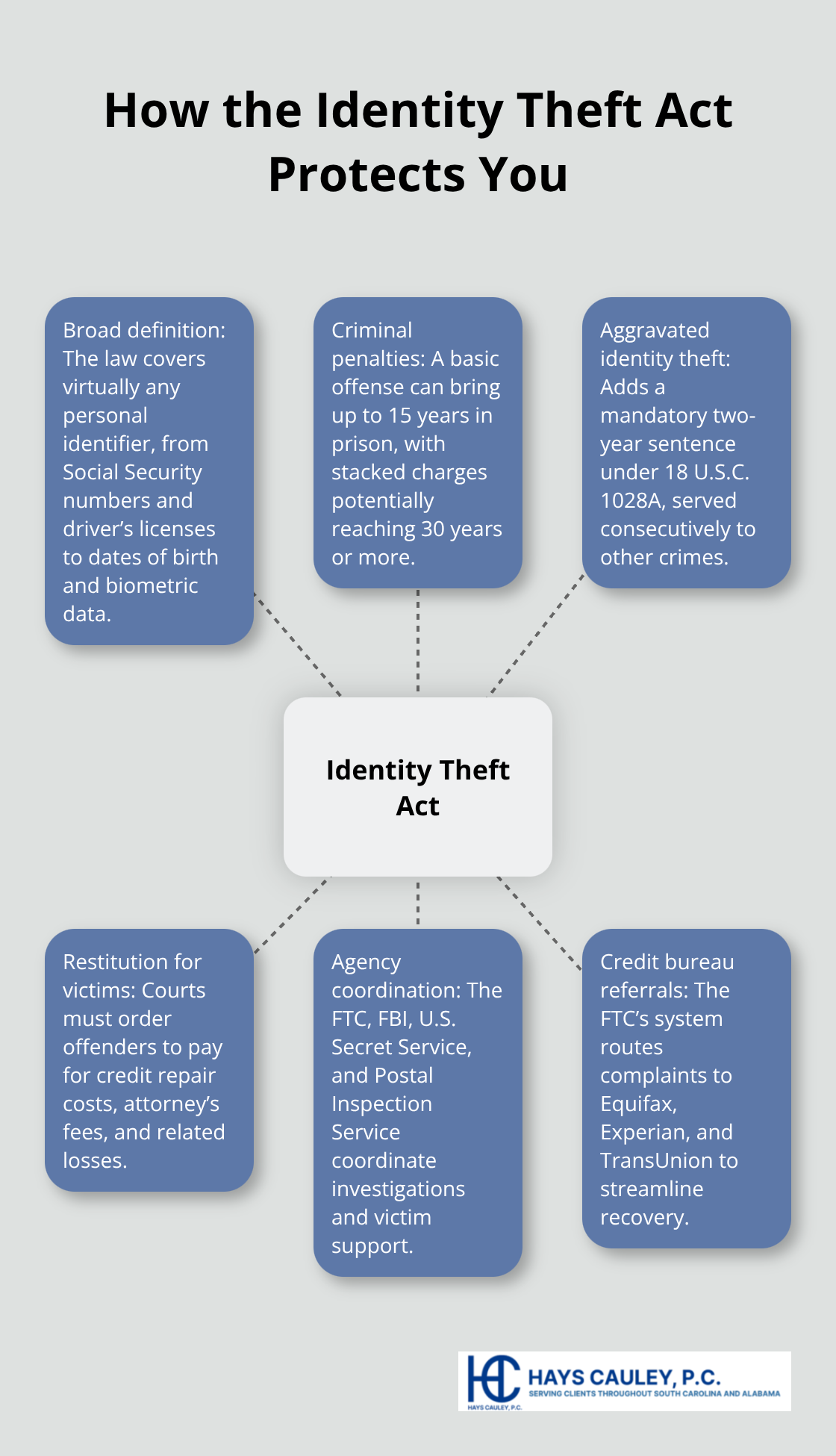

Congress passed the Identity Theft Assumption Deterrence Act in 1998 because identity theft was becoming a widespread problem that existing laws couldn’t adequately address. The Act created the first federal framework specifically designed to criminalize identity theft and give victims concrete remedies. Senator Jon Kyl introduced the legislation after recognizing that criminals were stealing personal information and using it to open credit accounts, take out loans, and obtain government IDs in victims’ names. The law defines identity theft as knowingly transferring or using someone else’s means of identification to commit or aid unlawful activity. A means of identification includes Social Security numbers, driver’s license numbers, dates of birth, government ID numbers, biometric data, and names or numbers that can identify a specific person.

This broad definition matters because it means criminals face prosecution for stealing or misusing virtually any personal identifier, not just credit card numbers.

Criminal Penalties That Actually Deter Theft

The Act imposes serious federal penalties to discourage identity theft crimes. A basic identity theft offense carries up to 15 years in prison plus fines and forfeiture of property used to commit the crime. When identity theft occurs alongside other federal crimes like wire fraud, mail fraud, or credit card fraud, prosecutors can stack additional charges that push sentences to 30 years or more. The Act also created aggravated identity theft under 18 U.S.C. 1028A, which imposes a mandatory two-year sentence that runs consecutively to any underlying offense. This means if someone steals your identity while committing another federal felony, they face at least two additional years in prison on top of whatever sentence they receive for the underlying crime.

How Sentencing Guidelines Reflect the Crime’s Severity

The U.S. Sentencing Commission adjusted federal sentencing guidelines to reflect these offenses, considering factors like the number of victims, the number of means of identification involved, and the total value of losses. These penalties apply to attempts and conspiracies to commit identity theft as well, not just completed crimes. Law enforcement agencies including the FBI, U.S. Secret Service, and the United States Postal Inspection Service investigate identity theft cases and coordinate to pursue offenders across state lines (since identity theft frequently involves interstate commerce or mailed documents).

What Victims Actually Recover

The Act mandates that courts order restitution to victims, which means the convicted offender must pay you for direct losses caused by their crime. Restitution covers costs to repair your credit history, attorney’s fees, and debts arising from the defendant’s actions. This protection matters because identity theft victims often spend hundreds or thousands of dollars clearing their names and fixing fraudulent accounts. The Federal Trade Commission enforces victim protections by maintaining a centralized complaint system and referring cases to the three major national consumer reporting agencies: Equifax, Experian, and TransUnion.

How the Act Coordinates Recovery Across Agencies

The Act’s integrated approach combines criminal penalties with victim support systems designed to help you report theft and recover quickly. Multiple federal agencies work together to investigate and prosecute offenders, creating a coordinated response that increases the likelihood of holding criminals accountable. Understanding these protections sets the foundation for knowing what rights you actually have when identity theft strikes-and what steps you can take to exercise those rights.

Your Rights Under the Identity Theft Assumption Deterrence Act: Serving South Carolina, including Greenville, Columbia and Charleston

Contact Affected Companies and Freeze Accounts Immediately

The Identity Theft Assumption Deterrence Act gives you concrete rights to challenge fraudulent accounts and restore your credit, but most victims don’t know how to exercise them effectively. Contact the fraud department of any company where you discovered unauthorized activity and request that they freeze or close those accounts immediately. This action stops criminals from making additional charges while you work through the recovery process.

Place a Fraud Alert with Credit Bureaus

Place a fraud alert with one of the three major credit bureaus by calling Experian at 1-888-397-3742, TransUnion at 1-800-680-7289, or Equifax at 1-888-766-0008. The fraud alert is free and makes it significantly harder for someone to open new accounts in your name because creditors must verify your identity before extending credit. The alert stays active for one year and you can renew it if needed.

Review Your Credit Reports and Dispute Fraudulent Accounts

You have the right to obtain free credit reports from all three bureaus through annualcreditreport.com or by calling 1-877-322-8228 to identify unfamiliar accounts or fraudulent transactions. Review these reports carefully because they reveal the full scope of damage and provide documentation for disputes. When you find fraudulent accounts, dispute them directly with the credit reporting agencies in writing and provide copies of your FTC Identity Theft Report as evidence. The Fair Credit Reporting Act requires bureaus to investigate disputes within 30 days and they must remove inaccurate information if they cannot verify it.

File Reports with the FTC and Law Enforcement

Report the identity theft to the Federal Trade Commission at IdentityTheft.gov, which generates a personalized Identity Theft Report and recovery plan that creditors and credit bureaus recognize as official documentation. File a police report and bring your FTC Identity Theft Report, government-issued photo ID, proof of address, and any documents related to the theft. Request a copy of the police report because creditors often require it when you dispute fraudulent charges or close accounts. In South Carolina, identity theft qualifies as a felony under state and federal law, which means law enforcement takes these cases seriously and prosecutors can pursue criminal charges against offenders.

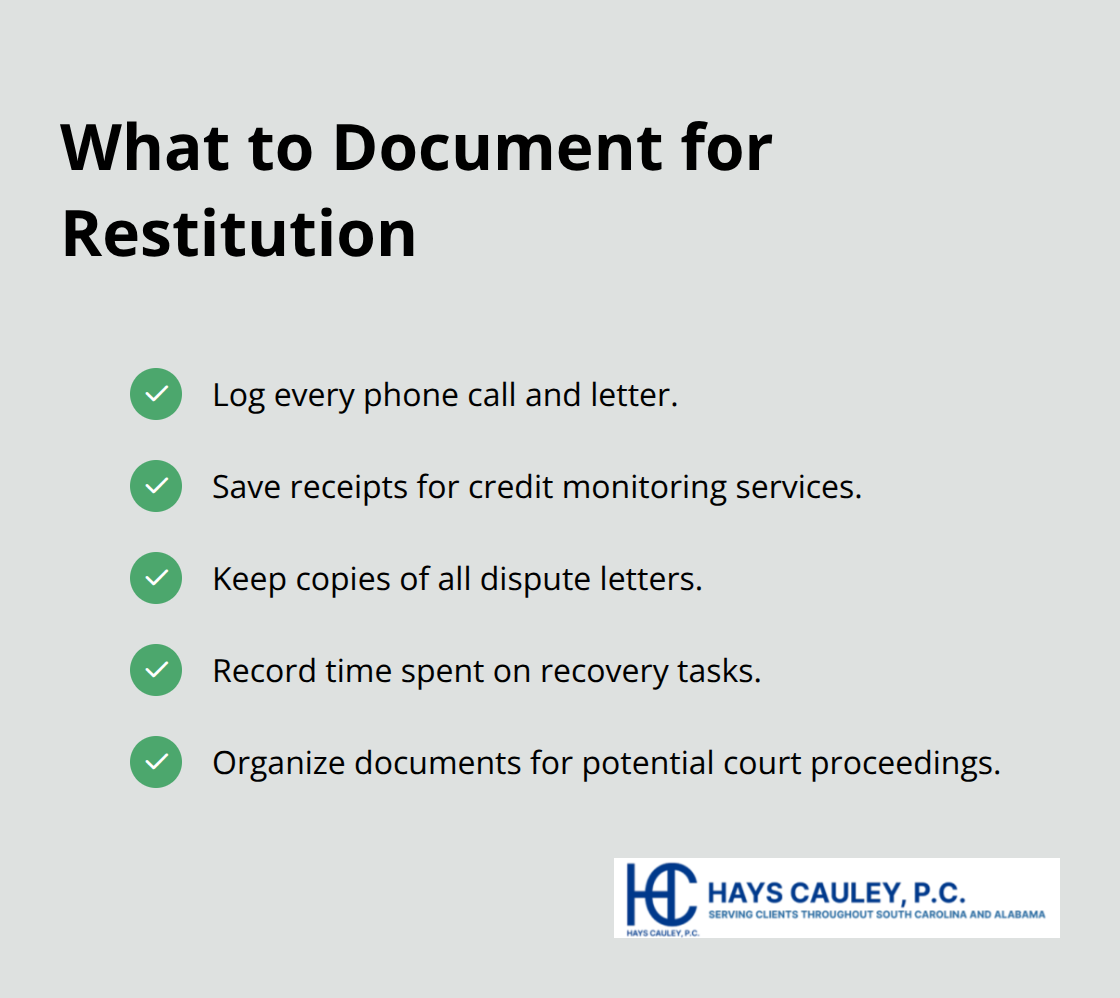

Document All Expenses for Potential Restitution

Under the Act, convicted offenders must pay restitution to cover your costs for repairing credit, including attorney’s fees and debts arising from the defendant’s actions, so you should document every expense related to your recovery. Track phone calls, written correspondence, credit monitoring fees, and time spent resolving accounts. The federal framework created by the Act coordinates agency responses so that your single report to the FTC triggers referrals to Equifax, Experian, and TransUnion, streamlining the recovery process and eliminating the need to contact each agency separately or repeat your story multiple times. Once you’ve taken these steps, the next phase involves working directly with creditors and credit bureaus to remove fraudulent information from your accounts and credit history.

Steps to Take if You’re a Victim of Identity Theft

Act Within the First 24 Hours

The first 24 hours after discovering identity theft determine how much damage you can prevent. Contact the fraud department of every company where you found unauthorized activity and demand that they freeze or close those accounts immediately. This stops additional charges from accumulating while you work through recovery.

Place Fraud Alerts with Credit Bureaus

Experian, TransUnion, and Equifax all maintain fraud departments that can place fraud alerts preventing new account openings. Call Experian at 1-888-397-3742, TransUnion at 1-800-680-7289, or Equifax at 1-888-766-0008. Calling one bureau automatically triggers alerts at the other two under federal law. These calls take minutes and cost nothing. The alert remains active for one year, giving you breathing room to assess the full scope of the theft.

Review Credit Reports and Dispute Fraudulent Accounts

Obtain your free credit reports from all three bureaus through annualcreditreport.com or 1-877-322-8228 to identify every fraudulent account opened in your name. Review these reports line by line because they reveal the complete picture of what criminals have done. Write dispute letters to each credit bureau documenting the fraudulent accounts and include your FTC Identity Theft Report as supporting evidence. Federal law requires bureaus to investigate disputes within 30 days and remove information they cannot verify.

File Reports with the FTC and Police

File a report with the Federal Trade Commission at IdentityTheft.gov immediately because the system generates an official Identity Theft Report that creditors recognize and that law enforcement uses. Then file a police report in your jurisdiction, bringing your FTC report, government-issued photo ID, proof of address, and any documents showing the theft. Request a written copy of the police report because banks and creditors often demand it before closing fraudulent accounts or removing charges.

Contact Financial Institutions and Document Everything

Contact your bank and credit card companies to report the fraud and request new cards with different account numbers. Document every phone call, email, and piece of correspondence throughout this process because under the Identity Theft Assumption Deterrence Act, convicted offenders must pay restitution covering your costs for credit repair, attorney’s fees, and time spent resolving accounts. Keep receipts for credit monitoring services, copies of dispute letters, and records of time spent on recovery calls. This documentation becomes critical if the case reaches prosecution and restitution hearings.

The FTC’s centralized system automatically refers your complaint to Equifax, Experian, and TransUnion, eliminating the need to contact each agency separately and ensuring coordinated action across the credit reporting system.

Final Thoughts

The Identity Theft Assumption Deterrence Act transformed how federal law addresses identity theft by creating real consequences for criminals and real remedies for victims. Federal penalties reach 15 years in prison, plus mandatory two-year sentences for aggravated identity theft, signaling that this crime carries serious weight in the criminal justice system. The FTC’s centralized complaint system automatically coordinates with Equifax, Experian, and TransUnion, eliminating the burden of contacting each agency separately.

Your recovery path includes free credit reports through annualcreditreport.com, fraud alert phone lines at the three major credit bureaus, and the FTC’s personalized recovery plans. Law enforcement agencies including the FBI and U.S. Secret Service investigate cases across state lines, increasing the likelihood that criminals face accountability. Documentation of your expenses becomes critical because restitution orders can cover credit repair costs, attorney’s fees, and time spent resolving fraudulent accounts.

We at Hays Cauley, P.C. help identity theft victims throughout South Carolina, including Greenville, Columbia and Charleston, understand their rights and pursue recovery. Contact us to discuss how we can support your recovery and protect your rights under the Identity Theft Assumption Deterrence Act.