Identity theft affects millions of Americans each year, and the financial and emotional toll can be devastating. If you’re facing unauthorized accounts, credit damage, or disputes with creditors and credit bureaus, you need an attorney for identity theft who understands both the legal landscape and the urgency of your situation.

At Hays Cauley, P.C., we help clients navigate these complex cases and recover their financial health. This guide walks you through the signs you need legal help, what to look for in representation, and the immediate steps to protect yourself.

When Do You Need Legal Help for Identity Theft

Unauthorized Accounts Signal Immediate Danger

Recognizing when identity theft crosses into territory that demands legal representation separates victims who recover quickly from those who spend years battling fraudulent accounts. The moment you discover unauthorized activity is not the moment to decide whether an attorney matters-it’s the moment to understand which situations absolutely require one. South Carolina ranks as the 13th highest state for identity theft reports per 100,000 citizens, which means the threat is real and local.

When someone opens accounts in your name-credit cards, loans, utilities, even medical services-without your consent, you face liability for charges you never authorized. Banks and creditors will pursue you for payment, and without legal intervention, these accounts damage your credit score and create a paper trail of fraudulent debt. A single fraudulent account can lower your score by 100 points or more, affecting your ability to secure mortgages, car loans, and employment opportunities for years.

Multiple Creditors and Agencies Require Professional Help

When multiple creditors and agencies become involved-your bank, credit card companies, credit bureaus, and potentially law enforcement-the complexity explodes. You cannot effectively negotiate with three credit bureaus simultaneously while disputing charges with your bank and responding to collection agencies. Creditors ignore consumer complaints without legal pressure behind them, leaving you stuck in a cycle of repeated disputes and mounting frustration.

The Federal Trade Commission reports that identity theft victims spend an average of 16 hours resolving fraud, but complex cases involving multiple creditors often require 40 hours or more of your personal time. That calculation excludes the emotional toll and the risk of missing critical deadlines. The time investment alone makes professional representation a practical necessity, not a luxury.

Legal Notices and Tax Fraud Demand Immediate Action

If you receive legal notices for crimes you did not commit, or if fraudulent tax returns have been filed in your name, waiting to hire an attorney actively harms your position. Statutes of limitations apply to disputes and lawsuits, meaning delayed action can eliminate your right to recover damages entirely. These situations move quickly, and every week you wait strengthens the creditor’s position and weakens yours.

The moment you find unfamiliar accounts on your credit report, unauthorized charges on bank statements, or notices from creditors about accounts you never opened, contact an attorney. Acting quickly prevents new fraudulent accounts from being opened in your name and preserves your ability to hold banks and credit bureaus accountable for their failures to verify identity. What comes next requires understanding exactly what to look for in the right legal representation.

What Separates Strong Identity Theft Attorneys from Weak Ones

Experience Matters More Than General Practice

The difference between an attorney who merely handles identity theft cases and one with real depth in this practice shows up immediately in how they attack your problem. An attorney with genuine experience in identity theft and credit reporting knows the Fair Credit Reporting Act inside out, understands how to leverage the Identity Theft Enforcement and Restitution Act, and recognizes which creditors routinely ignore consumer disputes. This knowledge translates to faster resolution and better outcomes.

When you call an attorney’s office, ask directly: How many identity theft cases have you handled in the past two years? If they hesitate or give a vague answer, that’s your signal to keep looking. Beyond experience, demand to see concrete results.

Track Record Reveals What Attorneys Actually Accomplish

Ask for examples of outcomes in cases resembling yours-not hypothetical scenarios, but actual cases where charges were avoided, fraudulent accounts were removed, or creditors reversed charges. Many attorneys will cite general statistics about identity theft prevalence, but few will show you their track record. The Federal Trade Commission reports that identity theft victims lose an average of $5,000 per incident, yet most attorneys won’t tell you how much they recovered for clients or how quickly they resolved disputes.

Request case results or summaries that demonstrate what the attorney has accomplished for clients facing unauthorized accounts, credit bureau disputes, or creditor negotiations. If an attorney cannot or will not provide this information, they lack confidence in their results. This transparency separates attorneys who produce outcomes from those who simply process cases.

Federal Law Knowledge Determines Your Leverage

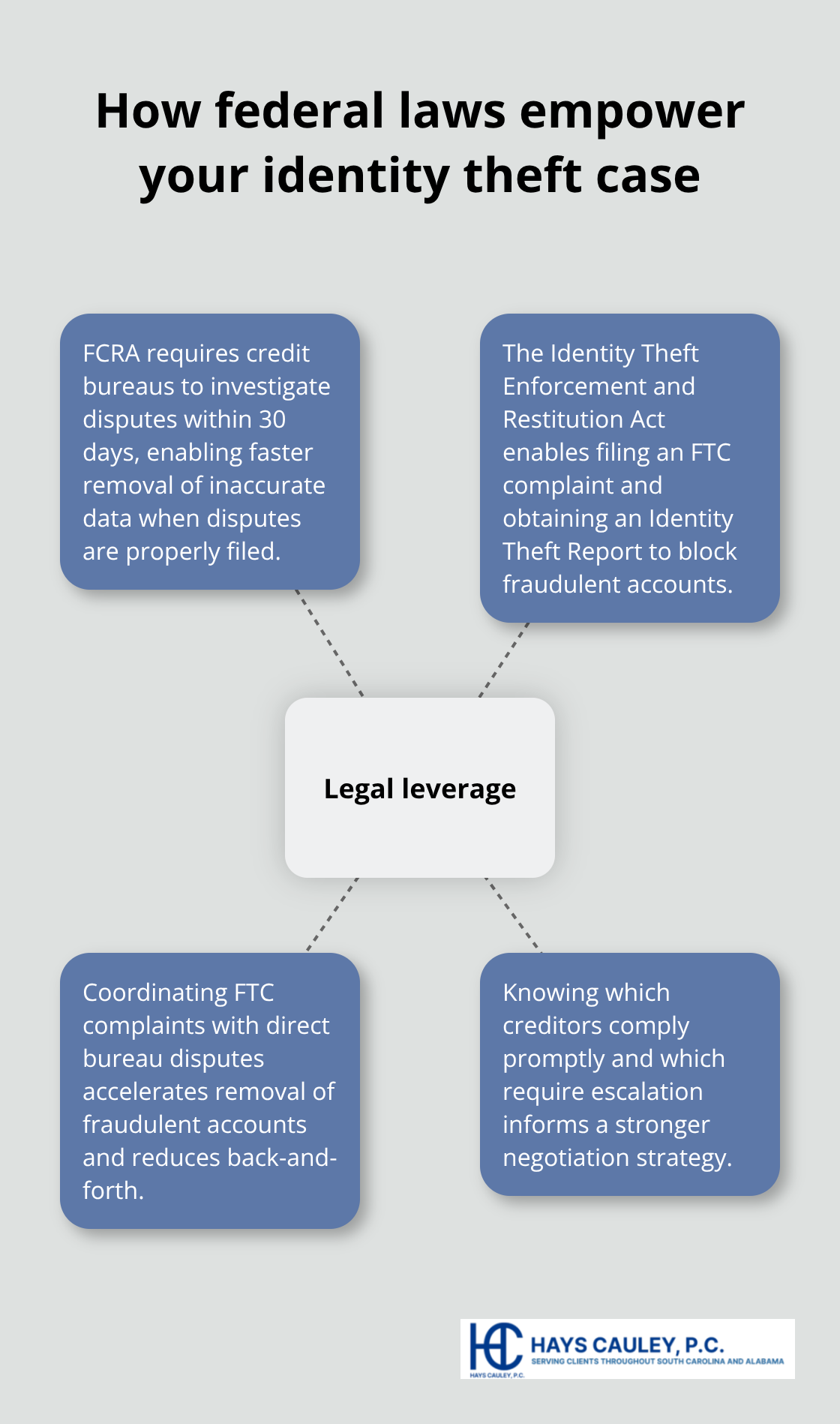

Federal law is your leverage in identity theft cases, and your attorney must know how to use it. The Fair Credit Reporting Act gives you the right to dispute inaccurate information on your credit report, and it requires credit bureaus to investigate disputes within 30 days. The Identity Theft Enforcement and Restitution Act allows you to file a complaint with the Federal Trade Commission and receive an Identity Theft Report, which you can then send to creditors and bureaus to block fraudulent accounts.

An attorney who understands these laws can coordinate your FTC complaint with disputes filed directly to credit bureaus, dramatically accelerating removal of fraudulent accounts. They also understand which creditors must comply with these laws and which ones ignore them-knowledge that shapes your negotiation strategy. This coordination separates effective representation from scattered efforts.

State Law Protections Strengthen Your Position

Your attorney should understand state laws in South Carolina that govern identity theft disputes and credit freezes. Many attorneys focus only on federal law and miss state-level protections that strengthen your position. During your consultation, ask the attorney to explain your rights under the Fair Credit Reporting Act and how they will use the Identity Theft Enforcement and Restitution Act in your specific case.

If they cannot articulate a clear strategy tied to these laws, they lack the depth required to represent you effectively. The right attorney will walk you through how federal and state protections work together to remove fraudulent accounts and restore your credit. This comprehensive approach determines whether your case moves forward efficiently or stalls in disputes with creditors and bureaus.

What to Do Right Now

Gather and Organize Your Evidence

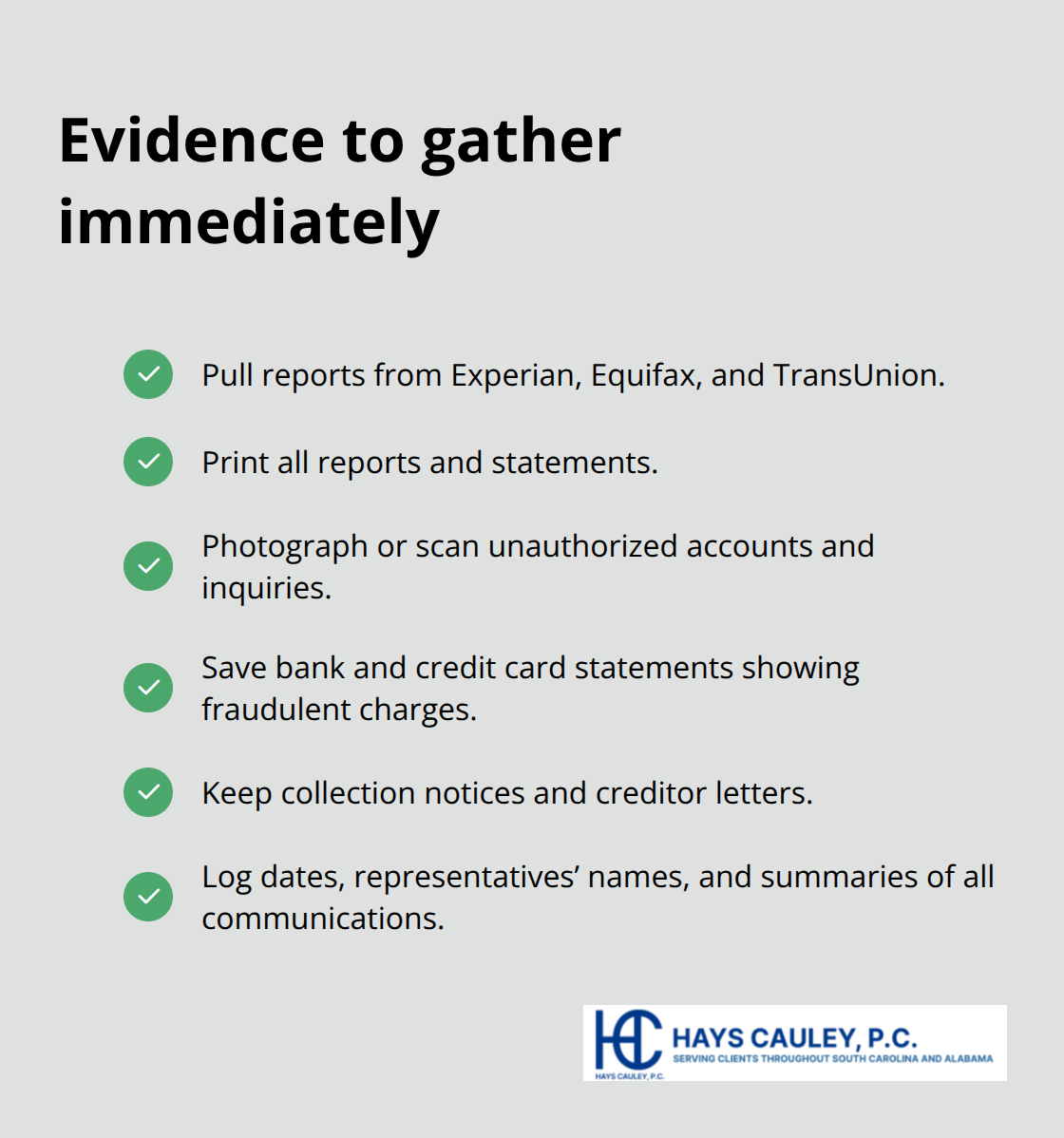

Start collecting evidence the moment you suspect identity theft. Pull your credit reports from all three bureaus-Experian, Equifax, and TransUnion-using the free annual reports available at annualcreditreport.com. Print everything. Photograph or scan unauthorized accounts, unfamiliar inquiries, and any suspicious activity you find. Create a folder with bank statements showing fraudulent charges, credit card statements with accounts you never opened, and any collection notices or letters from creditors.

This documentation becomes your roadmap for disputes and your proof when negotiating with banks and credit bureaus. The Federal Trade Commission recommends keeping detailed records of all communications with creditors and bureaus, including dates, names of representatives, and what was discussed. Without this evidence, credit bureaus will dismiss your disputes as unsubstantiated claims, and creditors will ignore your demands to reverse charges.

File Your FTC Report Immediately

File an official report with the Federal Trade Commission at IdentityTheft.gov within days of discovering the fraud. The FTC generates an Identity Theft Report that carries legal weight with creditors and credit bureaus-many are required to honor this document and remove fraudulent accounts from your credit file within 30 days. The report also creates an official record that protects you if criminals file fraudulent tax returns or open accounts in your name months later.

South Carolina residents can also file a police report with their local department and contact the South Carolina Department of Consumer Affairs at IDTheftHelp@scconsumer.gov or 803-734-4200 for additional guidance and resources. This multi-agency approach strengthens your position and creates multiple official records of the fraud.

Contact Your Bank and Credit Card Companies

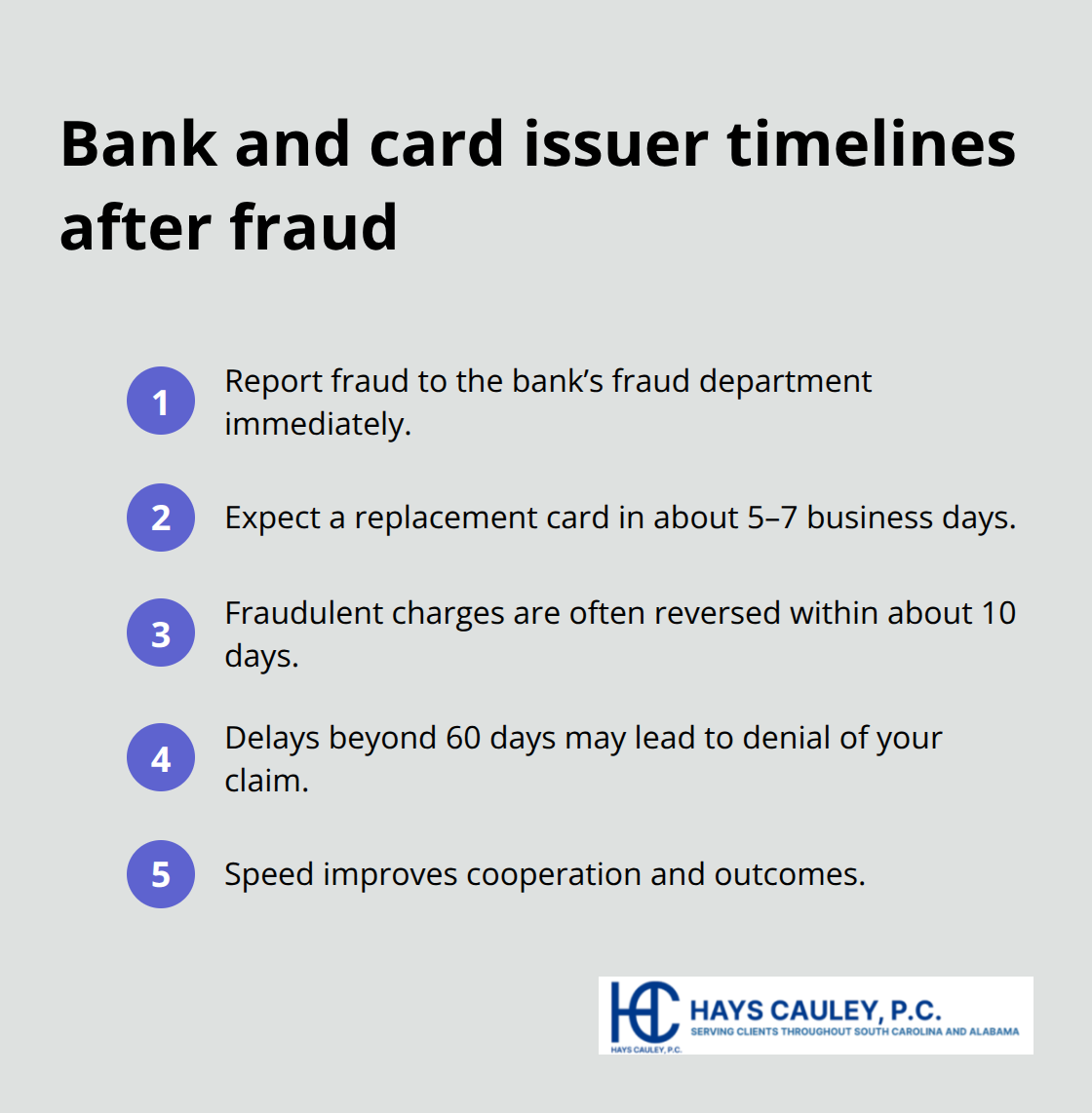

Contact your bank and credit card companies immediately-not through customer service chat, but through the fraud department phone number on the back of your card or your account statements. Tell them specifically which transactions are fraudulent and request that they reverse the charges and close compromised accounts. Document the name and employee ID of every representative you speak with and request written confirmation of the fraud report.

Many banks will issue a new card within 5–7 business days and reverse fraudulent charges within 10 days if you report quickly. The longer you wait, the more difficult banks become to work with, and some will deny your claim entirely if you delay reporting beyond 60 days. Speed matters tremendously in this phase.

Dispute Fraudulent Accounts with Credit Bureaus

Contact the credit bureaus directly to dispute fraudulent accounts by mail or through their online dispute portals-do not rely on creditors to report corrections to the bureaus themselves. Coordinate your FTC report with direct bureau disputes to accelerate removal of fraudulent accounts and prevent creditors from reporting false debts to your credit file. This systematic approach (combining FTC filings with bureau disputes) produces faster results than scattered efforts.

Hiring an attorney to manage these disputes with creditors and credit bureaus eliminates the back-and-forth that consumes 40 hours or more of your personal time and increases the likelihood that fraudulent accounts are removed permanently rather than simply disputed and re-reported months later. An attorney who understands credit reporting law knows which creditors respond to legal pressure and which ones require escalation to achieve results.

Final Thoughts

Identity theft doesn’t resolve itself, and waiting costs you money, time, and peace of mind. Every day you delay filing an FTC report or disputing fraudulent accounts allows criminals to open new accounts in your name and creditors to report false debts to your credit file. The statutes of limitations that protect your right to recover damages and hold banks accountable don’t pause while you decide whether to act.

The right attorney for identity theft cases accelerates your recovery by handling the disputes, negotiations, and legal filings that would otherwise consume 40 hours or more of your personal time. An attorney who understands the Fair Credit Reporting Act and Identity Theft Enforcement and Restitution Act knows exactly which creditors will respond to legal pressure and which ones require escalation. They coordinate your FTC report with credit bureau disputes, negotiate with banks to reverse fraudulent charges, and file lawsuits when necessary to recover damages for financial loss, legal fees, and emotional distress.

If you’re facing unauthorized accounts, credit damage, or disputes with multiple creditors, contact us at hayscauley.net to discuss your situation. We help consumers navigate identity theft and credit reporting issues with the urgency these cases demand. Your path forward starts with one conversation and the decision to act now rather than later.