Credit reporting errors can devastate your financial life, yet many South Carolina consumers don’t know their rights under federal law. When credit agencies, employers, or landlords violate reporting requirements, they face serious Fair Credit Reporting Act violation penalties.

We at Hays Cauley, P.C. see how these violations harm hardworking families across our state. Understanding your legal options can help you recover damages and protect your credit future.

Understanding FCRA Violations in South Carolina

Common Types of FCRA Violations by Credit Reporting Agencies

Credit reporting agencies violate federal law through systematic failures that harm South Carolina consumers daily. The three major bureaus-Equifax, Experian, and TransUnion-process hundreds of millions of transactions each day, which creates massive opportunities for errors that destroy credit scores. These agencies fail to investigate disputes within the required 30-day timeframe, ignore consumer documentation that proves inaccuracies, and continue to report false information after they receive correction requests. Mixed credit files represent another common violation where agencies merge unrelated consumer records, which causes innocent people to inherit someone else’s debts and payment history.

How Employers and Landlords Violate FCRA Requirements

Employers and landlords create widespread FCRA violations through improper background check procedures that cost South Carolina residents jobs and housing opportunities. Many employers pull credit reports without they provide required disclosures or obtain proper written consent from job applicants. Landlords fail to notify rental applicants about adverse decisions based on credit information, which violates notification requirements that could help consumers address credit issues. Property management companies use outdated or incomplete credit data to reject applications without they follow proper dispute procedures when applicants challenge inaccurate information.

Impact on South Carolina Consumers

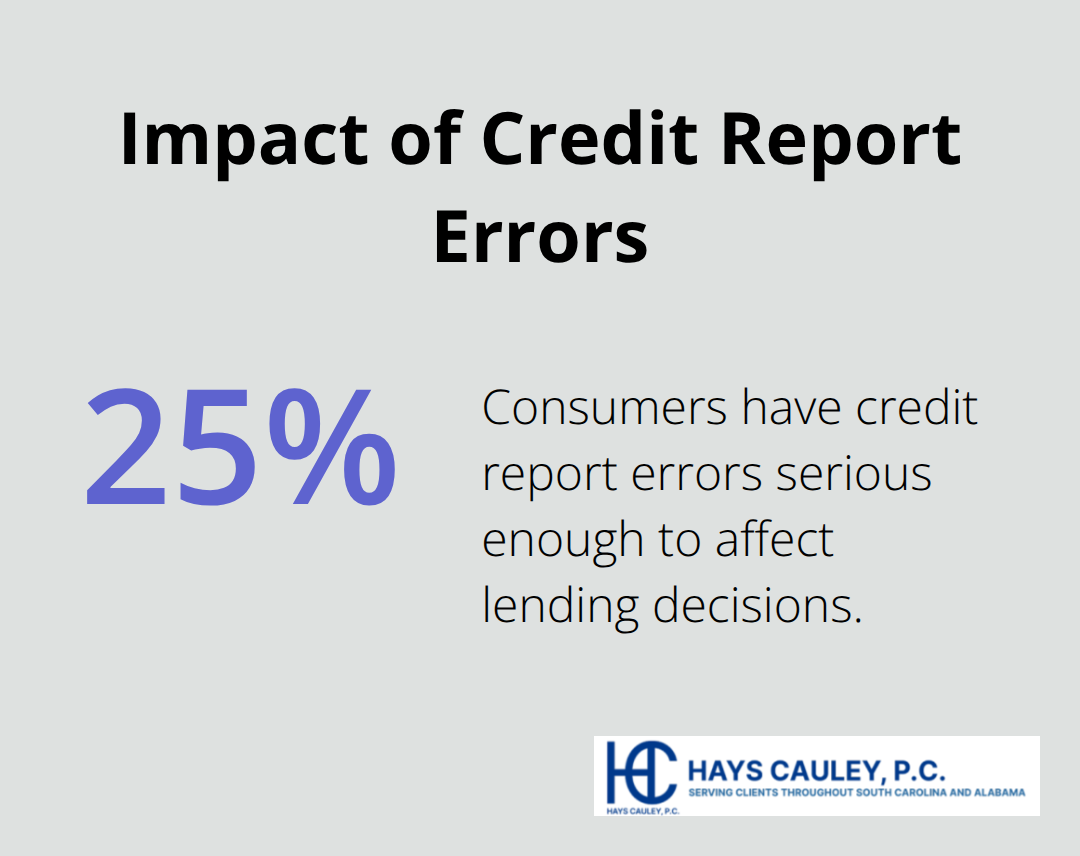

These violations carry devastating financial consequences that extend far beyond credit scores. Studies show that 25% of consumers have credit report errors serious enough to affect lending decisions (translating to higher interest rates that cost families thousands of dollars annually). A single false late payment can drop credit scores by 60 to 110 points, which pushes consumers from prime to subprime lending categories. South Carolina residents face loan denials, increased insurance premiums, and employment rejections based on inaccurate credit information that agencies should have corrected months or years earlier. These violations create a pattern of harm that demands legal accountability and compensation for affected consumers.

Legal Consequences for FCRA Violations

Statutory Damages That Don’t Require Proof of Harm

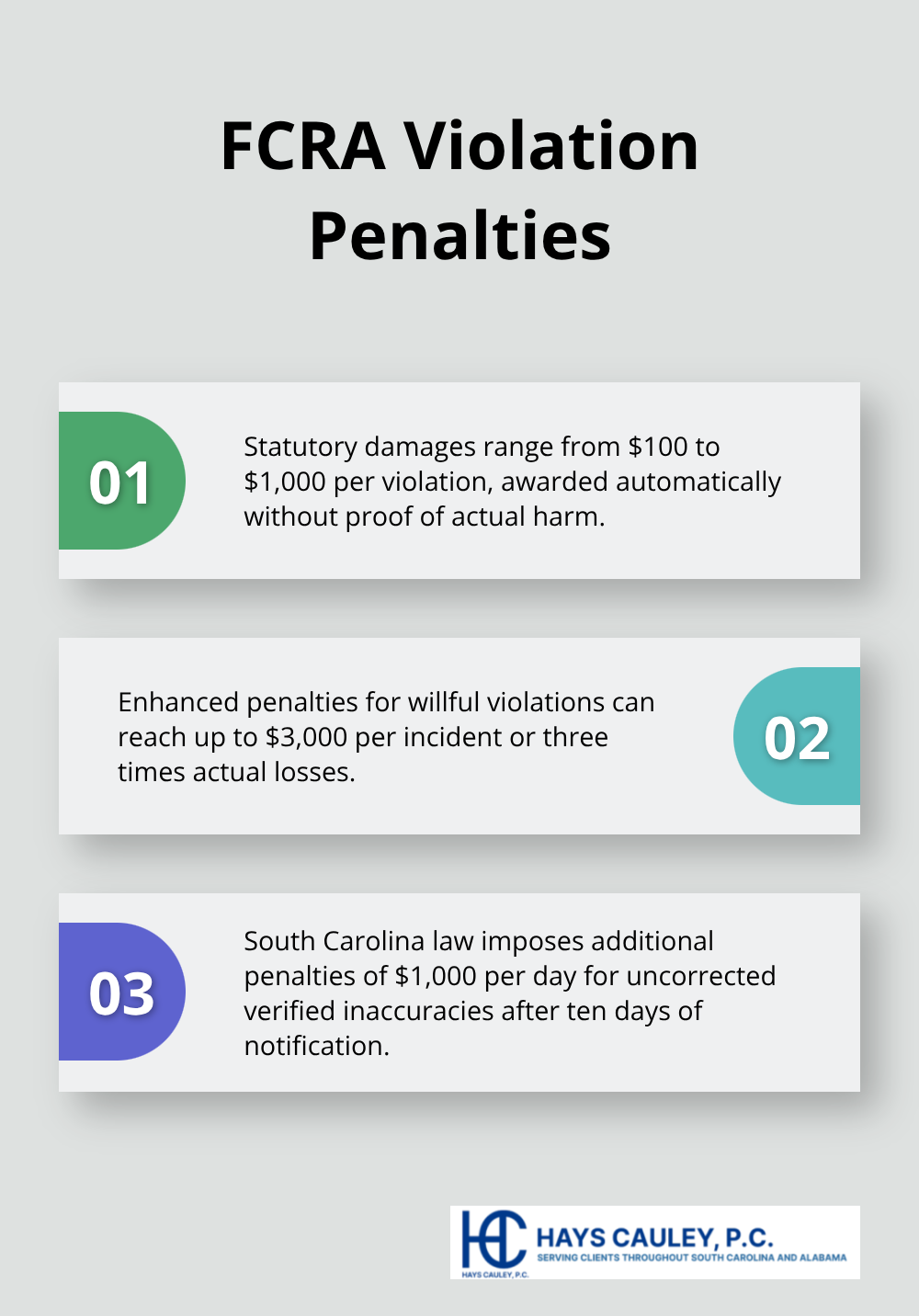

Federal law provides automatic compensation for FCRA violations regardless of whether you can prove actual financial losses. Courts award between $100 and $1,000 per violation as statutory damages, which means South Carolina consumers receive guaranteed compensation when agencies fail to follow proper procedures. These damages apply even when credit report errors don’t directly cause loan denials or higher interest rates. The Federal Trade Commission reports that successful FCRA lawsuits have resulted in class action settlements that exceed $100 million, which demonstrates the significant financial consequences agencies face for widespread violations.

Enhanced Penalties for Willful Violations

When credit agencies knowingly violate FCRA requirements or show reckless disregard for consumer rights, courts impose punitive damages up to three times actual losses or $3,000 per incident. South Carolina law allows additional penalties of $1,000 per day when agencies fail to correct verified inaccuracies within ten days after notification. These enhanced penalties target agencies that ignore dispute letters, continue to report false information after they receive correction documentation, or maintain policies that systematically violate consumer rights. Willful violations often involve repeated failures to investigate disputes or deliberate decisions to prioritize profits over accuracy.

Complete Cost Recovery for Legal Action

The FCRA requires violators to pay your attorney fees and court costs when you win, which makes legal action financially accessible for South Carolina consumers. This fee-shifting provision allows consumers to pursue FCRA claims without upfront legal expenses (as attorneys often work on contingency and know they’ll recover fees from defendants). Courts also award costs for filing fees, document production, and other litigation expenses. This comprehensive cost recovery system levels the playing field against well-funded credit agencies and encourages consumers to enforce their rights.

Maximum Damage Awards Under Federal Law

Federal courts can stack multiple violations to create substantial damage awards that reflect the true harm agencies cause to consumers. Each separate violation (failure to investigate, continued false reporting, improper procedures) generates its own statutory damage award. Recent court decisions show that consumers can recover tens of thousands of dollars when agencies commit multiple violations across different time periods. These cumulative awards send a strong message that agencies must take consumer rights seriously and implement proper procedures to avoid costly litigation.

Understanding these potential recoveries helps you evaluate whether legal action makes sense for your specific situation and prepares you to recognize when agencies violate your fundamental rights as a South Carolina consumer.

Your Rights as a South Carolina Consumer

How to Identify FCRA Violations on Your Credit Report

South Carolina consumers must actively monitor their credit reports to catch violations that agencies hope you’ll miss. Request your free annual reports from annualcreditreport.com and examine every detail for inaccuracies. Look for wrong personal information, accounts that don’t belong to you, incorrect payment histories, and outdated negative information that should have been removed after seven years.

Pay special attention to mixed file errors where agencies merge your information with someone else’s records (which creates false debts and payment problems). The Federal Trade Commission found that one in five consumers have errors on at least one credit report. Regular checks catch problems before they destroy your credit score and financial opportunities.

Steps to Take When Your Rights Are Violated

When you find violations, document everything with screenshots and written records before agencies can change or delete information. File disputes with all three credit bureaus through certified mail to create proof of delivery. Keep copies of all correspondence that includes dispute letters, supporting documentation, and agency responses.

Agencies must investigate within 30 days, but many South Carolina consumers report delays and inadequate responses that violate federal requirements. If agencies fail to correct verified errors or ignore your documentation, these failures create additional FCRA violations that strengthen your legal case and increase potential damage awards.

Time Limits for Filing FCRA Lawsuits

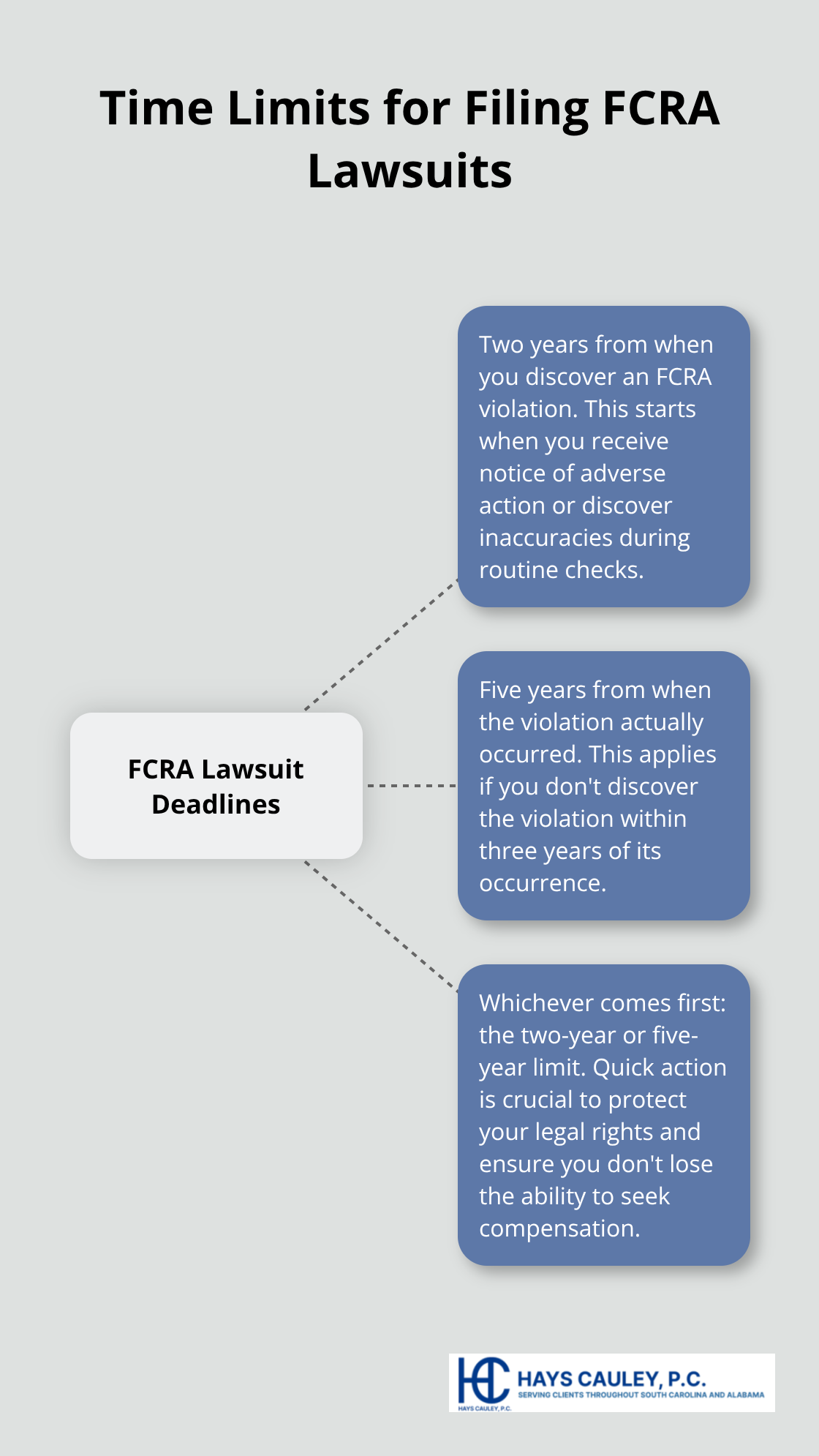

Federal law imposes strict time limits that can destroy your right to compensation if you wait too long to act. You have two years from when you discover an FCRA violation to file a lawsuit, or five years from when the violation actually occurred (whichever comes first).

These deadlines start when you receive notice of adverse action based on your credit report or when you discover inaccuracies during routine checks. South Carolina consumers who delay action often lose their right to statutory damages and attorney fee recovery, even when agencies clearly violated federal requirements. Quick action protects your legal rights and forces agencies to take your complaints seriously rather than hope you’ll give up and accept inaccurate credit reports.

Final Thoughts

Credit agencies count on South Carolina consumers to remain silent about violations because they know most people won’t fight back. This passive approach costs families thousands of dollars in higher interest rates and missed opportunities while agencies profit from inaccurate information. Fair Credit Reporting Act violation penalties exist specifically to change this dynamic and force agencies to prioritize accuracy over convenience.

The two-year deadline for FCRA lawsuits means delays can permanently destroy your right to compensation. When agencies ignore your disputes, continue to report false information, or fail to investigate within 30 days, these violations create legal claims that generate statutory damages. You don’t need to prove actual financial harm to recover compensation under federal law.

We at Hays Cauley, P.C. help South Carolina consumers hold credit agencies accountable through legal action that recovers damages and forces compliance with federal law. Action protects not just your credit score but also sends a message that South Carolina consumers won’t tolerate systematic violations of their rights. Contact us today to discuss your credit report issues and learn about your legal options (we offer free consultations to evaluate your case).