Synthetic Identity Theft SC: How It Hurts Your Credit And How To Fight Back

Synthetic identity theft in SC is growing faster than traditional identity theft, making it one of the hardest fraud schemes to catch. Criminals build fake identities using a mix of real and fabricated information, then open accounts and rack up debt in your name.

At Hays Cauley, P.C., we help South Carolina residents fight back against this threat. This guide walks you through what synthetic identity theft looks like, how it damages your credit, and the concrete steps you can take right now to protect yourself.

How Criminals Build Synthetic Identities

The Anatomy of a Fake Identity

Synthetic identity theft works by pairing a stolen Social Security number with completely fabricated personal information. A criminal takes a real SSN, often purchased on the dark web, then invents a name, date of birth, and address to create what Thomson Reuters calls a Frankenstein ID. This isn’t identity theft in the traditional sense because no real person’s identity is stolen. Instead, fraudsters manufacture an entirely new person on paper.

The Social Security Administration randomized SSN issuance in 2011, which was meant to improve security, but it actually made detection harder. Before randomization, lenders could spot invalid SSNs through sequential validity checks. Now those checks don’t work, so fake SSNs slip past initial fraud screening more easily.

How Fraudsters Build Credibility Over Time

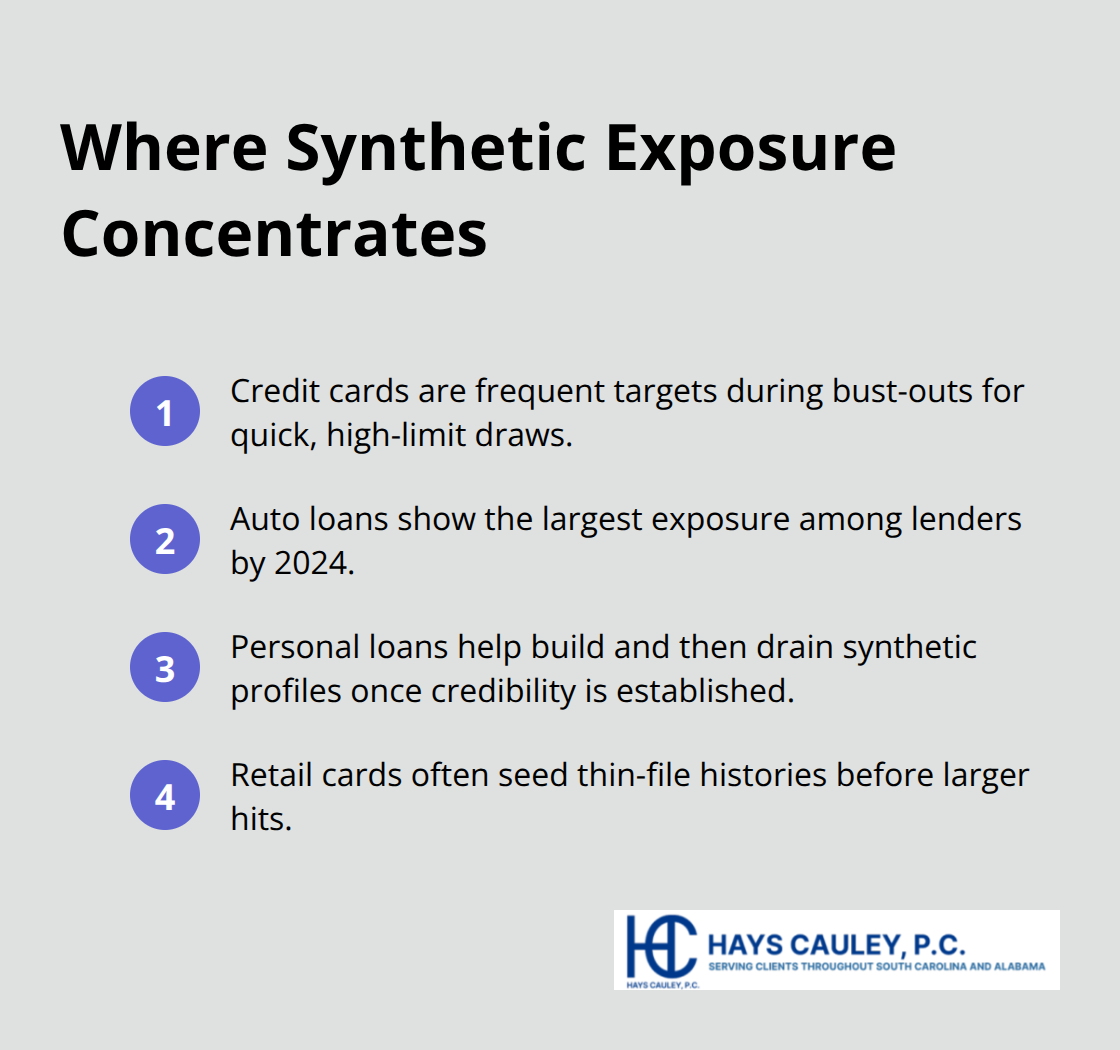

Criminals don’t rush this process. They spend months or even years building credibility by making small purchases, paying bills on time, and establishing a legitimate-looking credit history across multiple accounts. Only after this patient cultivation do they execute what’s called a bust-out, maxing out credit cards and loans before disappearing. According to TransUnion, lenders faced about 3.3 billion dollars in synthetic identity exposure across credit cards, auto loans, personal loans, and retail cards by the end of 2024, with auto loans showing the largest exposure.

Why Detection Remains Nearly Impossible

The reason synthetic identity theft is so difficult to catch comes down to one fundamental problem: there’s no real victim complaining during the fraud. With traditional identity theft, a person notices fraudulent charges on their own account and reports them. With synthetic fraud, the fake person doesn’t exist to complain, so accounts stay open for months or years before anyone catches on.

When delinquencies finally appear on credit reports, they attach to your SSN, dragging down your credit score even though you never authorized the accounts. Thomson Reuters reports that over 80 percent of all new-account fraud now stems from synthetic identities, making it the fastest-growing fraud type in the country. Detection becomes further complicated because synthetic identities create split credit files that are difficult to separate from your legitimate history once discovered.

Many fraudsters operate multiple synthetic identities simultaneously as a full-time criminal operation, compounding the scale of the problem across the financial system. The challenge isn’t identifying obvious red flags anymore. It’s recognizing that a perfectly normal-looking credit history might not belong to a real person at all-which means your credit report could contain accounts you never opened, and you might not know until damage has already occurred.

How Synthetic Identity Theft Wrecks Your Credit

Immediate Damage to Your Credit Score

The moment a fraudster opens an account using your stolen SSN, damage starts accumulating on your credit report. Those fraudulent accounts generate payment histories, credit inquiries, and account balances that attach directly to your SSN. When the criminal eventually defaults on these accounts, the delinquencies and charge-offs drag your credit score down significantly.

TransUnion data shows that lenders faced 3.3 billion dollars in synthetic identity exposure by the end of 2024, meaning this damage is happening to real people across South Carolina right now. Your credit score can drop 50 to 100 points or more depending on how many accounts were opened and how severely they defaulted.

The problem intensifies because you have no control over payment activity on accounts you never authorized. You cannot prevent the damage through normal financial management, no matter how responsibly you handle your own finances.

How Fraudulent Accounts Block Your Access to Credit

Lenders may deny your credit applications, impose higher interest rates on legitimate borrowing, or reject your mortgage application entirely because your credit report now shows multiple defaults and delinquencies. The damage persists on your credit report for seven years from the date of first delinquency, meaning a synthetic identity opened today could harm your borrowing ability well into 2031.

Even after you dispute the fraudulent accounts with credit bureaus, the process takes 30 days minimum, and disputes don’t always succeed immediately. Many people find themselves stuck paying higher rates on car loans, mortgage refinances, or personal loans because lenders see a credit history full of defaults they don’t understand.

The Long-Term Financial Toll

If the synthetic account was used to open a loan or credit card with a high balance, you could face debt collection calls for accounts you never created. You must repeatedly prove you’re not liable while the psychological stress mounts. The fraudulent accounts can remain active for months or years before you discover them, extending the period during which new damage accumulates.

This extended timeline means that by the time you detect the fraud, multiple creditors have already reported negative information to the bureaus. The longer accounts stay open, the more interest and fees accrue, and the deeper the damage cuts into your credit profile. Understanding how quickly synthetic identity theft destroys your creditworthiness makes the detection and response steps that follow absolutely essential to limiting losses.

How to Detect and Fight Synthetic Identity Theft: Serving South Carolina, Including Greenville, Columbia and Charleston

Monitor Your Credit Reports Every Four Months

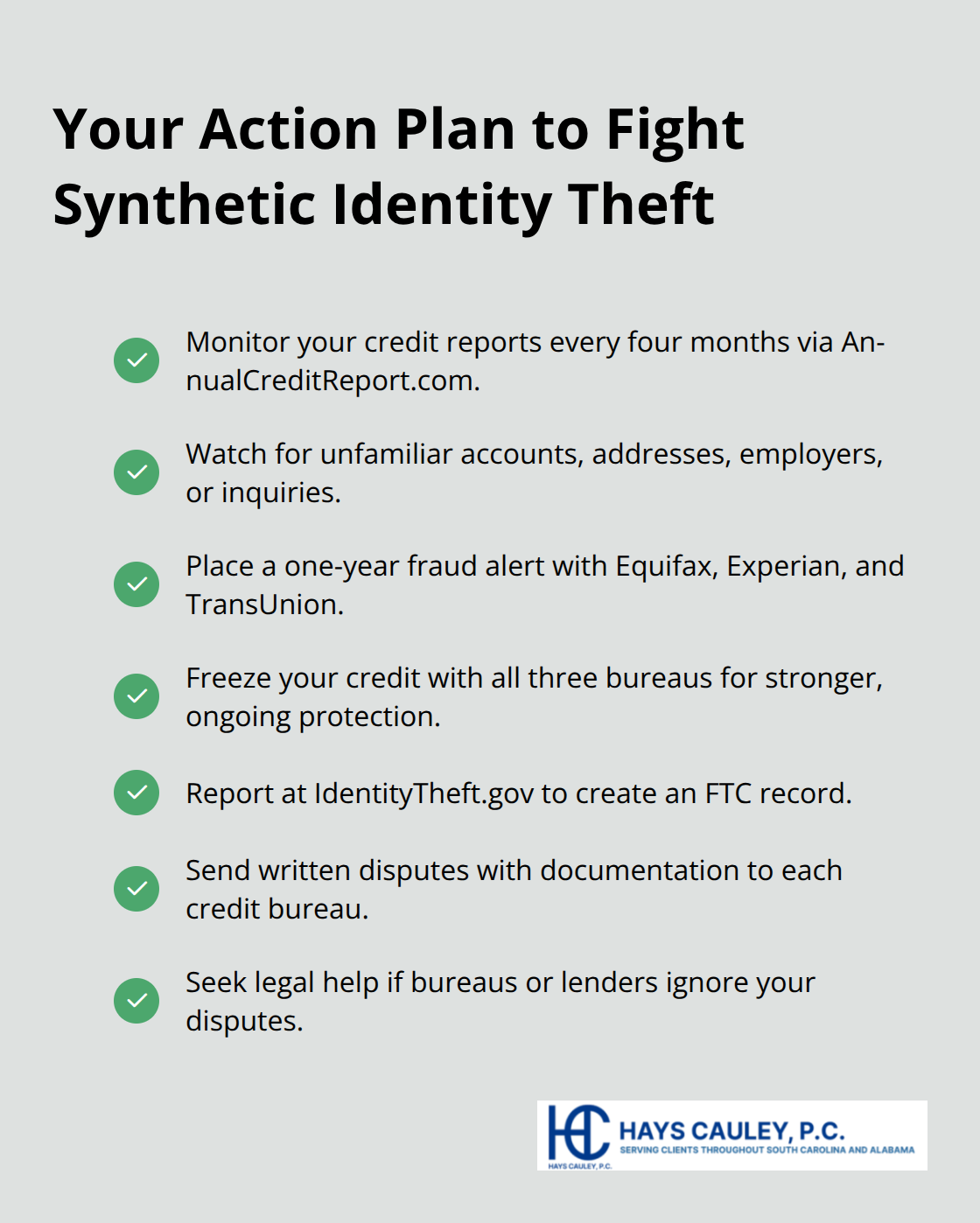

Start checking your credit reports immediately, not once a year. Pull your free reports from AnnualCreditReport.com every four months rather than waiting until you suspect fraud. This staggered approach gives you three complete views of your credit file annually, making it much harder for fraudsters to operate undetected for extended periods. When you review each report, look specifically for unfamiliar addresses, employers, or credit inquiries that don’t match your actual financial activity. Cross-check every entry against your real history.

Unfamiliar accounts, sudden inquiries from lenders you never contacted, or statements arriving at addresses you don’t recognize signal that synthetic fraud is already happening. Your credit score itself tells a story. A sudden, unexplained drop of 50 points or more warrants immediate investigation, not a wait-and-see approach. According to TransUnion, lenders faced 3.3 billion dollars in synthetic identity exposure by the end of 2024, meaning the threat is active right now across South Carolina. The faster you catch fraudulent accounts, the sooner you can limit the damage spreading across your credit file.

Place Fraud Alerts and Credit Freezes Immediately

The moment you spot suspicious activity, place a fraud alert with all three credit bureaus-Equifax, Experian, and TransUnion. A fraud alert is temporary, lasting one year and requiring renewal, but it forces creditors to contact you before opening new accounts in your name. This single step stops many bust-outs cold because fraudsters want speed and minimal friction.

If you want stronger protection, a credit freeze blocks new accounts entirely and costs nothing to place with any of the three bureaus. Freezes remain in place indefinitely until you lift them, making them far superior to alerts for long-term defense. After placing alerts or freezes, report the fraud at IdentityTheft.gov to create an official record with the Federal Trade Commission.

Dispute Fraudulent Accounts with Credit Bureaus

Send written disputes to each credit bureau listing the fraudulent accounts and attach your IdentityTheft.gov report as evidence. Federal law requires bureaus to investigate within 30 days and remove accounts that cannot be verified as legitimate. If bureaus fail to act or lenders refuse to remove accounts after your disputes, you may need legal assistance to enforce your rights under federal credit reporting laws.

Many people try to handle disputes alone and fail because they don’t know the legal leverage available to them. A consumer protection law firm that handles identity theft cases knows exactly which federal statutes apply to your situation and how to force compliance from creditors and bureaus that ignore consumer disputes. Hays Cauley, P.C. is a consumer protection law firm dedicated to helping consumers with credit reporting and identity theft issues, and we can help you pursue federal remedies if disputes fail or the damage is extensive.

Final Thoughts

Synthetic identity theft in SC represents one of the fastest-growing threats to your financial security, and the statistics back this up. Over 80 percent of all new-account fraud now stems from synthetic identities, with lenders facing billions in losses annually. The danger lies in how quietly this fraud operates-unlike traditional identity theft where you notice fraudulent charges on your own account, synthetic fraud creates phantom accounts attached to your SSN that you may never know exist until damage has already accumulated.

You control your response starting today. Pull your free credit reports from annualcreditreport.com every four months and scrutinize them for unfamiliar accounts, addresses, or inquiries. A sudden credit score drop signals trouble and demands immediate action, so place fraud alerts with all three credit bureaus the moment you spot suspicious activity, then follow up with a credit freeze for stronger protection. Report the fraud at IdentityTheft.gov to create an official FTC record, then send written disputes to each bureau with your IdentityTheft.gov report attached as evidence.

If credit bureaus ignore your disputes or lenders refuse to remove fraudulent accounts, you need legal help. We at Hays Cauley, P.C. are a consumer protection law firm dedicated to helping consumers with credit reporting and identity theft issues, and we know which federal statutes apply to your situation and how to force compliance from creditors and bureaus that ignore consumer disputes. Contact Hays Cauley, P.C. today to discuss your case and explore your options for pursuing federal remedies when disputes fail or damage is extensive.