Medical Debt and the Fair Credit Reporting Act Explained in South Carolina

Medical debt is a growing concern for many South Carolina residents, affecting their financial stability and credit scores.

The Fair Credit Reporting Act (FCRA) plays a crucial role in how medical debt is reported and managed on credit reports.

At Hays Cauley, P.C., we understand the complexities of the Fair Credit Reporting Act and medical debt, and we’re here to help you navigate these challenges.

What Is Medical Debt in South Carolina?

Definition and Prevalence

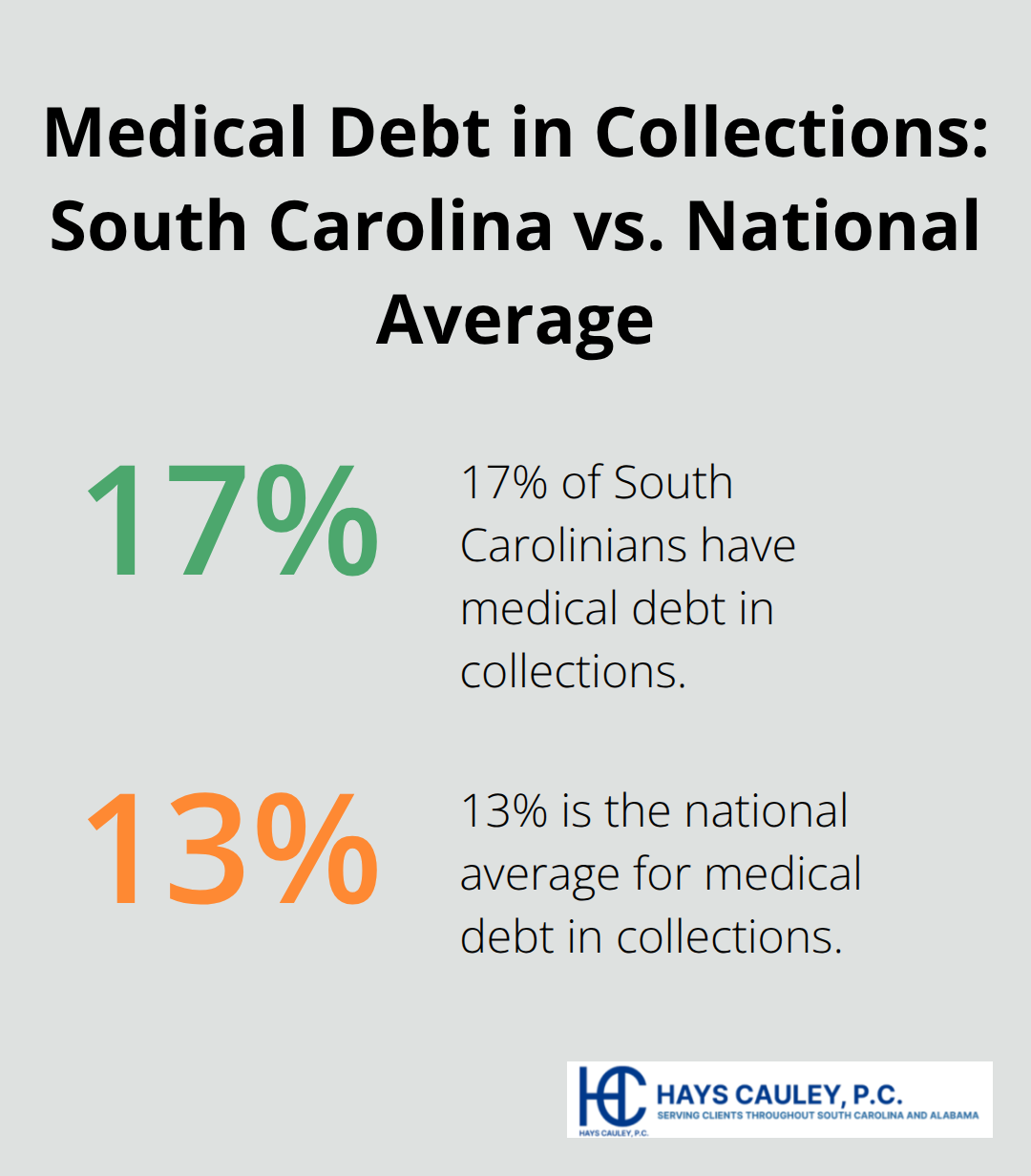

Medical debt refers to unpaid healthcare bills that burden many South Carolina residents. A 2022 Urban Institute study revealed that about 17% of South Carolinians have medical debt in collections, which exceeds the national average of 13%.

Common Causes

Several factors contribute to medical debt accumulation in South Carolina:

- High Deductibles and Out-of-Pocket Costs: A 2021 Kaiser Family Foundation report found that the average deductible for employer-sponsored health plans in South Carolina was $1,669 (a 55% increase from 2011).

- Unexpected Medical Emergencies: A single hospital stay can cost thousands of dollars. The Healthcare Cost and Utilization Project reports that the average cost of a 3-day hospital stay in South Carolina is approximately $30,000.

- Lack of Insurance Coverage: The U.S. Census Bureau reported that 10.8% of South Carolinians were uninsured in 2021, which leaves them vulnerable to high medical costs.

Impact on Residents

Medical debt can severely affect South Carolina residents:

- Financial Stress: It often leads to damaged credit scores and even bankruptcy. A 2019 study by the American Journal of Public Health found that 66.5% of all bankruptcies were tied to medical issues.

- Delayed Treatment: A 2022 Gallup poll revealed that 38% of Americans postponed medical treatment due to cost concerns, which potentially worsens health outcomes and increases long-term healthcare expenses.

Addressing Medical Debt

South Carolina residents can take several steps to tackle medical debt:

- Review Bills Carefully: The Medical Billing Advocates of America estimates that up to 80% of medical bills contain errors. Thorough review can identify and dispute these errors.

- Negotiate with Providers: Many hospitals offer financial assistance programs or discounts for uninsured patients. Patients should not hesitate to discuss their financial situation with healthcare providers.

- Consider Payment Plans: Some providers offer interest-free payment plans to help manage large medical bills over time. This option can make debt repayment more manageable.

- Seek Legal Advice: Professional legal counsel can help individuals understand their rights and options when dealing with medical debt collectors.

The Fair Credit Reporting Act (FCRA) plays a significant role in how medical debt affects credit reports and scores. Understanding this act is essential for South Carolina residents who want to protect their financial health while managing medical debt.

How the FCRA Protects You from Medical Debt

Understanding the Fair Credit Reporting Act

The Fair Credit Reporting Act (FCRA) is a federal law that governs how credit reporting agencies handle your information. This law is particularly important for South Carolina residents dealing with medical debt.

FCRA Rules for Medical Debt Reporting

The FCRA establishes strict guidelines for the reporting of medical debt on credit reports. Credit bureaus must adhere to a 180-day waiting period before they can add medical debt to your credit report. This grace period allows consumers time to resolve insurance issues or establish payment plans.

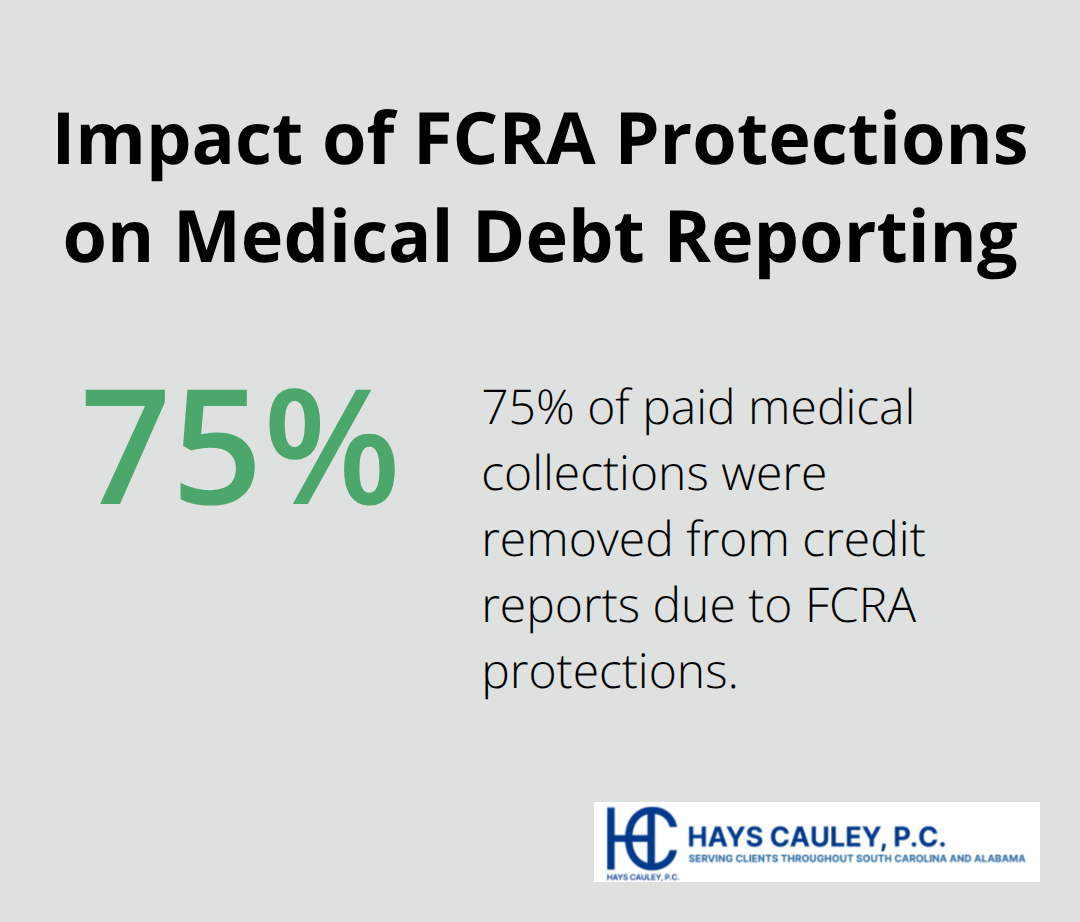

A Consumer Financial Protection Bureau study (conducted in 2020) revealed that medical collections appeared on 43 million credit reports. However, the FCRA’s protections resulted in the removal of approximately 75% of these medical collections once they were paid off.

Your Rights Under the FCRA

The FCRA provides specific rights to consumers regarding medical debt on their credit reports:

- Dispute Inaccurate Information: The Federal Trade Commission reports that 1 in 5 consumers have an error on at least one of their credit reports. You have the right to challenge these inaccuracies.

- Free Annual Credit Reports: You can obtain one free credit report from each major bureau every year (through annualcreditreport.com). This allows you to check for any medical debt errors.

- Timely Investigations: If you find an error, credit bureaus must investigate and respond within 30 days. The National Consumer Law Center states that 70% of credit report disputes result in some modification to the credit report.

Recent Changes to FCRA Medical Debt Reporting

In 2022, the three major credit bureaus announced significant changes to medical debt reporting:

- Paid medical collection debt no longer appears on credit reports.

- The grace period for reporting unpaid medical debt increased from 180 days to one year.

- Starting in 2023, medical collection debt under $500 will not appear on credit reports.

These changes affect an estimated 70% of medical collection debt, providing substantial relief to millions of consumers.

The Impact of FCRA Protections

The FCRA’s protections have far-reaching effects on consumers dealing with medical debt. By extending grace periods and removing certain debts from credit reports, the FCRA helps many South Carolina residents maintain better credit scores despite facing medical financial challenges.

These protections underscore the importance of understanding your rights under the FCRA when managing medical debt. The next section will explore specific strategies you can use to exercise these rights and address medical debt issues on your credit report.

How to Exercise Your FCRA Rights in South Carolina

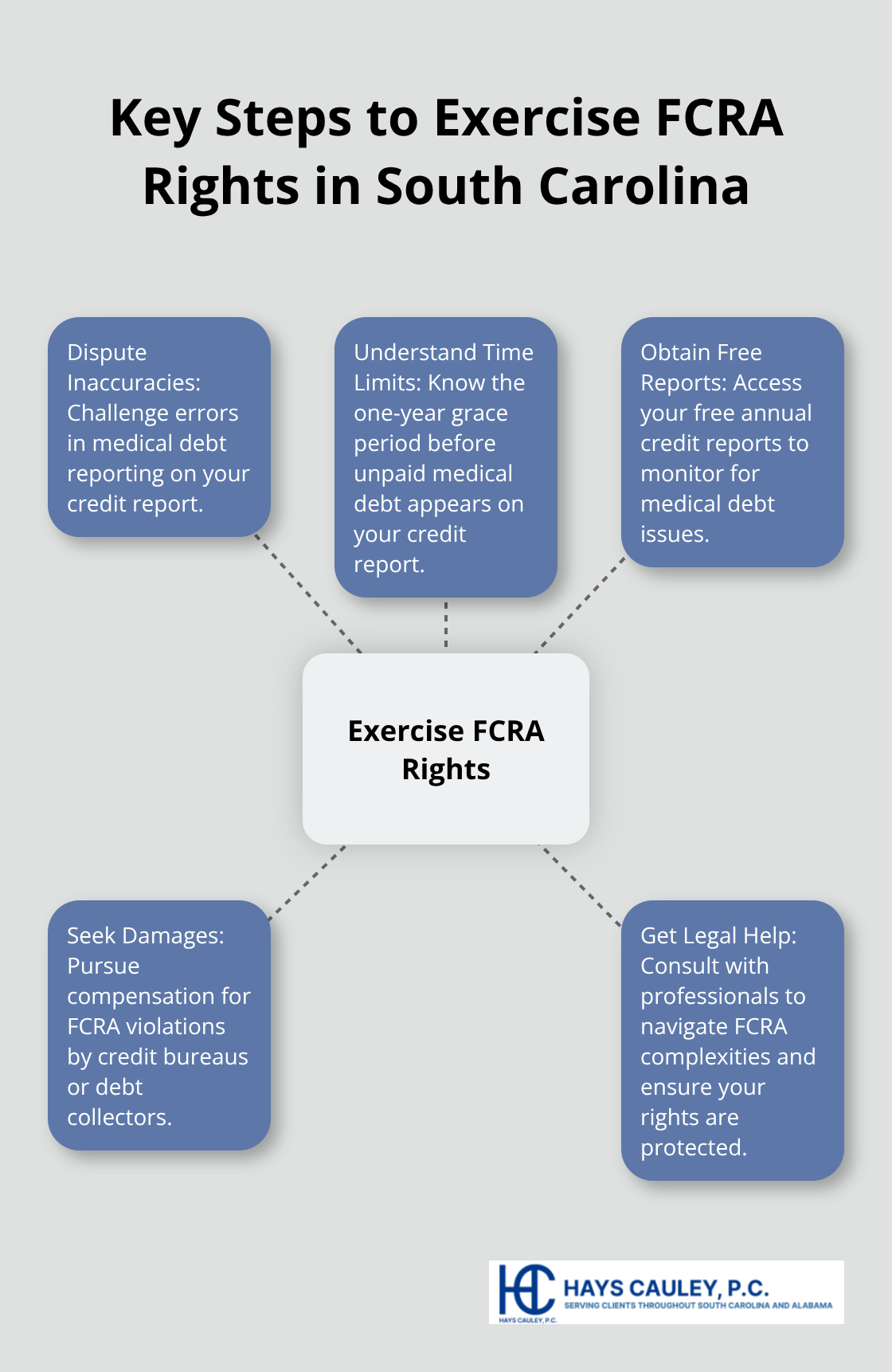

Dispute Inaccurate Medical Debt Information

The Fair Credit Reporting Act (FCRA) empowers South Carolina residents to challenge errors in their medical debt reporting. A Federal Trade Commission study found that 1 in 5 consumers discovered errors on their credit reports that could affect their credit scores. To dispute inaccuracies:

- Write to the credit bureau and clearly identify the error.

- Include supporting documents (e.g., payment records, insurance statements).

- The bureau must investigate within 30 days and remove incorrect information.

A Consumer Financial Protection Bureau report indicates that credit bureaus resolve about 95% of disputes within the required timeframe, highlighting the effectiveness of this process.

Understand Time Limits for Medical Debt Reporting

The FCRA sets specific time limits for reporting medical debt. As of 2022, credit bureaus must wait one year before adding unpaid medical debt to your credit report. This extended grace period (up from the previous 180 days) allows more time to resolve insurance issues or establish payment plans.

Paid medical collection debt no longer appears on credit reports, providing immediate relief once you settle the debt. Starting in 2023, medical collection debt under $500 will not appear on credit reports at all, potentially benefiting millions of consumers.

Obtain Free Credit Reports

You have the right to one free credit report from each major bureau annually through annualcreditreport.com. Due to the COVID-19 pandemic, you can now access free weekly online reports through December 2023. Regular checks allow you to spot and address medical debt issues promptly.

A Consumer Financial Protection Bureau survey revealed that only 1 in 5 consumers check their credit reports annually. Increasing this frequency can better protect your credit score from medical debt impacts.

Seek Damages for FCRA Violations

If a credit bureau or medical debt collector violates your FCRA rights, you can pursue damages. The National Consumer Law Center reports that consumers who successfully sue for willful FCRA violations can receive between $100 to $1,000 in statutory damages (plus actual damages and attorney fees).

Utilize Professional Legal Assistance

Navigating the complexities of the FCRA and medical debt can prove challenging. Professional legal counsel can help you understand your rights under Fair Credit Reporting Act Section 609. They can guide you through the dispute process, ensure compliance with FCRA regulations, and represent you in case of violations.

Final Thoughts

Medical debt poses a significant challenge for many South Carolina residents. The Fair Credit Reporting Act (FCRA) provides valuable protections for consumers dealing with medical debt on their credit reports. These protections include extended grace periods and the removal of certain debts from credit reports, which offer substantial relief to those facing medical financial burdens.

The FCRA empowers consumers to dispute inaccuracies, obtain free credit reports, and seek damages for violations. Recent changes to FCRA medical debt reporting rules further benefit consumers, with paid medical collection debt no longer appearing on credit reports (and debts under $500 soon to be excluded). Regular credit report checks and prompt action on errors can significantly impact your financial health.

At Hays Cauley, P.C., we help South Carolina residents understand and exercise their rights under the Fair Credit Reporting Act for medical debt issues. Our consumer protection law firm focuses on credit reporting, identity theft, and debt-related matters. We can guide you through the dispute process, ensure FCRA compliance, and represent you if your rights are violated.