FCRA Investigation Steps: What to Expect When Your File Is Opened

A credit report error can tank your score and cost you thousands in higher interest rates. When you file a dispute, the Fair Credit Reporting Act requires credit bureaus to investigate your claim within 30 days.

Understanding the FCRA investigation steps helps you know what happens next and protects your rights throughout the process. We at Hays Cauley, P.C. guide South Carolina residents through these disputes every day.

What Triggers an FCRA Investigation

File a Formal Dispute With Proper Documentation

A dispute does not automatically trigger an investigation-you must file it correctly. The Consumer Financial Protection Bureau reports that about 1 in 5 credit reports contain errors, yet most people never challenge them. When you spot an inaccuracy, file a formal dispute with the credit bureau or furnisher, clearly identifying the exact item (account balance, account number, payment status) and attaching supporting documents like bank statements, receipts, or creditor letters. Vague disputes receive less favorable treatment than well-documented ones, so specificity matters. The credit bureau must send your dispute to the furnisher within one business day, starting the clock on their investigation obligation.

Build Strong Evidence for Identity Theft Cases

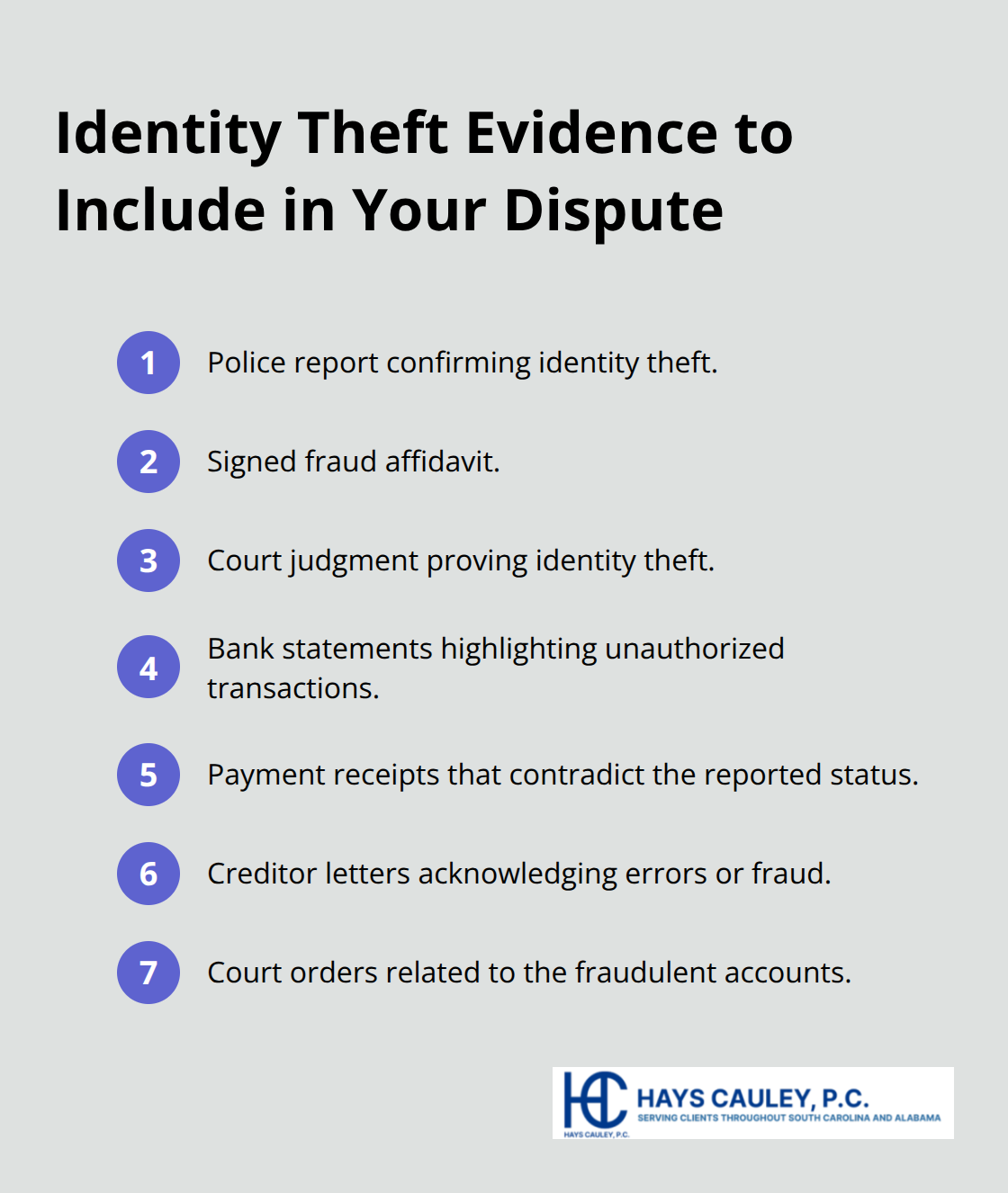

Identity theft cases follow a different path and require additional proof. If fraudulent accounts appear on your file, you must gather concrete evidence: police reports, fraud affidavits, and any court judgments proving identity theft. These documents carry weight because furnishers must actually review their records during investigation-they cannot simply assume data is correct. A court judgment proving identity theft can eliminate fraudulent accounts from your file entirely. The specificity of your supporting evidence (bank statements, payment receipts, creditor letters, court orders) strongly affects investigation speed and outcomes.

Challenge Unauthorized Inquiries Immediately

Unauthorized inquiries also warrant attention, though they trigger a separate process. Hard inquiries from creditors you never authorized signal potential fraud and require immediate dispute action with documentation showing you never applied for that account. Furnishers verify claims by reviewing internal systems, cross-checking dispute materials against their records, and contacting the original creditor or collection agency when needed. This verification process means your evidence directly influences how thoroughly the furnisher investigates your claim. The stronger your documentation, the faster furnishers complete their review and report results back to the credit bureau.

The FCRA Investigation Process: What Happens After You File, Serving South Carolina, Including Greenville, Columbia and Charleston

The Credit Bureau’s One-Business-Day Obligation

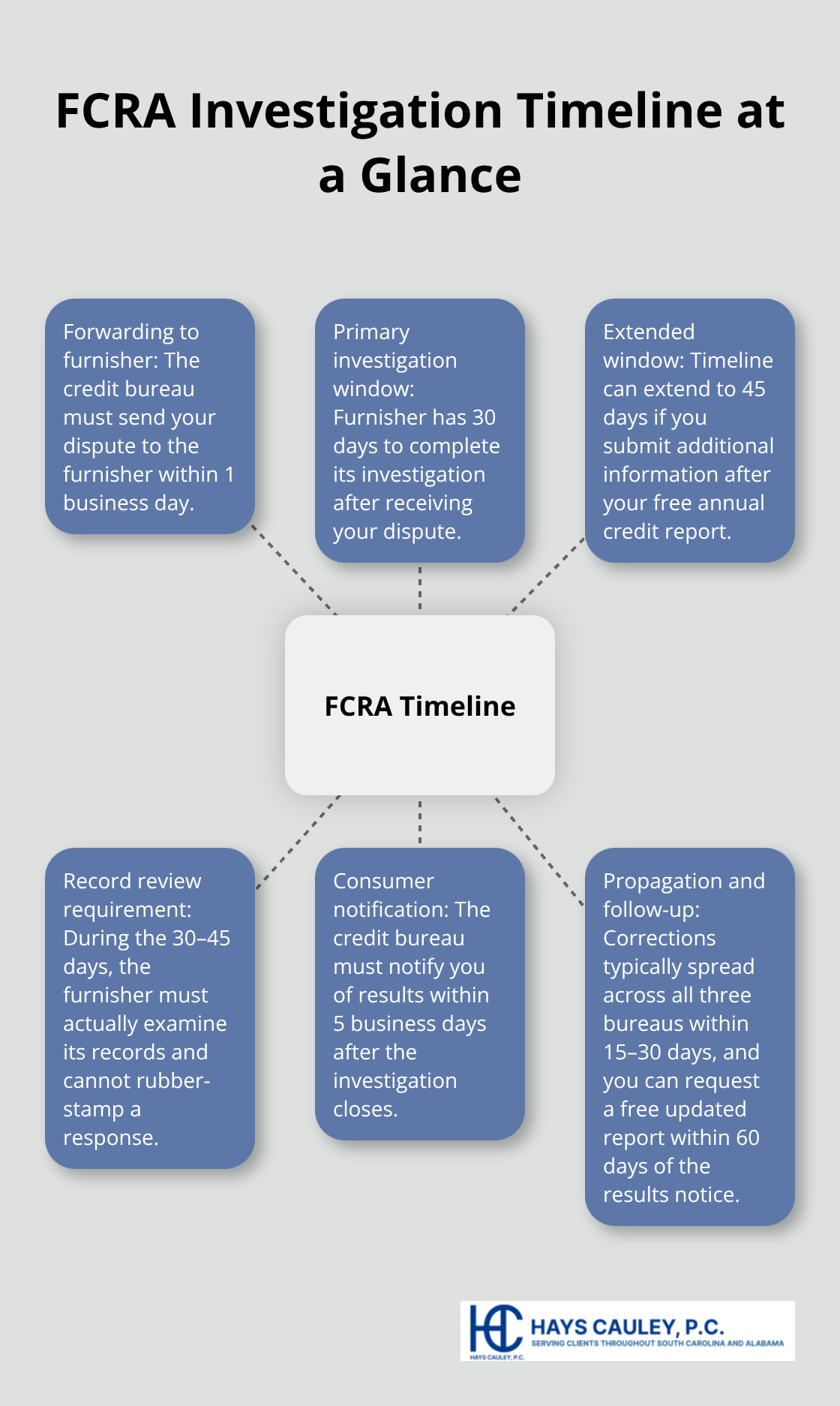

Once your dispute lands with the credit bureau, they have one business day to forward it to the furnisher-and this is where most disputes either gain momentum or stall. The furnisher then has 30 days to investigate, though this timeline extends to 45 days if you submitted additional information after pulling your free annual credit report. During those 30 to 45 days, the furnisher must actually examine their records; they cannot simply assume the data is correct or rubber-stamp a response. The Consumer Financial Protection Bureau’s examination procedures make clear that furnishers must review internal systems, cross-check your dispute materials against what they have on file, and contact the original creditor or collection agency if needed.

This is not a box-checking exercise.

How Furnishers Verify Your Dispute

The furnisher’s investigation focuses on whether the disputed item matches their records, including current balance, payment status, and account details. If you submitted strong documentation (bank statements, payment receipts, creditor letters, court orders), the furnisher must compare your evidence against what they hold. Vague disputes receive slower, less thorough treatment than well-documented ones, so the quality of your supporting materials directly affects how quickly the furnisher completes their work. The furnisher cannot ignore your dispute or fail to investigate within the legal timeframe without facing enforcement by the Consumer Financial Protection Bureau and consumer lawsuits, with penalties potentially reaching $4,983 per violation as of 2026. That enforcement threat is real, and it means furnishers know they cannot cut corners or delay without legal exposure.

Corrections Spread Across All Three Bureaus

If the furnisher finds the information is inaccurate, they must notify all three credit bureaus so the correction spreads across your entire file, not just one bureau. Corrections typically propagate within 15 to 30 days after the investigation closes, which is why you should pull fresh credit reports to confirm the updates actually posted. If one bureau still shows the old information after corrections, contact that bureau directly with proof of the correction notice to force remediation. The credit bureau must notify you of the results within five business days and provide a copy of your updated credit report. This notification is your official record that the investigation occurred.

What Happens When Furnishers Fail to Investigate

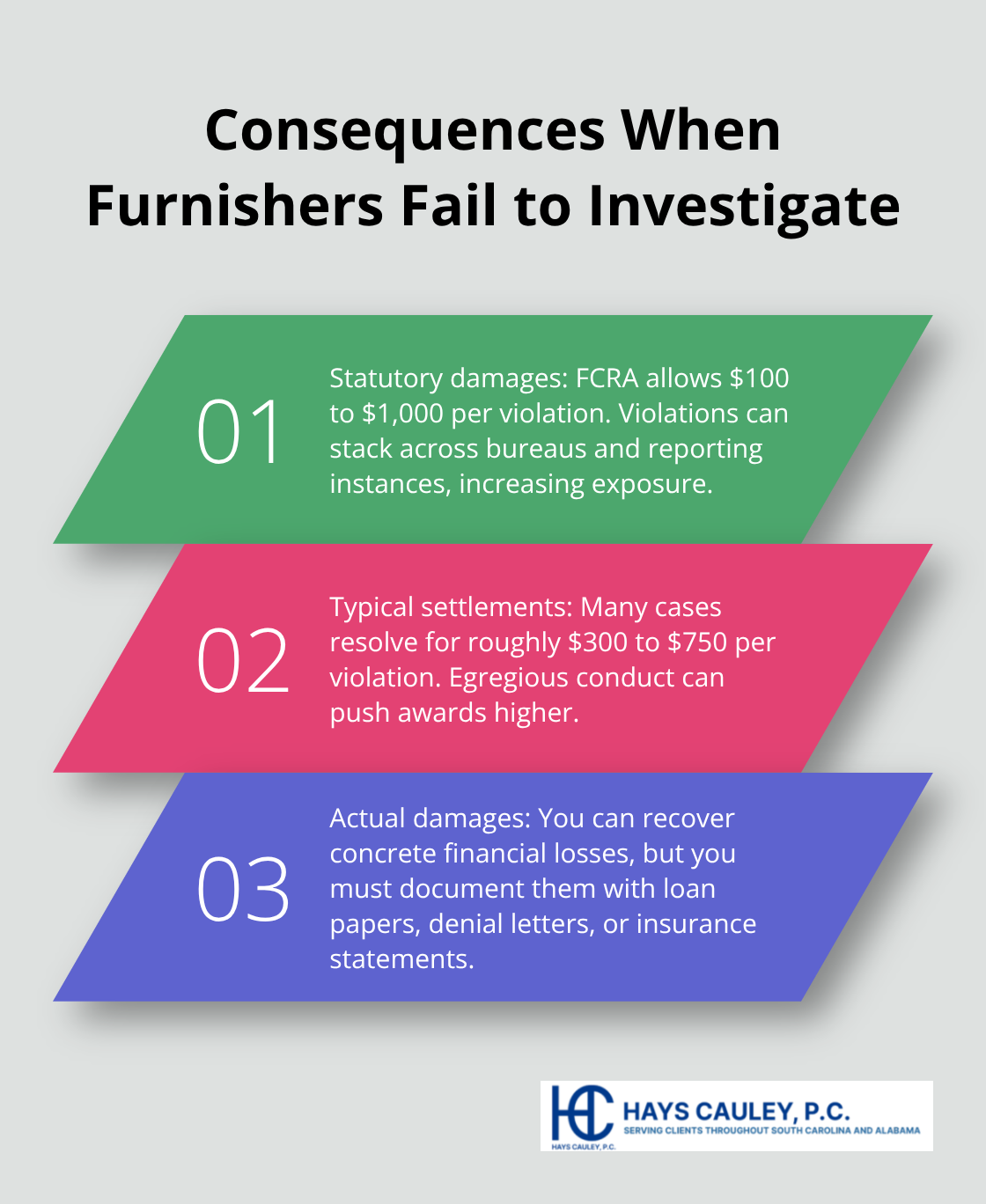

Furnishers who ignore disputes or fail to meet investigation deadlines face real consequences. The CFPB enforces these violations, and consumers can file lawsuits against furnishers that violate FCRA requirements. Statutory damages can reach $100 to $1,000 per violation, and violations can stack-one per bureau, per reporting instance. Settlements have commonly awarded roughly $300 to $750 per violation, with higher awards in more egregious cases. Beyond statutory damages, you can recover actual damages for financial harm caused by the error (higher loan rates, denied credit, increased premiums), though you must document these losses with loan documents, denial letters, or insurance statements.

These remedies exist because the law takes furnisher accountability seriously.

Your rights during this investigation process are substantial, and understanding them positions you to hold furnishers accountable if they fail to investigate properly.

What You Can Demand From Furnishers and Credit Bureaus, Serving South Carolina, Including Greenville, Columbia and Charleston

Written Notice and Updated Credit Reports

The moment a furnisher receives your dispute, you gain concrete rights that most people never use. The Fair Credit Reporting Act requires furnishers to send you written notice of their investigation results within five business days after the investigation closes. This notice must tell you exactly what they found: whether they deemed the information accurate, inaccurate, or could not verify it. You have the absolute right to obtain a free copy of your updated credit report within 60 days of receiving the results notice, and you should pull reports from all three bureaus since corrections sometimes fail to propagate uniformly. If one bureau still displays the old information after 15 to 30 days, contact that bureau with your correction notice and demand they update their file.

Access to Investigation Documentation

Furnishers cannot withhold investigation documentation or results from you under FCRA requirements. If they refuse to provide written notice or your updated report, that refusal itself violates FCRA requirements and creates grounds for legal action. Demand specificity in their response-vague conclusions like “verified as accurate” without explaining what they actually checked are red flags that the furnisher cut corners. According to the CFPB’s 2022 guidance, furnishers cannot demand you submit documents in special formats or through specific channels before they investigate.

Consumer Statements and Dispute Notation

You retain the right to place a consumer statement on your credit report if you disagree with investigation results, though this remedy is weaker than actually correcting the error. A 100-word statement explaining your version of events stays on your file, but lenders and employers often ignore these statements entirely, which is why actual corrections matter far more. This option exists as a safety valve when furnishers refuse to correct inaccurate information, but it should never be your first choice.

Protection Against Retaliation

The FCRA prohibits furnishers from retaliating against you for filing a dispute by continuing to report the disputed item as accurate after they received your challenge. If a furnisher keeps reporting the item unchanged 30 days after your dispute arrived, document this failure with screenshots and written notices, as it demonstrates they either ignored your dispute or failed to investigate. Furnishers who retaliate face statutory damages of $100 to $1,000 per violation, and these violations compound across each bureau that receives the unchanged information. The law treats retaliation seriously because it prevents furnishers from using their reporting power to intimidate consumers into dropping legitimate disputes.

Final Thoughts

An FCRA investigation follows a clear path: you file a dispute with proper documentation, the credit bureau forwards it within one business day, the furnisher investigates within 30 to 45 days, and you receive written results. Throughout these FCRA investigation steps, furnishers must actually examine their records, not simply assume data is correct. If corrections are needed, they spread across all three bureaus within 15 to 30 days.

If investigation results disappoint you, your options depend on what went wrong. Document every step: dates you filed, copies of your dispute, the furnisher’s response, and proof that corrections did not post. These records become evidence if you pursue statutory damages of $100 to $1,000 per violation, plus actual damages for financial harm like higher loan rates or denied credit.

We at Hays Cauley, P.C. help South Carolina residents navigate these disputes and hold furnishers accountable when they violate FCRA requirements. If you have filed a dispute and received unsatisfactory results, or if furnishers are ignoring your challenges entirely, contact us to discuss your options.