Checking credit report errors: A Simple Verification Process

Your credit report directly affects your ability to borrow money, rent an apartment, and sometimes even get hired for a job. Checking credit report errors is essential because mistakes on your report can tank your score and cost you thousands of dollars in higher interest rates.

At Hays Cauley, P.C., we help South Carolina residents from Greenville to Charleston fight inaccurate reporting and protect their financial futures. This guide walks you through spotting errors, disputing them, and knowing your rights.

How to Obtain Your Credit Report: Serving South Carolina, Including Greenville, Columbia and Charleston

Access Your Free Credit Reports

You hold the right to receive free credit reports from Equifax, Experian, and TransUnion at least once every 12 months, and you should pull all three. Many people check only one bureau, which leaves them vulnerable-errors don’t appear uniformly across all three. The Federal Trade Commission reports that through 2026, you can obtain six free credit reports per year from Equifax by visiting their website or calling 1-866-349-5191. All three bureaus also allow you to check your report for free weekly through AnnualCreditReport.com. This means you have no reason to skip regular monitoring of your file. Request reports from all three bureaus at the same time so you can compare them side by side and spot discrepancies immediately.

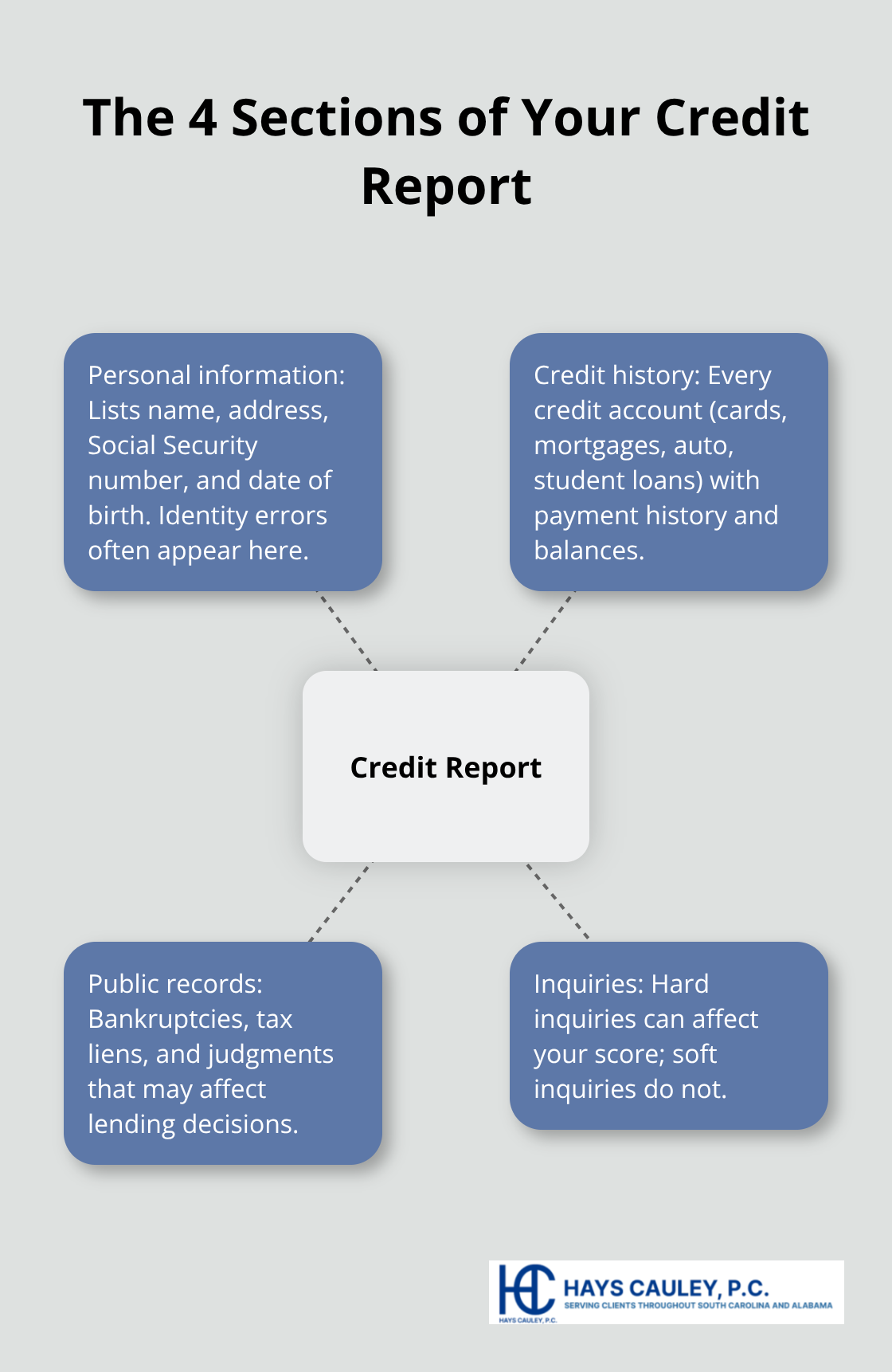

Understand the Four Main Report Sections

Your credit report contains four main sections: personal information, credit history, public records, and inquiries. The personal information section lists your name, address, Social Security number, and date of birth-this is where identity errors hide. The credit history section shows every credit account you have or had, including credit cards, mortgages, auto loans, and student loans, along with payment history and current balances.

Public records include bankruptcies, tax liens, and judgments. Inquiries show which companies have pulled your report, divided into hard inquiries (which affect your score) and soft inquiries (which don’t). Most people skip reading these sections carefully, but errors like duplicate accounts, wrong balances, and fraudulent accounts live there. Spend time reading each section thoroughly rather than just checking your score.

Compare Information Across All Three Bureaus

Equifax, Experian, and TransUnion don’t always report the same information. A creditor might report to one or two bureaus but not all three, meaning an error on one report might not appear on another. One bureau might show a closed account as open while another shows it correctly closed. A furnisher might have reported incomplete information to just one bureau. When you pull reports from all three sources, you catch errors that would otherwise slip through and damage your score with specific lenders. Creditors often pull from different bureaus depending on the type of loan, so an error on your Equifax report could affect you on a mortgage application while your TransUnion report looks clean. Once you’ve identified the errors on your reports, the next step involves taking action through the formal dispute process.

Common Credit Report Errors and How to Spot Them

Personal Information and Identity Errors

Your credit report contains three categories of errors that damage your financial life, and you need to know exactly where to look for them. Personal information errors seem harmless until a creditor denies you a loan because your address is wrong or your name is misspelled, triggering a mismatch during verification. The Fair Credit Reporting Act allows you 30 days to dispute these errors with the credit bureau, and furnishers must investigate within the same window. Check your name, address, phone number, Social Security number, and date of birth against official documents like your driver’s license or tax return.

Mixed files happen more often than you’d think, especially if you share a name with someone else in your area. One South Carolina resident discovered accounts belonging to someone with a nearly identical name on their Equifax report, which dropped their score 87 points until the bureau corrected it.

Account Status and Duplicate Account Errors

Account status errors are equally destructive. Accounts reported as open when you closed them years ago, or accounts marked delinquent when you paid on time, signal deeper problems with how creditors report to the bureaus. TransUnion and Equifax don’t always receive the same information from furnishers, so an account might show as current on one bureau and 60 days past due on another.

Duplicate accounts appear when the same debt gets listed multiple times under slightly different names or account numbers, inflating your debt-to-income ratio and tanking your score. These errors require immediate attention because they distort your financial picture to potential lenders.

Fraudulent Accounts and Unauthorized Inquiries

Fraudulent accounts and unauthorized inquiries represent the most serious errors because they indicate identity theft or unauthorized credit applications. Hard inquiries from accounts you never opened are red flags. The Fair Credit Reporting Act requires creditors to have a permissible purpose before pulling your report, and fraudulent inquiries violate this requirement. Check the inquiry section carefully and note the company name and date for any inquiries you don’t recognize.

If you spot fraud, report it immediately at IdentityTheft.gov to trigger an FTC investigation and receive a personalized recovery plan.

Payment History Errors

Inaccurate payment history errors damage your creditworthiness more than any other mistake because payment history accounts for 35 percent of your credit score. A single account incorrectly marked as 30 days late can lower your score by 100 points or more. Late payment dates that are wrong, accounts showing delinquencies you never had, and current balances that don’t match your statements all belong in this category. Experian must correct these within 30 days of your dispute, and if they fail to investigate properly, you have grounds for legal action under the Fair Credit Reporting Act.

Willful violations carry damages of three times your actual damages or up to $3,000 per incident plus attorney fees. Negligent violations result in actual damages or at least $1,000 per incident plus attorney fees.

Comparing Reports to Identify Errors

Pull all three reports side by side and compare the same accounts across bureaus. Discrepancies between reports point directly to errors that need immediate attention. Equifax, Experian, and TransUnion don’t always report the same information, so an error on one report might not appear on another. A furnisher might have reported incomplete information to just one bureau, or a creditor might report to one or two bureaus but not all three. Once you’ve identified the errors on your reports, the formal dispute process becomes your next step to correct them.

How to Dispute Credit Report Errors Effectively: Serving South Carolina, Including Greenville, Columbia and Charleston

File Your Written Dispute with the Credit Bureau

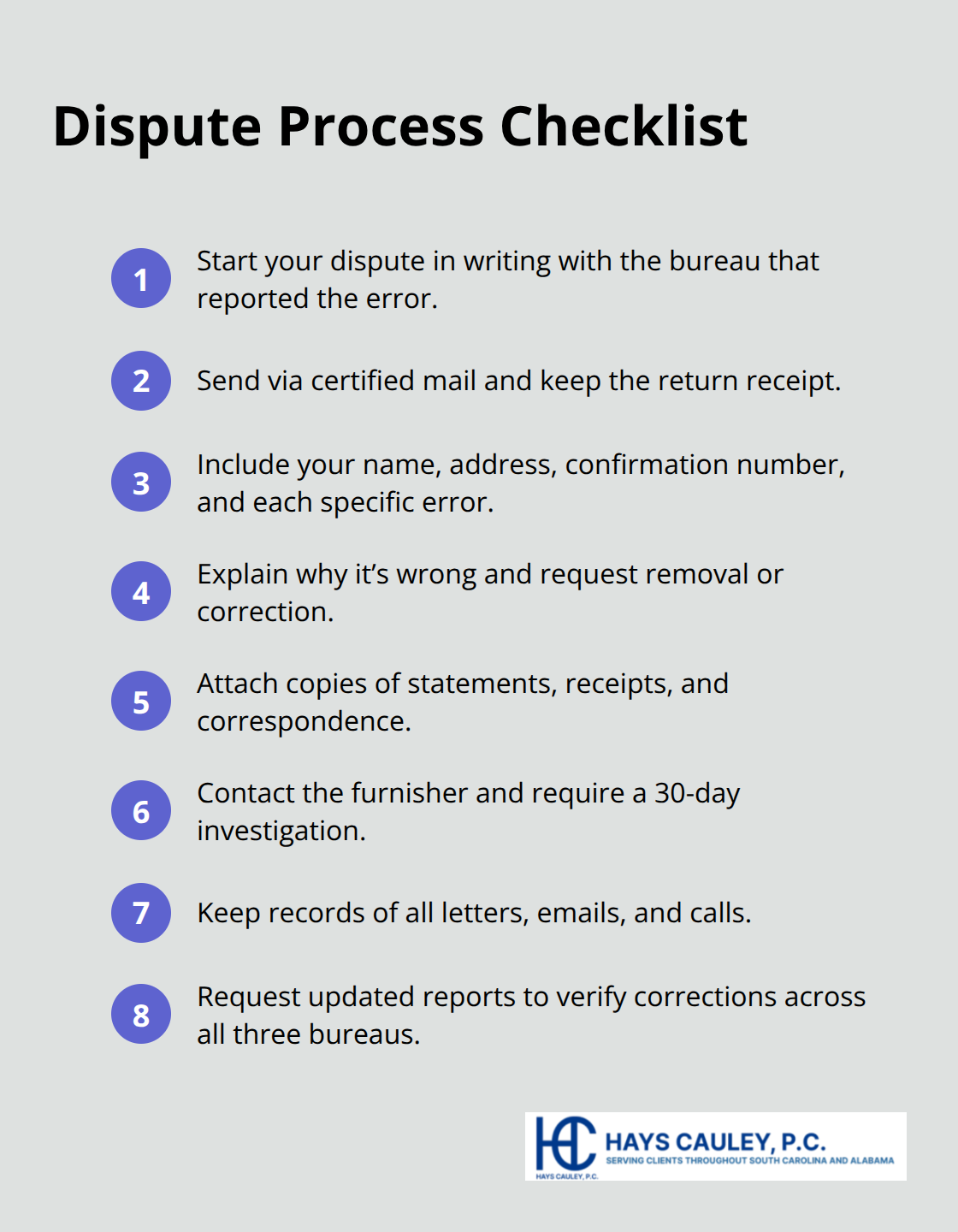

Start your dispute in writing to the credit bureau that reported the error. The Fair Credit Reporting Act mandates that credit bureaus must investigate disputes within 30 days at no charge to you, and they must forward all relevant information to the furnisher-the bank, creditor, or company that originally reported the data. Send your dispute letter via certified mail with return receipt to create a verifiable record that the bureau received it. Address your letter to the specific bureau: Equifax Information Services LLC at P.O. Box 740256, Atlanta, GA 30348; Experian at P.O. Box 4500, Allen, TX 75013; or TransUnion LLC Consumer Dispute Center at P.O. Box 2000, Chester, PA 19016. You can also dispute online or by phone-Experian at 888-397-3742, TransUnion at 800-916-8800, or Equifax at 866-349-5191 but written disputes create stronger documentation for potential legal action.

Your written dispute letter must include your full name and address, your credit report confirmation number (if available), each specific error with the account number, a clear explanation of why the information is wrong, and a request to remove or correct the item. Attach a copy of the relevant report portion with errors circled and copies (not originals) of supporting documents like bank statements, payment receipts, or creditor correspondence that prove your case.

Contact the Furnisher Directly

After disputing with the credit bureau, contact the furnisher directly using the CFPB’s sample dispute letter as your template. Mail this dispute to the furnisher’s address listed on your credit report or the address they provide for disputes. Furnishers must investigate and respond within 30 days of receiving your dispute, and if they find the information inaccurate or cannot verify it, they must update or remove the item and notify all three bureaus to correct your credit reports.

Keep thorough records of every letter, email, and phone call throughout this process. These records protect you if you need to pursue legal action later. If the furnisher determines the information is accurate after investigation, you can request that the bureaus include a brief statement about your dispute in your file, which will appear on all future reports provided to employers, lenders, and other authorized parties.

Monitor Your Investigation and Request Corrections

After the investigation concludes, request updated credit reports from all three bureaus to confirm the corrections appear across your files. If the bureau determines a dispute is frivolous or irrelevant-meaning it lacks sufficient information to investigate-you will receive written notice within five business days, which gives you the opportunity to resubmit with more detail. Comparing your new reports against the originals ensures that all three bureaus reflect the corrections accurately and consistently.

Final Thoughts

Checking credit report errors stops being passive once you understand your rights under the Fair Credit Reporting Act. Credit bureaus must investigate your disputes within 30 days at no cost, and furnishers face real consequences if they ignore your claims-willful violations carry damages of three times your actual losses or up to $3,000 per incident plus attorney fees, while negligent violations result in actual damages or at least $1,000 per incident plus attorney fees. Many disputes resolve quickly when you provide solid documentation and follow proper procedures, but some cases demand more aggressive action when bureaus ignore disputes or furnishers continue reporting false information.

If a credit bureau resists your dispute, claims it’s frivolous without proper investigation, or a furnisher keeps reporting information you’ve already proven wrong, you have grounds to pursue legal claims. These violations happen more often than most people realize, and companies count on consumers not knowing their rights or lacking the resources to fight back. We at Hays Cauley, P.C. help South Carolina residents challenge inaccurate credit reporting and force corrections that should have happened months earlier.

If your dispute stalls or the bureaus deny your claim without investigating properly, contact us to discuss your options. You shouldn’t have to fight alone against companies with teams of lawyers defending their mistakes.