A mistake on your credit report can cost you thousands of dollars in higher interest rates or lost job opportunities. Many South Carolina residents don’t realize they have legal rights under the Fair Credit Reporting Act to challenge inaccurate information.

At Hays Cauley, P.C., we help people fix FCRA data accuracy issues that damage their financial futures. This guide walks you through your rights and the practical steps to dispute errors on your credit report.

What the Fair Credit Reporting Act Actually Protects

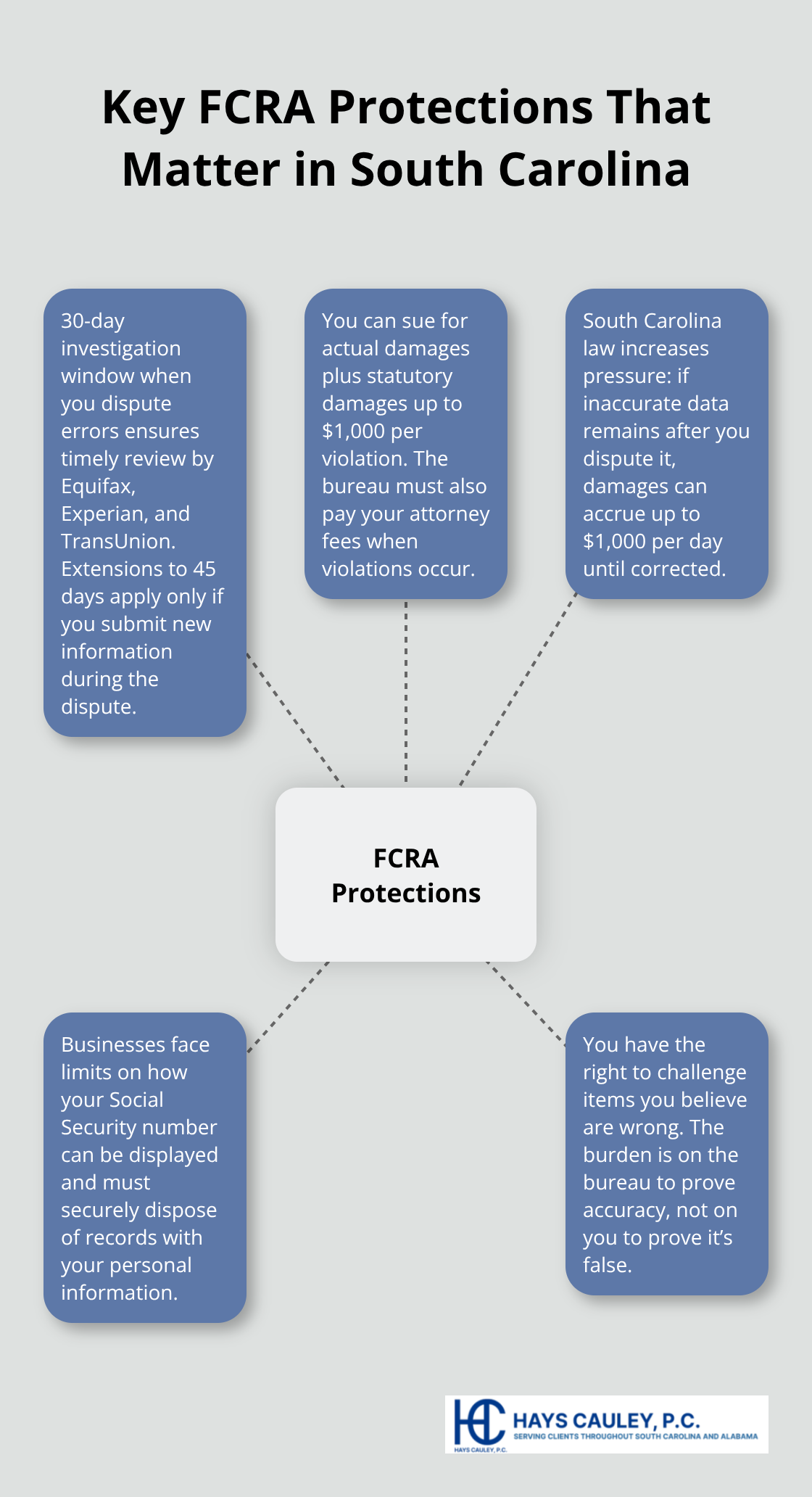

The Fair Credit Reporting Act sets strict rules that credit bureaus and creditors must follow when handling your financial information. The law requires Equifax, Experian, and TransUnion to maintain accurate data and investigate errors within 30 days when you dispute them. If a bureau fails to correct verified inaccuracies, you can sue for actual damages plus statutory damages up to $1,000 per violation, and the bureau must pay your attorney fees. South Carolina law goes further-if a bureau refuses to remove inaccurate information after you’ve disputed it, damages can accrue up to $1,000 per day until the error is corrected. This means a single persistent mistake can trigger serious financial liability for the bureau. The FCRA also restricts how businesses can display your Social Security number and requires them to dispose of records containing your personal information securely.

Most importantly, the law gives you the right to challenge anything on your report that you believe is wrong, and the burden falls on the bureau to prove the information is accurate, not on you to prove it’s false.

How to Access Your Free Credit Reports

You can obtain one free credit report annually from each of the three major bureaus through AnnualCreditReport.com, the official government-backed site. The FTC recommends rotating your requests every four months so you pull one bureau’s report at a time, allowing you to catch errors faster throughout the year. Equifax currently offers six additional free reports per year through 2026 beyond your standard annual report. When you pull your reports, look for unfamiliar accounts, incorrect personal details, payment history that doesn’t match your records, and items that should have aged off after seven years.

What Errors Look Like on Your Report

About 20% of consumers have an error on at least one major report according to FTC data, so finding mistakes is common. Errors may appear on one bureau but not the others, which is why you must review all three separately. Common mistakes include incorrect payment status, mixed-file data from identity theft, duplicate collections accounts, and outdated negative information that should have fallen off your report. Spotting these errors early prevents them from damaging your finances further.

Protecting Your File With a Security Freeze

If you spot identity theft or suspect fraud, you can place a security freeze on your file within five business days of requesting it, and the bureau must provide you a PIN or password within ten days to manage the freeze later. Freezes are free to place, remove, or temporarily lift, giving you control over who accesses your credit information. This protection stops unauthorized creditors from opening accounts in your name while you work to correct the errors on your report.

How to Find and Fight Credit Report Errors

Finding errors on your credit report requires a systematic approach, not a casual scan. Pull all three reports from Equifax, Experian, and TransUnion simultaneously so you can compare them side by side. Look for unfamiliar accounts, incorrect payment statuses, duplicate collections entries, mixed-file data where another person’s information bleeds into your file, and negative items older than seven years that should have aged off. The FTC reported that about 20% of consumers have errors on at least one major report, so take this seriously. Once you spot an error, document it immediately through screenshots, note the exact date you discovered it, and circle the problematic information on a printed copy of your report. This documentation becomes critical evidence if you later need to pursue legal action.

Filing Your Dispute the Right Way

Send written disputes to each bureau that has the error, and do not rely on online dispute tools alone because they often lead nowhere. Use certified mail with return receipt so you have proof the bureau received your dispute. Include a clear written explanation of why the item is inaccurate, copies of supporting documents like account statements or canceled checks, a copy of your report with the errors circled, and a request for reinvestigation. Under South Carolina law and the FCRA, the bureau must investigate within 30 days (or 45 days if you submit new information during the dispute). The bureau must then send you written results detailing what changed, what was deleted, or why nothing changed. Many consumers make the mistake of disputing only with the bureau while ignoring the furnisher-the creditor or debt collector who originally reported the false information. Contact the furnisher directly as well using their dispute address if listed on your report. If the furnisher finds the information inaccurate, they must tell all three bureaus to update or delete it. About 70% of disputes lead to some correction according to FTC data, but persistence matters when errors reappear or bureaus refuse to investigate properly.

Building Your Evidence File

Gather everything that supports your claim before filing your dispute. Pull account statements showing correct payment history, canceled checks proving you paid on time, identity theft police reports if the error stems from fraud, and any correspondence with creditors about the disputed item. Keep copies of every communication with the bureaus and furnishers, including confirmation numbers from online disputes and receipts from certified mail. If a bureau ignores your dispute or the furnisher fails to correct after you notify them, your evidence file becomes the foundation for legal action. This documentation also helps if you need to file a complaint with the Consumer Financial Protection Bureau or pursue other remedies available under the FCRA.

When Disputes Stall and You Need Help

If the bureau refuses to investigate, the furnisher ignores your correction request, or errors reappear on your report after you dispute them, you have reached the point where legal action becomes necessary. Willful violations of the FCRA allow you to recover actual damages plus statutory damages up to $1,000 per violation, and the bureau or furnisher must pay your attorney fees. Negligent violations also trigger actual damages plus attorney fees. The strength of your case depends on how thoroughly you documented each step of the dispute process and how clearly the bureau or furnisher violated their legal obligations. A consumer protection law firm can review your dispute history and evidence to identify whether violations occurred and what remedies you can pursue.

How Inaccurate Credit Information Damages Your Finances, Serving South Carolina, Including Greenville, Columbia and Charleston

An inaccurate credit report doesn’t sit there harmlessly-it actively costs you money every single day it remains on your file. If a bureau reports a late payment that never happened or a collection account from identity theft, lenders see you as a riskier borrower and charge you higher interest rates to offset that perceived risk. A single error reporting a 30-day late payment can increase your mortgage rate by 0.5 to 1 percentage point, which translates to tens of thousands of dollars in extra interest over a 30-year loan.

The Federal Trade Commission found that about 20% of consumers have errors on at least one major credit report, meaning millions of people pay inflated rates on car loans, mortgages, and credit cards because of information that isn’t even accurate. Employers increasingly pull credit reports during hiring, and negative items-even inaccurate ones-can disqualify you from positions in finance, government, or security work where financial responsibility matters to the employer. Housing discrimination based on credit report errors is also common; landlords deny rental applications when they see collections accounts or late payments, sometimes without bothering to verify whether the information is correct.

The damage compounds because negative information stays on your report for seven years, meaning a single error from 2019 could still sabotage your finances in 2026. South Carolina law recognizes this harm so seriously that if a bureau refuses to remove inaccurate information after you dispute it, damages can accrue at up to $1,000 per day until the error is corrected-a financial penalty that forces bureaus to act quickly when they know they’re wrong.

Why Your Credit Score Plummets From False Information

A wrong late payment or collection account can drop your credit score by 100 points or more depending on what’s reported and how recent the item appears. That 100-point drop doesn’t just feel bad-it moves you from qualified for a prime interest rate into the subprime category, where you’ll pay substantially more for credit. Credit scoring models weight recent payment history much more heavily than older information, so the impact intensifies if the error involves recent activity.

If a bureau reports that you missed a payment last month when you actually paid on time, you start from a much deeper hole than if the error dated back five years. Many people don’t check their credit scores regularly, so errors can damage their finances for months or years before they notice anything wrong. Pull your three credit reports from AnnualCreditReport.com every four months and review your credit score from your bank or credit card issuer at least quarterly.

How Errors Affect Major Financial Decisions

Catching an error within 30 days of it appearing gives you the best chance of correcting it before it affects major financial decisions like applying for a mortgage or refinancing existing debt. If you’ve already been denied credit or offered a worse rate because of an inaccurate report, that’s evidence of real harm you can use in a legal claim against the bureau or furnisher responsible for the error. Lenders rely on credit reports to make decisions about whether to approve your application and what rate to charge, so even one false item can shift the outcome dramatically.

The Long-Term Financial Consequences of Inaction

Waiting for errors to age off your report is not a strategy-it’s financial self-sabotage. Seven years is a long time to pay higher interest rates, face rental denials, or miss job opportunities because of information that isn’t even true. South Carolina residents who discover errors on their credit reports should dispute them immediately rather than hoping the problem resolves itself.

The FCRA requires bureaus to investigate disputes within 30 days, and about 70% of disputes lead to some correction according to FTC data, meaning most errors can be fixed if you take action. The longer you wait, the more damage accumulates in your financial life, and the harder it becomes to prove when the error started affecting your decisions. If errors persist after you dispute them properly, that’s when the case for legal action becomes strong-you have documentation of the bureau’s failure to correct, evidence of financial harm, and a clear record showing the violation occurred.

Final Thoughts

You now understand your rights under the FCRA and how to challenge inaccurate information on your credit report. The practical steps are straightforward: pull your reports, identify errors, document everything, and file disputes with both the bureaus and furnishers. About 70% of disputes result in corrections, so taking action works more often than not.

If you’ve already disputed errors and the bureaus or furnishers ignored your requests, or if errors keep reappearing on your report, you’ve reached the point where professional help becomes necessary. We at Hays Cauley, P.C. are a consumer protection law firm dedicated to helping South Carolina residents with FCRA data accuracy SC issues, identity theft, and debt-related problems. If inaccurate information on your credit report has cost you higher interest rates, denied you employment, or blocked your housing applications, we can review your case and identify whether the bureau or furnisher violated the law.

The FCRA gives you a two-year window from when you discover a violation to file a lawsuit, so acting quickly protects your right to relief. You can recover actual damages, statutory damages up to $1,000 per violation, and attorney fees when violations occur, which means pursuing legal action often costs you nothing upfront. Contact Hays Cauley, P.C. for a confidential consultation if you believe your credit report contains errors that have harmed your finances.