A mistake on your credit report can tank your score and cost you thousands in higher interest rates. Inaccurate information appears on millions of reports every year, yet most people don’t know how to fight back.

The credit report dispute process is straightforward once you understand your rights. We at Hays Cauley, P.C. walk you through each step to reclaim your financial standing.

What Errors Show Up on Credit Reports

Common Mistakes That Appear on Your Report

Inaccurate information spreads across credit reports more often than most people realize. According to the Federal Trade Commission, millions of Americans find errors on their reports each year, ranging from simple personal information mistakes to serious account reporting problems. The three nationwide credit bureaus-Equifax, Experian, and TransUnion-compile data from furnishers like banks, landlords, and credit card companies, and these sources frequently submit incorrect information. Common errors include accounts listed under the wrong name or address, payment histories marked as late when you paid on time, duplicate accounts appearing multiple times, closed accounts still showing as active, and balances that don’t match your actual account statements.

Identity Theft and Fraudulent Accounts

Identity theft creates another category of errors where fraudulent accounts appear under your name. These mistakes aren’t rare exceptions; they’re systematic problems built into how credit reporting works. Personal information errors matter too-an outdated address or misspelled name can complicate your entire financial profile.

How Errors Damage Your Financial Future

A single inaccurate late payment can drop your credit score by 100 points or more, depending on how recent it is. Lenders use credit scores to determine interest rates, and a lower score means you’ll pay thousands more over the life of a mortgage or car loan. The Federal Trade Commission notes that negative information like late payments stays on your report for seven years, while bankruptcies remain for ten years (meaning a single error can haunt you for a decade). Beyond lending, employers sometimes check credit reports before hiring, and insurance companies use credit information to set premiums.

Why You Must Act Now

Disputing errors isn’t optional-it’s the only way to reclaim accurate financial information about yourself. The process is free, and you have legal rights under the Fair Credit Reporting Act to challenge anything you believe is wrong. Taking action now prevents years of higher costs and rejected applications. Understanding what errors look like on your report sets the stage for the next critical step: obtaining your actual credit report and identifying which items need correction.

How to Get Your Credit Report and File a Dispute-Serving South Carolina, Including Greenville, Columbia and Charleston

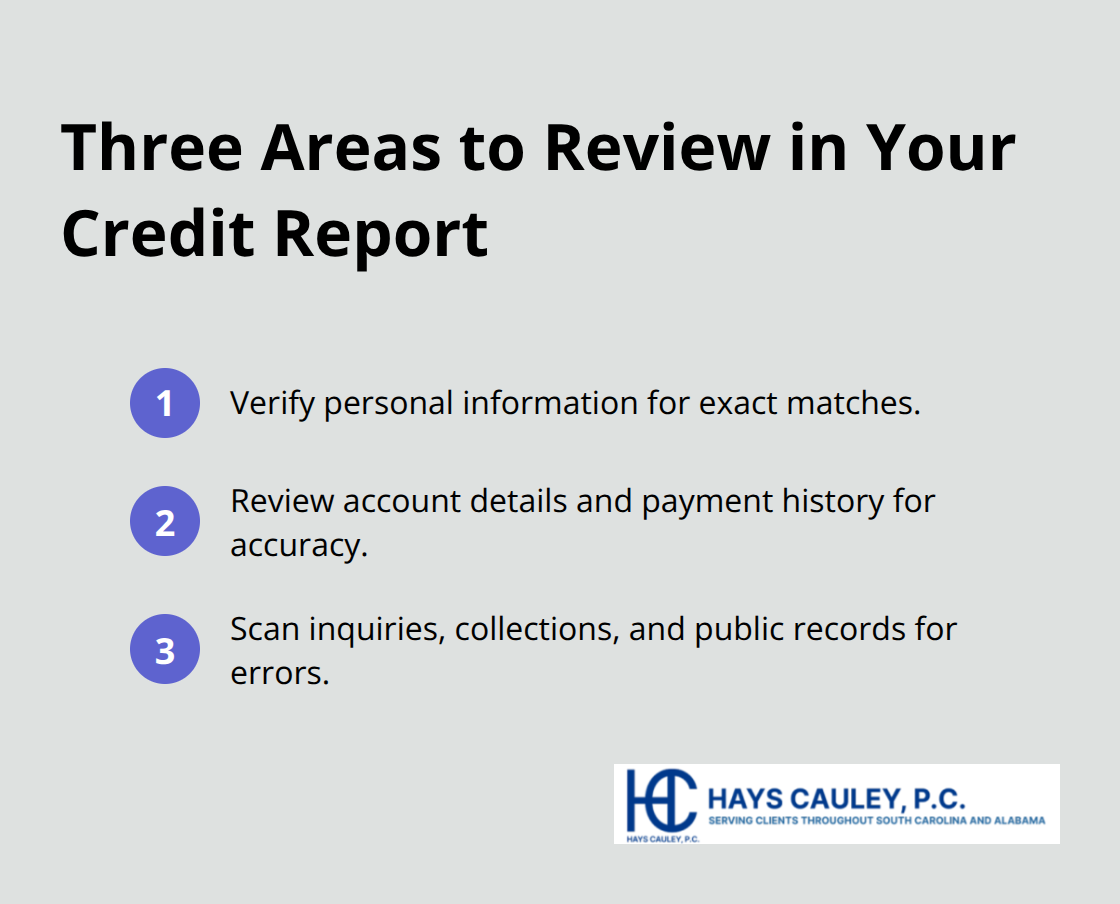

You can access your credit report for free from all three bureaus through AnnualCreditReport.com, which provides one report per bureau every twelve months. The Federal Trade Commission extended free weekly access through 2026, allowing you to monitor your reports far more frequently than before. Equifax offers six additional free reports annually through its site or by calling 1-866-349-5191. Pull reports from all three bureaus since errors on one bureau don’t automatically appear on the others. When you review your report, check three critical areas: personal information like your name, address, and Social Security number; account details including payment history, balances, and account opening dates; and inquiries, collections, or bankruptcies that may be outdated or fraudulent. Circle or highlight every error you find and note the exact account number and creditor name for each mistake.

This documentation becomes your foundation for the dispute.

File Your Dispute with the Correct Bureau

Contact the bureau that reports the error first, not all three at once. Equifax lets you file disputes through your myEquifax account online, which gives you a 10-digit confirmation code to track your case. You’ll receive results within 30 days of submission. Experian accepts disputes online at their website or by phone at 888-397-3742, while TransUnion handles disputes online or at 800-916-8800. If you prefer mailing your dispute, use certified mail with return receipt requested to every bureau reporting the error. Address your letter to Equifax Information Services LLC at P.O. Box 740256, Atlanta, GA 30348; Experian at P.O. Box 4500, Allen, TX 75013; or TransUnion LLC Consumer Dispute Center at P.O. Box 2000, Chester, PA 19016. Include your contact information, the confirmation number from your credit report if available, each disputed item with its account number, a clear explanation of why the information is wrong, copies of supporting documents like payment records or statements, and a copy of your report with errors circled. The bureau must investigate within 30 days and forward your dispute and evidence to the furnisher that reported the information.

Dispute Directly with the Furnisher

The bureau’s investigation alone won’t fix the problem-you must also dispute directly with the furnisher, which is the bank, landlord, or creditor that supplied the incorrect information. Send a separate certified letter to the furnisher’s dispute address, which appears on your credit report. State your name and address, identify each error with account numbers, explain precisely why the information is inaccurate, and request removal or correction. Include copies of supporting documents like cancelled checks, bank statements, or payment records. The furnisher must investigate and respond within 30 days of receiving your dispute. If they determine the information is inaccurate, they must notify all three credit bureaus so your reports get corrected. The Fair Credit Reporting Act gives you this right to challenge information at both the bureau and furnisher level, and the process is completely free. Keep copies of every letter you send and every response you receive throughout the entire dispute process.

What Happens Next in the Investigation

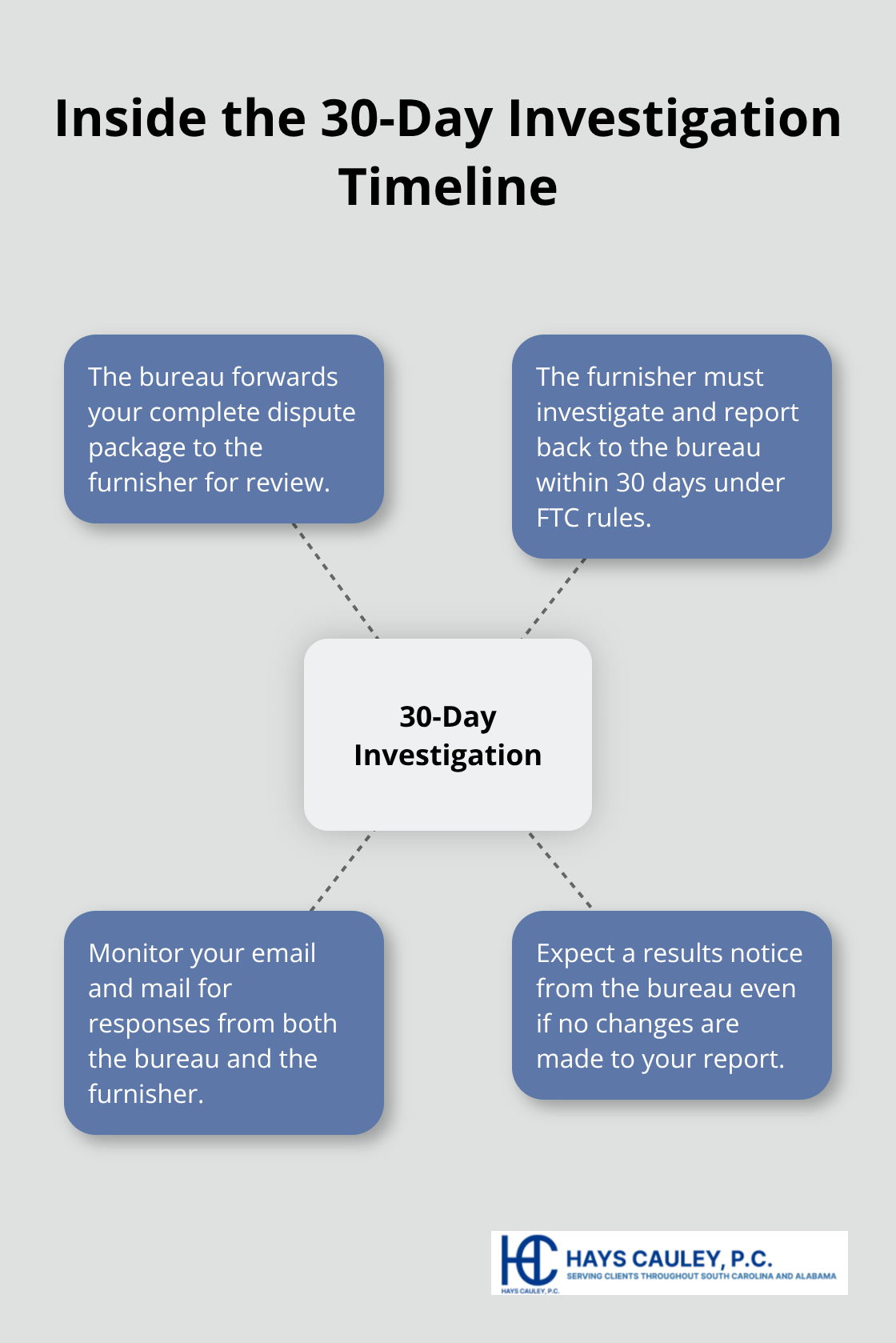

Once you file your dispute with both the bureau and furnisher, the investigation phase begins. The bureau forwards all your evidence to the furnisher, who then investigates the claim and reports back to the bureau. If the furnisher determines the information is inaccurate, they notify all three credit bureaus immediately so corrections appear across your entire credit profile. The bureau provides you with a free copy of your updated report once changes occur. If the investigation doesn’t resolve your dispute, you can add a brief statement to your file explaining your position, and this statement appears on future reports provided to creditors and employers. Understanding what happens during this investigation period helps you know what to expect and when to take additional action if errors persist.

What Happens During Your Dispute Investigation-Serving South Carolina, Including Greenville, Columbia and Charleston

The 30-day investigation window represents your critical period for action. Once you file with the credit bureau, they forward your complete dispute package to the furnisher who reported the error. The furnisher must investigate your claim and respond to the bureau within 30 days, according to the Federal Trade Commission. During this time, monitor your email and mail for responses from both the bureau and furnisher.

The bureau will contact you with results even if nothing changes on your report.

What Happens When Furnishers Respond

If the furnisher finds your information is accurate, they tell the bureau to keep it on file. If they determine it’s wrong, they notify all three bureaus immediately so corrections appear everywhere your credit is reported. This dual-track process matters because sometimes the furnisher responds faster than expected, and you want to catch corrections the moment they happen. Check your myEquifax account, Experian online portal, or TransUnion dashboard weekly during this 30-day period rather than waiting for official notification.

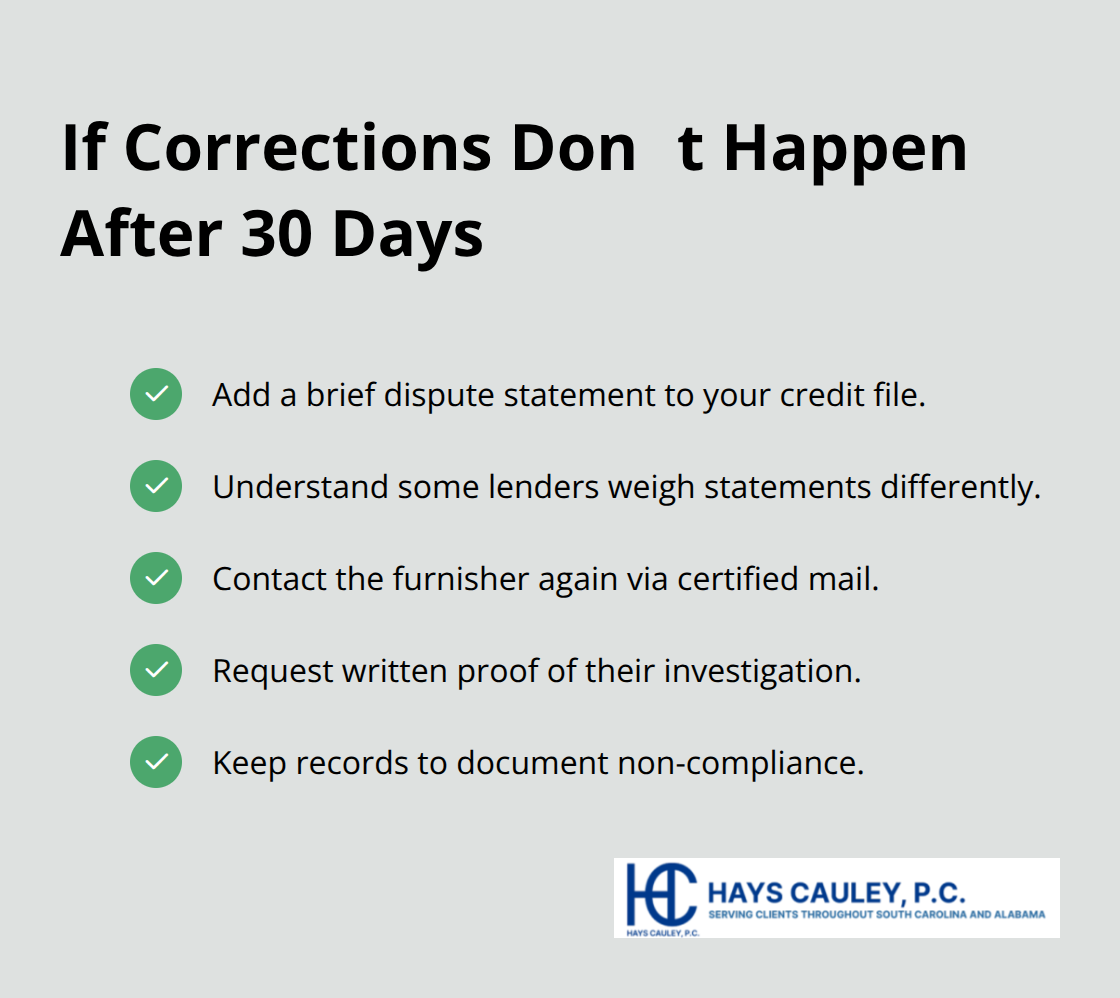

When Corrections Don’t Happen

If the 30 days pass and errors remain, you have concrete options. The Fair Credit Reporting Act allows you to add a brief statement of dispute to your file, and this statement appears on every credit report sent to creditors and employers going forward. This isn’t a perfect solution, but it signals to lenders that you challenged the information. Some lenders ignore dispute statements entirely, while others review them carefully (mortgage lenders tend to pay more attention than credit card companies). If the furnisher continues reporting disputed information after you’ve challenged it, the bureau must include a notice that you’re disputing it, and creditors can see this flag.

Contact the furnisher again in writing with certified mail, referencing your original dispute and the 30-day deadline they missed. Request written proof of their investigation. If they still refuse to correct the error, you’ve documented a clear pattern of non-compliance with federal law.

Escalating Stalled Disputes

Persistent errors demand escalation. If errors remain after 60 days total (30 days for the bureau investigation plus 30 for furnisher response), file a complaint with the Consumer Financial Protection Bureau at their official website. Include your dispute timeline, copies of all letters sent, confirmation numbers, and the furnisher’s failure to correct or respond. The CFPB investigates complaints and can pressure furnishers to take action. You can also report fraud to the Federal Trade Commission at ReportFraud.ftc.gov if you suspect the furnisher is deliberately reporting false information.

Building Your Documentation Trail

Document everything meticulously throughout the process. Keep all certified mail receipts, confirmation codes, letters from bureaus and furnishers, and copies of your reports showing the errors. This documentation becomes essential if you need legal assistance. At this stage, many consumers find that professional help accelerates results, as furnishers respond differently when they know an attorney is involved. Hays Cauley, P.C. helps consumers in South Carolina, including Greenville, Columbia, and Charleston, hold furnishers accountable when they ignore legitimate disputes and violate your Fair Credit Reporting Act rights.

Final Thoughts

Most errors correct themselves within 30 to 60 days when you follow the proper credit report dispute process: obtain your reports, identify mistakes, send certified letters to both the bureau and furnisher, and document everything meticulously. The Fair Credit Reporting Act guarantees your right to challenge inaccurate information, and this process costs nothing. Adding a dispute statement to your file protects you if corrections don’t happen, and reporting non-compliance to the Consumer Financial Protection Bureau escalates stalled cases.

Some furnishers ignore legitimate disputes or continue reporting false information despite your efforts. When a furnisher violates your rights under federal law, legal action becomes necessary if documentation shows a clear pattern of non-compliance, if errors significantly damage your credit score or finances, or if a furnisher refuses to investigate your dispute properly. Furnishers often correct errors quickly once they know an attorney is involved.

We at Hays Cauley, P.C. help consumers throughout South Carolina, including Greenville, Columbia, and Charleston, hold furnishers accountable for credit reporting violations. If you’ve followed the dispute process and errors remain, or if a furnisher reports false information deliberately, contact us to discuss your options. You may have a claim for damages under the Fair Credit Reporting Act, and inaccurate information should not control your financial future.