Your credit report affects your ability to borrow money, rent an apartment, and sometimes even get hired. Errors on that report can damage your financial future, which is why understanding your credit reporting rights explained is so important.

At Hays Cauley, P.C., we help South Carolina residents-including those in Greenville, Columbia, and Charleston-protect themselves from inaccurate credit information. This guide walks you through your legal protections and shows you exactly how to fix mistakes on your credit file.

What Are Credit Reporting Rights

Understanding the Fair Credit Reporting Act

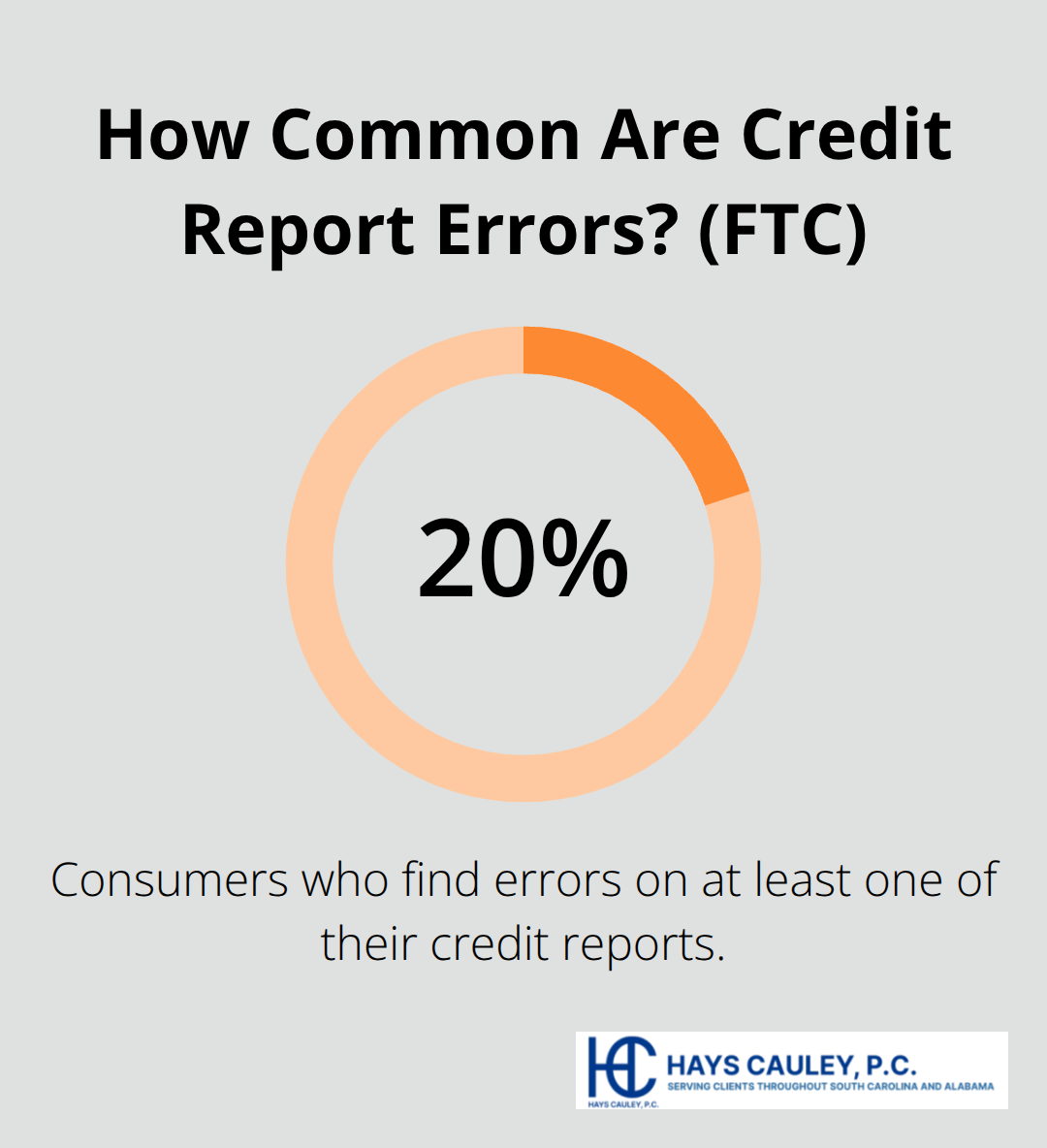

The Fair Credit Reporting Act is a federal law that gives you specific powers over how your credit information is collected, used, and distributed. Under this law, you have the absolute right to access your credit report from the three major bureaus-Equifax, Experian, and TransUnion-once every 12 months at no cost through AnnualCreditReport.com. The Federal Trade Commission expanded free access through 2026, allowing you to request one free report from each bureau every four months. This matters because the FTC found that roughly 20% of consumers find errors on at least one of their credit reports.

The Real Cost of Credit Report Errors

Those errors can cost you real money. A difference between a 650 and 750 credit score on a $200,000 mortgage means approximately $68,000 in interest over 30 years. Your credit report affects your ability to borrow money, rent an apartment, and sometimes even get hired, which is why accuracy matters so much. Even a single mistake can lower your score and limit your financial opportunities.

Your Right to Dispute and Correct Information

You have the right to dispute any information you believe is inaccurate, and when you do, the credit bureau must investigate your claim within 30 days at no charge. The bureau forwards your complaint to the company that reported the information, and that company must investigate and respond. If the information cannot be verified, it must be removed from your report. If it’s found accurate, the bureau must explain how they determined that.

South Carolina’s Additional Protections

South Carolina law further protects you by allowing you to place a security freeze on your credit file at no cost, which prevents lenders from accessing your report without explicit authorization-a powerful tool against identity theft. The law also imposes real penalties on bureaus that violate these protections: negligent violations carry liability for actual damages or at least $1,000 per incident plus attorney fees, while willful or grossly negligent violations can trigger up to three times actual damages or $3,000 per incident.

These aren’t theoretical protections; they’re enforceable rights that put you in control of your financial information. Now that you understand what rights you have, the next step is learning how to actually access your credit reports and identify the errors that may be harming your score.

Accessing Your Credit Reports and Spotting Problems

Where to Get Your Free Credit Reports

You need to see what lenders and employers see about you, and that means obtaining your actual credit reports. Start with AnnualCreditReport.com, the official source operated by Equifax, Experian, and TransUnion. This site costs nothing and requires no credit card, unlike countless impostor websites that charge hidden fees. Request one report from each bureau every four months rather than pulling all three at once; this approach gives you ongoing visibility throughout the year instead of a single snapshot. The Federal Trade Commission also expanded free access through 2026, allowing you to obtain an extra free report from Equifax by calling 1-866-349-5191, giving you six total free Equifax reports annually on top of your standard annual access. When you request your reports, do it in writing or online and keep documentation of your request date and method.

Why Errors Happen So Often

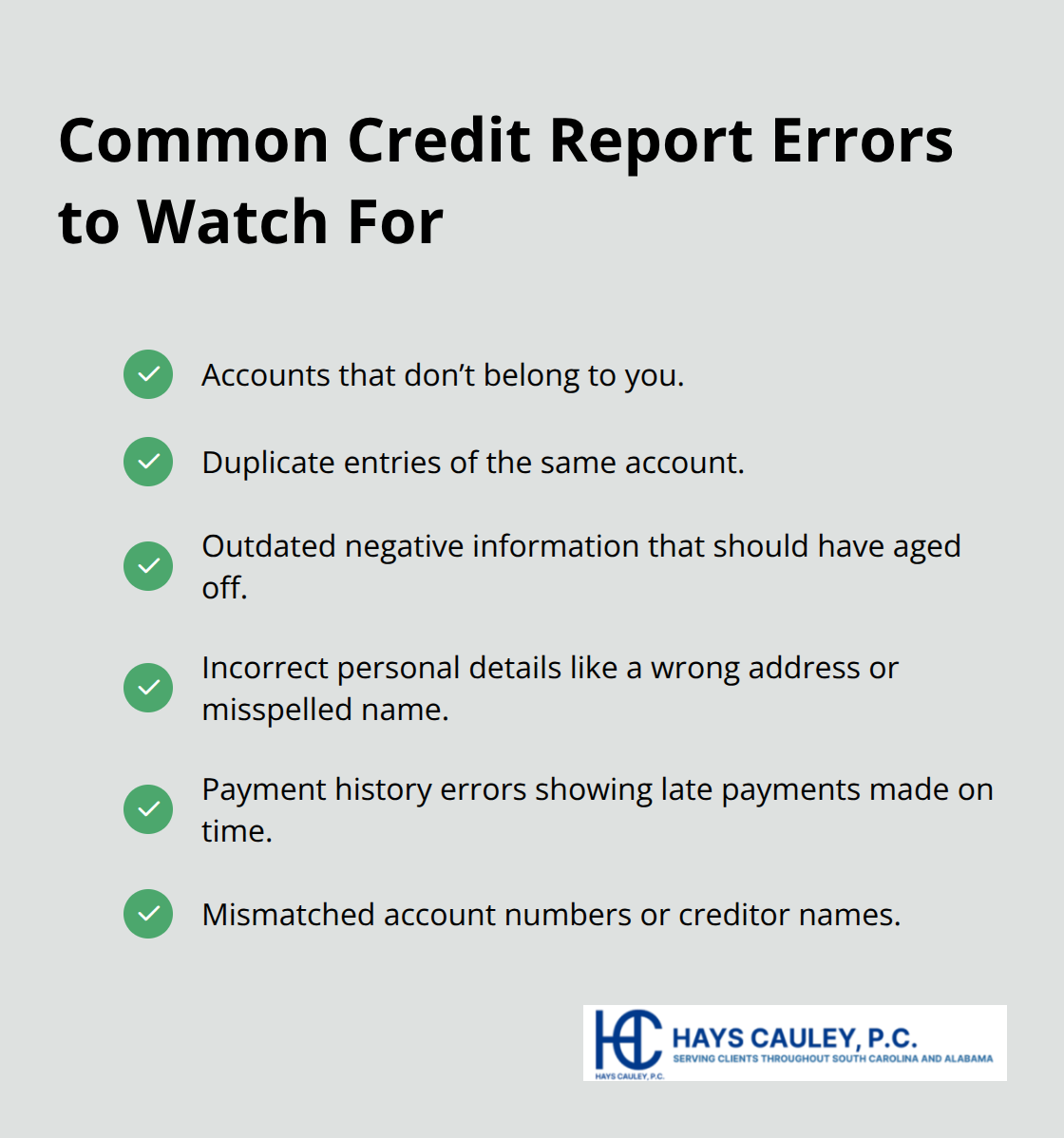

The credit bureaus process hundreds of millions of transactions daily, which means errors slip through constantly. Common mistakes include accounts that don’t belong to you, duplicate entries of the same account, outdated negative information that should have aged off your report, incorrect personal information like a wrong address or misspelled name, and payment history errors showing late payments you actually made on time. The Federal Trade Commission reports that roughly 20% of consumers find errors on at least one of their three reports, so you cannot assume yours will be clean.

How to Review Your Reports Line by Line

Once your reports arrive, examine them line by line against your own records. Start with your personal information section and verify every name variation, address, phone number, and employer listed. Then examine your account history section, checking the account type, creditor name, account number, opening date, current balance, credit limit, and payment status for each entry. Compare these details against your own statements and records (keep your documentation organized as you work through each report).

Document Every Error You Find

If you spot something wrong, write it down with the exact account number and the specific error. Create a separate file for each error with copies of your evidence, your credit report pages showing the problem, and notes about when you discovered it. This documentation becomes your foundation for the dispute process that follows, which requires you to present specific, detailed information to the credit bureaus.

How to File a Dispute and Fix Your Credit Report

File Your Dispute with the Credit Bureau

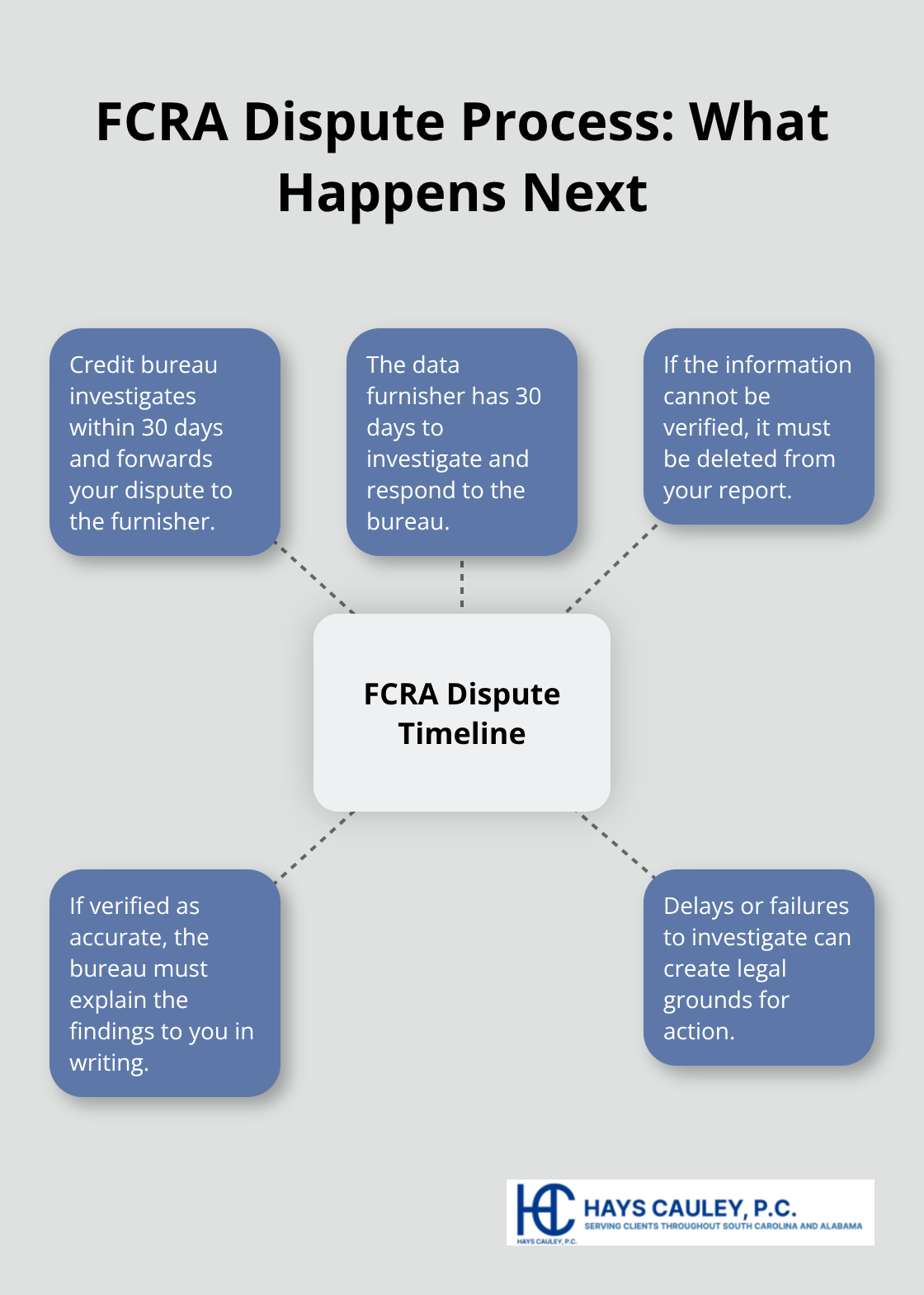

Once you’ve identified errors on your credit report, file a dispute directly with the credit bureau online, by mail, or by phone. Contact Equifax at 866-349-5191, Experian at 888-397-3742, or TransUnion at 800-916-8800. When you file, be specific: identify each disputed item by account number, explain exactly what’s wrong, and include copies of supporting documents that prove the error. The credit bureau must investigate within 30 days and forward your dispute to the company that reported the information.

That company then has the same 30-day window to investigate and respond. If they cannot verify the information, it must be removed from your report. If the investigation finds the information accurate, the bureau will notify you in writing and explain their verification process. This 30-day requirement is enforced-delays or failures to investigate give you legal grounds for action.

Verify the Correction and Request Updated Reports

After the bureau completes their investigation, request a free updated copy of your report to confirm the correction appeared. If the error remains, file a second dispute and submit a written statement to be added to your file explaining your position; future reports will include this dispute notice. Contact the company that reported the error directly and send them a formal dispute letter with the same documentation you sent the bureau. Under the Fair Credit Reporting Act, they must investigate and report their findings back to the credit bureaus. Many errors disappear faster when the data furnisher receives direct pressure.

Monitor Your Reports on a Schedule

After disputes are filed, monitor your reports quarterly for the next year. Pull one free report from each bureau every four months using AnnualCreditReport.com to track whether corrections stuck and no new errors appeared. Set phone reminders to check your reports on a schedule rather than waiting until you need credit for something important. If inaccurate information reappears after correction, file another dispute immediately; repeated reporting of disputed items violates the Fair Credit Reporting Act. The bureaus must flag your file to show you’re disputing the information.

Take Legal Action if Disputes Fail

If you filed multiple disputes and corrections aren’t happening, or if you believe the bureaus are violating your rights, consider consulting with a consumer protection attorney. We at Hays Cauley, P.C. help South Carolina residents address credit reporting violations and can advise on next steps, including potential legal remedies available under federal law.

Final Thoughts

The Fair Credit Reporting Act gives you real power to control your financial information, but that power only works if you act on it. You now understand your credit reporting rights explained and know exactly how to access your reports, spot errors, and file disputes that force corrections. The 30-day investigation requirement is a legal obligation that bureaus must follow, and violations carry penalties of at least $1,000 per incident plus attorney fees for negligent violations, or up to $3,000 per incident for willful violations.

Most errors disappear once you file a formal dispute with documentation, though some stick around because the data furnisher keeps reporting them or the bureau fails to investigate properly. When that happens, you have options beyond another dispute letter-contact a consumer protection attorney if corrections aren’t happening after multiple attempts or if you suspect the bureaus are ignoring your rights. We at Hays Cauley, P.C. help South Carolina residents address credit reporting violations and can evaluate whether you have grounds for legal action under federal law.

Your credit score affects loan approvals, interest rates, insurance premiums, rental eligibility, and sometimes hiring decisions, so inaccurate information on your report shouldn’t control your financial future. Start by pulling your free reports from AnnualCreditReport.com, review them carefully against your own records, and file disputes for anything that’s wrong. If the bureaus aren’t cooperating, reach out to Hays Cauley, P.C. for guidance on protecting your rights and restoring your credit health.