A credit report error can tank your score and cost you thousands in higher interest rates. Many people try to fix these mistakes on their own, only to hit dead ends with credit bureaus that ignore their complaints.

That’s where a credit report errors lawyer makes the difference. At Hays Cauley, P.C., we know how to fight back against inaccurate information and get results that DIY disputes simply cannot achieve.

What Errors Actually Show Up on Credit Reports

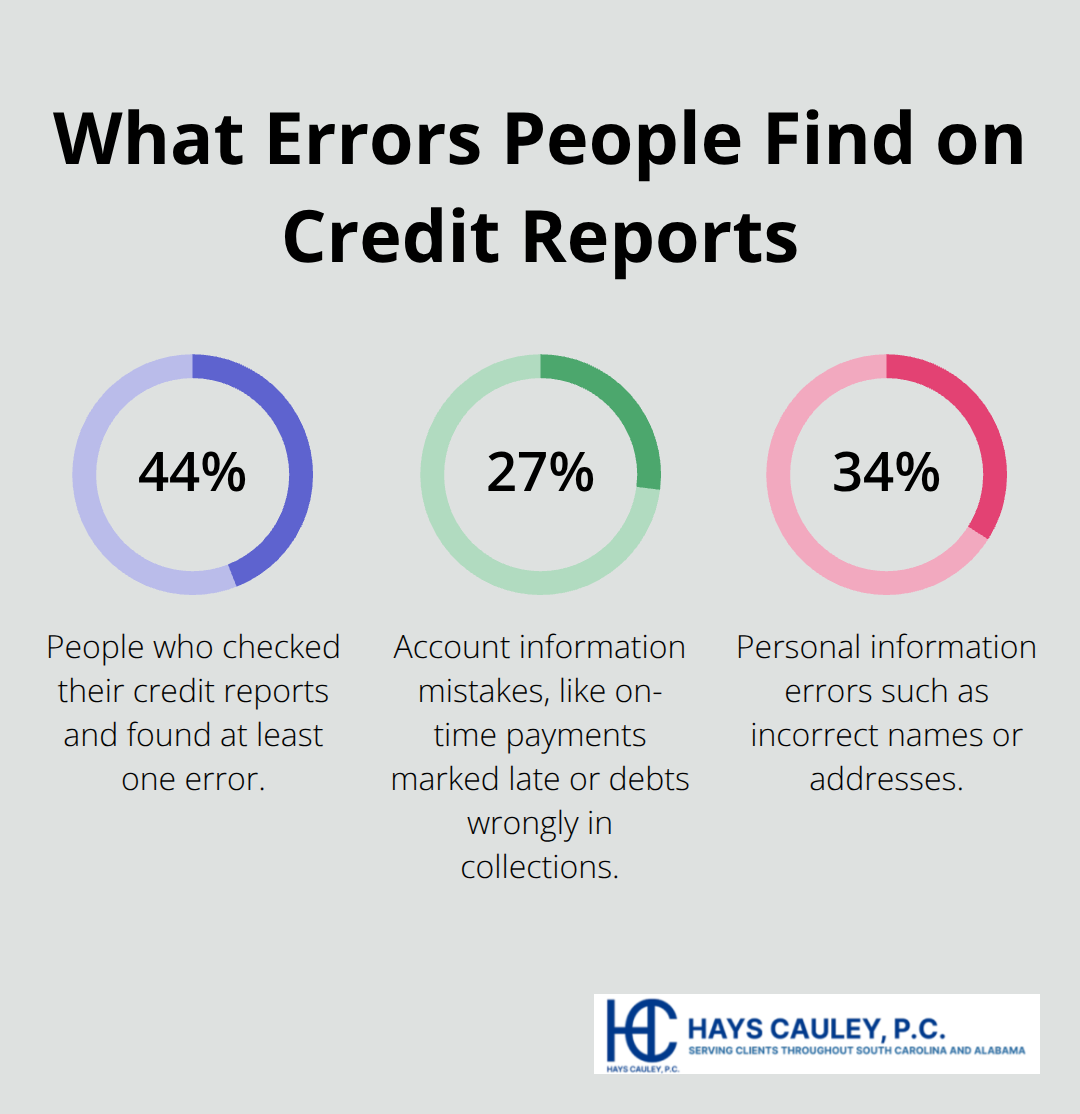

Credit report errors fall into distinct categories, and knowing which ones plague your file matters because different errors require different fixes. According to a February 2024 study by Consumer Reports and WorkMoney involving over 4,000 participants, 44% of people who checked their credit reports found at least one error. Account information mistakes topped the list at 27%, including late payments reported when they were actually made on time, unrecognized accounts, and debts wrongly listed in collections. Personal information errors accounted for 34% of findings, such as incorrect names or addresses appearing on reports.

Mixed Files and Duplicate Entries

Mixed files represent a serious category where information from someone with a similar name or Social Security number bleeds into your report, creating a financial nightmare that standard disputes often fail to catch. Duplicate entries also plague reports frequently-the same account appears multiple times, artificially tanking your score. Paid-off accounts continuing to show as unpaid stand out as particularly damaging because they signal ongoing delinquency to lenders even though you’ve settled the debt.

The Real Cost of Inaccuracy

These errors directly slash your credit score and wallet. A single error can cost you thousands in higher interest rates on mortgages, auto loans, and credit cards. Beyond lending, inaccurate credit information blocks housing approvals, eliminates job opportunities, and inflates insurance premiums. The Federal Trade Commission reports that up to 20% of consumers carry at least one error on their credit report, yet most never challenge it.

Why Bureaus Resist Corrections

Credit reporting agencies and data furnishers have little incentive to fix errors independently because they profit from the volume of information they process. The dispute process itself often fails because third-party disputes filed through credit repair services get flagged as frivolous and ignored by bureaus. Direct consumer disputes fare better, but agencies still conduct minimal investigations when they’re not motivated by legal pressure. This resistance to correction is precisely why many consumers find themselves stuck-their complaints disappear into bureaucratic black holes, and their credit scores remain damaged.

Why Legal Help Stops Credit Bureaus From Ignoring Your Disputes: Serving South Carolina, including Greenville, Columbia and Charleston

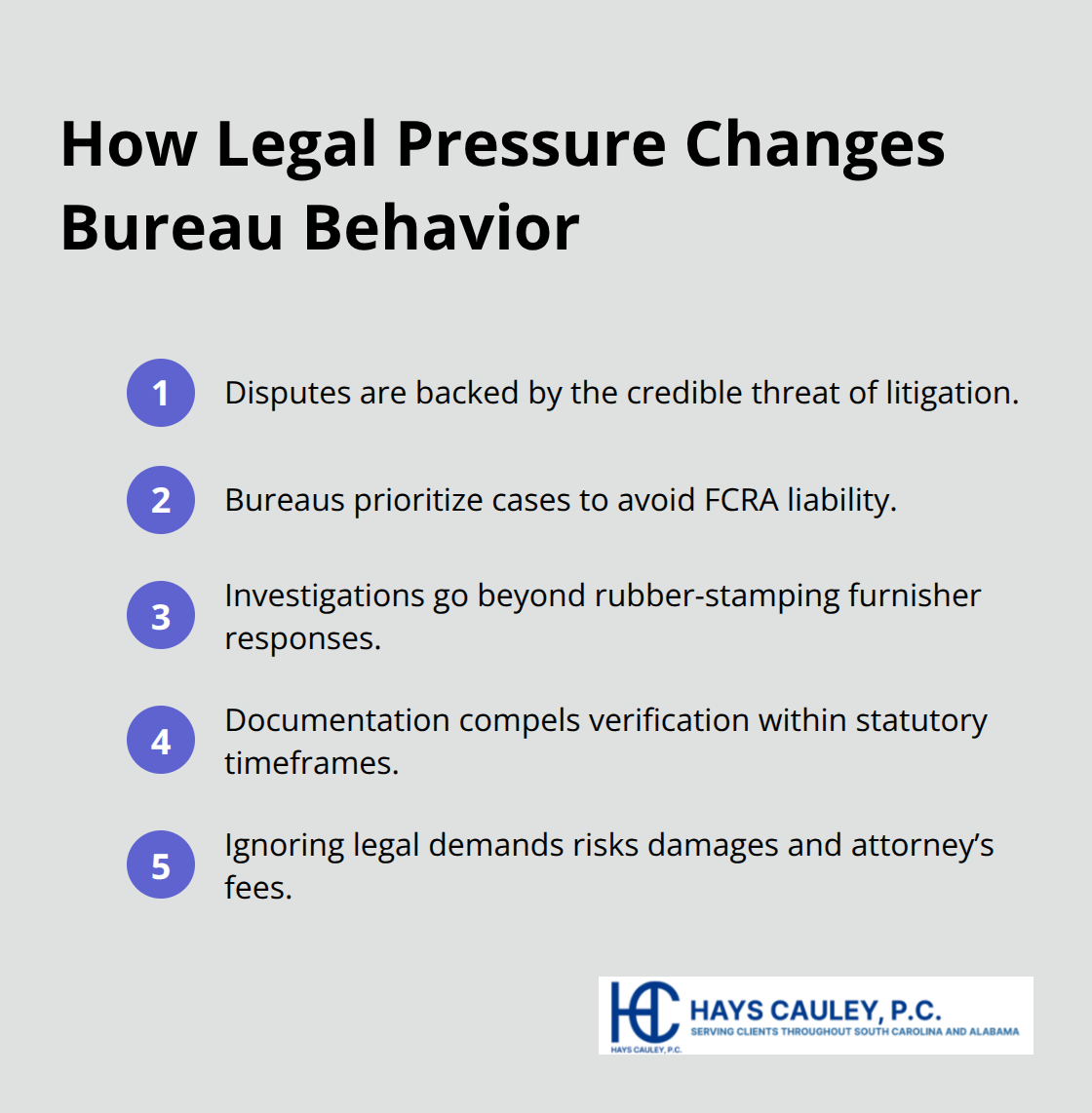

The Fair Credit Reporting Act gives you the right to dispute inaccuracies, but the law itself won’t force credit bureaus to listen. When you file a dispute on your own, you’re competing against a system designed to process thousands of complaints daily with minimal investigation. Third-party disputes filed through credit repair services get treated as frivolous and ignored outright. Even direct consumer disputes often receive cursory reviews because agencies lack motivation to dig deeper without legal pressure behind them. A lawyer transforms this dynamic entirely. A lawyer files disputes backed by the credible threat of litigation, which changes how bureaus respond. They know that ignoring a lawyer’s dispute letter could lead to an FCRA lawsuit where they face damages and attorney’s fees.

This shifts the entire equation from passive complaint to active enforcement.

Credit Bureaus Operate on Volume, Not Accuracy

Equifax, Experian, TransUnion, and Innovis process hundreds of millions of transactions daily, and they profit from moving data quickly, not from fixing it accurately. When a consumer files their own dispute, the bureau conducts a minimal investigation and often sides with the data furnisher who originally reported the error. The furnisher, in turn, has little incentive to correct mistakes because they face no consequences for inaccuracy. A lawyer’s dispute letter includes specific facts, documentation, and legal citations that force a real investigation. Lawyers reference FCRA sections that require agencies to conduct reasonable investigations and delete unverifiable information. This approach works because it creates liability. Bureaus know that if they dismiss a lawyer’s dispute without proper investigation, they’ve opened themselves to a lawsuit where courts can award damages, attorney’s fees, and court costs.

How Legal Pressure Changes Bureau Behavior

The Consumer Financial Protection Bureau reported that credit reporting complaints rose from 165,129 in 2021 to 430,600 in 2023, yet most consumers who file their own disputes never see corrections. Legal help changes that outcome because it introduces consequences that standard disputes cannot. When a lawyer sends a dispute letter, the bureau treats it differently-they conduct actual investigations rather than rubber-stamping the furnisher’s response. Courts increasingly hold credit bureaus accountable for sloppy practices, which means settlements send a signal that corrections matter. A bureau that ignores a lawyer’s demand faces potential litigation costs that far exceed the expense of simply fixing the error.

Pursuing Compensation for Real Financial Harm

A lawyer can pursue compensation when errors cause real financial harm (mortgage denials, job loss, inflated insurance rates). You may have grounds to recover damages under the FCRA when inaccurate information directly harms your finances. Credit repair services cannot pursue this remedy because they lack legal authority. Only a licensed attorney can file a lawsuit against credit bureaus or data furnishers and negotiate settlements that include corrected reports plus monetary recovery. Many consumer protection attorneys handle FCRA litigation on a contingency basis, meaning you pay no upfront fees. The responsible party typically covers legal costs if you prevail.

Fixing Mixed Files and Complex Errors

Beyond individual disputes, lawyers also handle mixed files where information from someone with a similar name or Social Security number contaminates your report. These cases require coordination across multiple bureaus and furnishers, something a consumer fighting alone rarely accomplishes. A lawyer identifies which bureau holds the contaminated file, contacts all relevant furnishers, and ensures corrections propagate across your entire credit profile. This coordination prevents the error from reappearing on one bureau while another shows the corrected information. When you understand what legal action can accomplish, the next step involves knowing exactly what a lawyer investigates and documents before filing any dispute.

What Lawyers Actually Do to Fix Your Credit Report

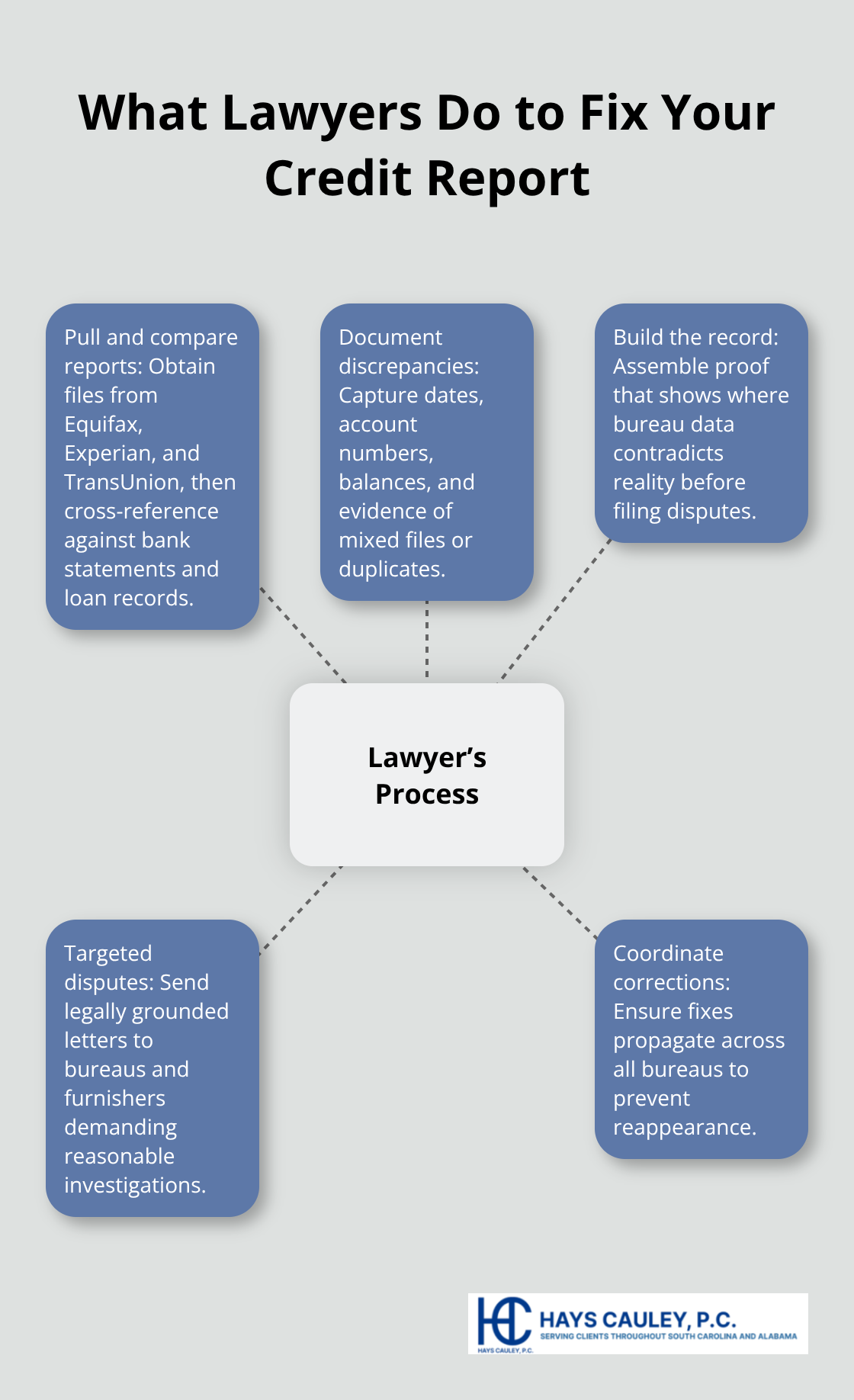

A lawyer pulls your complete credit file from all three major bureaus (Equifax, Experian, and TransUnion) and cross-references it against bank statements, loan documents, and payment records to identify exactly where inaccuracies live. This documentation phase transforms a vague complaint into concrete evidence. The lawyer notes dates, account numbers, reported balances versus actual balances, and flags duplicate entries or mixed file contamination.

According to the February 2024 Consumer Reports and WorkMoney study, 27% of credit report errors involved account information mistakes such as late payments reported when they were made on time or debts wrongly listed in collections. A lawyer builds a factual record that proves what went wrong and why the bureau’s records contradict reality.

The lawyer then files disputes directly with credit bureaus and data furnishers, but these disputes carry legal weight because they reference specific FCRA violations and demand reasonable investigation. Unlike consumer disputes that bureaus process in bulk with minimal attention, a lawyer’s dispute letter signals potential litigation. Bureaus know that dismissing a properly documented dispute without conducting a real investigation creates liability under the Fair Credit Reporting Act. This shifts how the bureau handles your case from routine processing to priority review.

How Documentation Strengthens Your Case

A lawyer’s investigation uncovers patterns that individual consumers miss. When you compare your actual payment history against what appears on your credit report, discrepancies become obvious. The lawyer documents these discrepancies with supporting evidence-bank statements showing on-time payments, loan documents proving account ownership, and correspondence from creditors confirming settlements. This evidence package forces credit bureaus to conduct actual investigations rather than rubber-stamping the data furnisher’s original response. Courts increasingly hold bureaus accountable for sloppy practices, which means settlements send a signal that proper investigation matters.

Filing Disputes That Demand Real Investigation

A lawyer’s dispute letter differs fundamentally from a consumer’s standard dispute form. The letter references specific FCRA sections that require agencies to conduct reasonable investigations and delete unverifiable information. It cites the exact violations present in your file and demands that the bureau verify the accuracy of disputed items within the statutory timeframe. Bureaus treat these letters differently because they understand the legal consequences of ignoring them. A bureau that dismisses a lawyer’s demand without proper investigation faces potential litigation costs that far exceed the expense of simply correcting the error.

Pursuing Settlements and Damages

If the bureau refuses to correct errors after a lawyer’s demand, the next step involves filing an FCRA lawsuit against the credit reporting agency, the data furnisher, or both. Courts can award actual damages (money for financial harm caused by the error), statutory damages up to 1,000 dollars per violation, attorney’s fees, and court costs. Many consumer protection attorneys handle these cases on contingency, meaning you pay nothing upfront and the responsible party covers legal fees if you win. This arrangement eliminates the financial barrier that prevents most consumers from pursuing legal action.

A lawyer negotiates directly with bureaus and furnishers to reach settlements that include corrected reports plus monetary compensation without requiring a trial. These negotiations happen faster when the other side understands you have legal representation and documentation backing your claim. For consumers dealing with identity theft or mixed files where information from someone else contaminates your report, a lawyer coordinates corrections across all bureaus simultaneously, preventing the error from reappearing on one bureau while another shows the corrected version.

Escalating Through Federal Agencies

The lawyer also handles CFPB complaints if disputes fail, escalating your case to a federal agency with enforcement power that individual consumers cannot access independently. When a bureau ignores a lawyer’s dispute letter, the CFPB complaint carries additional weight because it documents the bureau’s failure to respond appropriately to a documented legal demand. This federal involvement often prompts faster action from credit bureaus that might otherwise delay corrections indefinitely.

Final Thoughts

DIY disputes fail because credit bureaus ignore complaints without legal pressure behind them. When you file your own dispute, the bureau conducts minimal investigation and often sides with the data furnisher who reported the error. A credit report errors lawyer changes this dynamic entirely by filing disputes backed by the credible threat of litigation, which forces bureaus to conduct actual investigations rather than rubber-stamp responses. Bureaus know that ignoring a properly documented legal demand could result in an FCRA lawsuit where they face damages, attorney’s fees, and court costs.

We at Hays Cauley, P.C. understand how credit reporting agencies operate and what forces them to correct errors. Our team handles the investigation, documentation, and dispute process so you don’t have to navigate the system alone. We pull your complete credit file, identify exactly where inaccuracies live, and file disputes that demand real investigation. When bureaus refuse to correct errors, we pursue FCRA litigation to recover damages and attorney’s fees, with many cases handled on contingency so you pay nothing upfront.

If errors on your credit report are costing you higher interest rates, blocking housing approvals, or eliminating job opportunities, contact Hays Cauley, P.C. for a free consultation to discuss your case and learn what legal remedies apply to your situation. We serve South Carolina, including Greenville, Columbia and Charleston, and we’re ready to help you reclaim an accurate credit profile.