Financial companies break the rules every day, and most people don’t realize it’s happening to them. Inaccurate credit reports, unauthorized charges, and aggressive debt collectors damage your finances and your future.

We at Hays Cauley, P.C. help South Carolina residents fight back. A consumer rights lawyer can identify violations, recover damages, and protect your financial standing.

What Laws Protect You From Financial Companies

Federal law sets strict rules that financial companies must follow, and violations happen more often than most people realize. The Fair Credit Reporting Act requires credit bureaus and lenders to maintain accurate information about your financial history, yet the Consumer Financial Protection Bureau logged about 800,000 complaints in a single year related to deceptive financial practices. Many of these complaints stem from credit reporting errors-incorrect account status, identity mistakes, and balance discrepancies that tank your credit score without reason. The Truth in Lending Act mandates that lenders disclose all costs upfront, including interest rates and fees, before you sign anything.

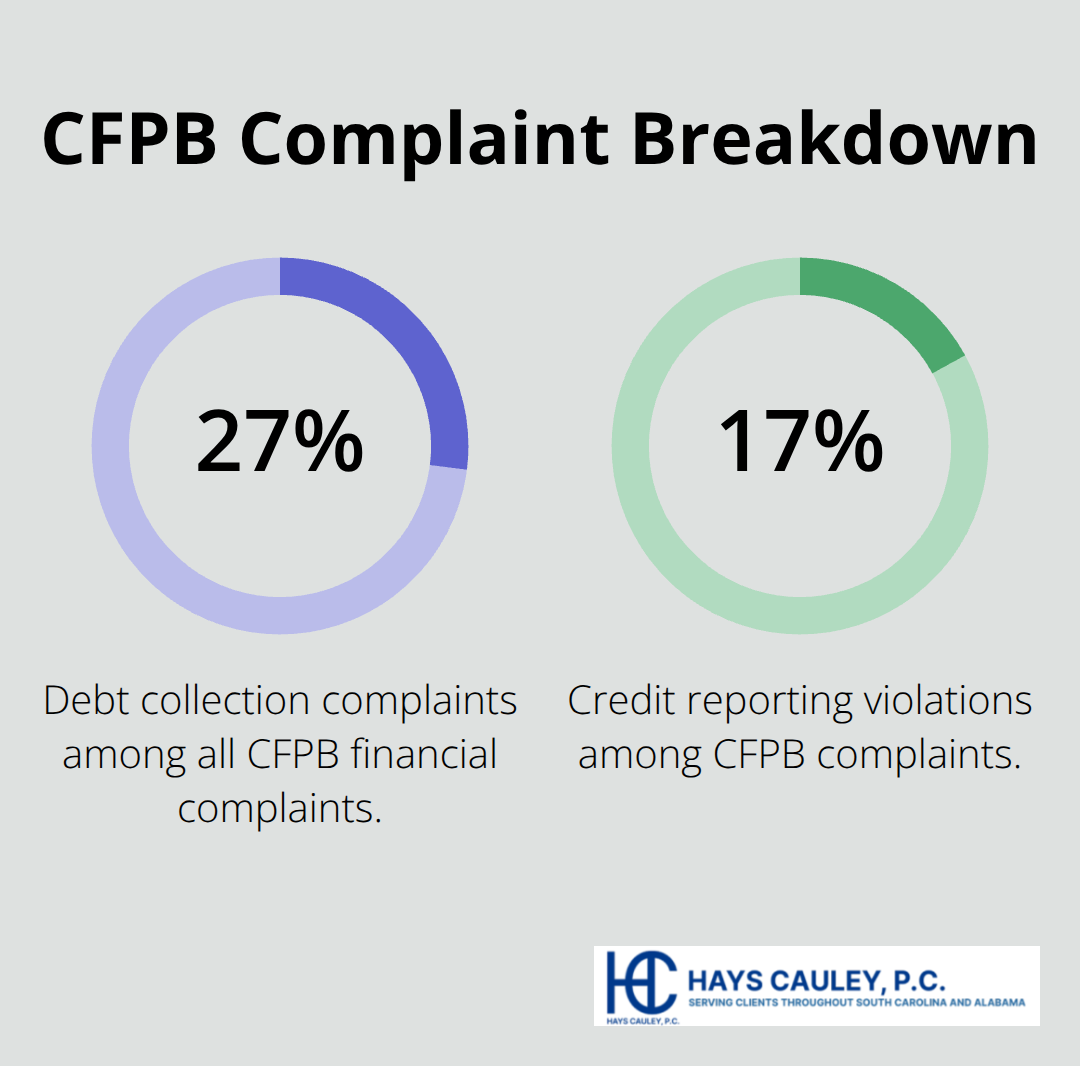

Banks and credit card companies routinely hide fees in fine print or bury them in lengthy documents, hoping you won’t catch the deception. The Fair Debt Collection Practices Act prohibits debt collectors from harassing you, calling before 8 a.m. or after 9 p.m., contacting your employer, or collecting debts you don’t actually owe. Despite these protections, the CFPB reported that debt collection complaints make up about 27 percent of all financial complaints, often involving debts consumers don’t owe-which means validation of the debt is your first line of defense.

Credit Reporting Accuracy Is Non-Negotiable

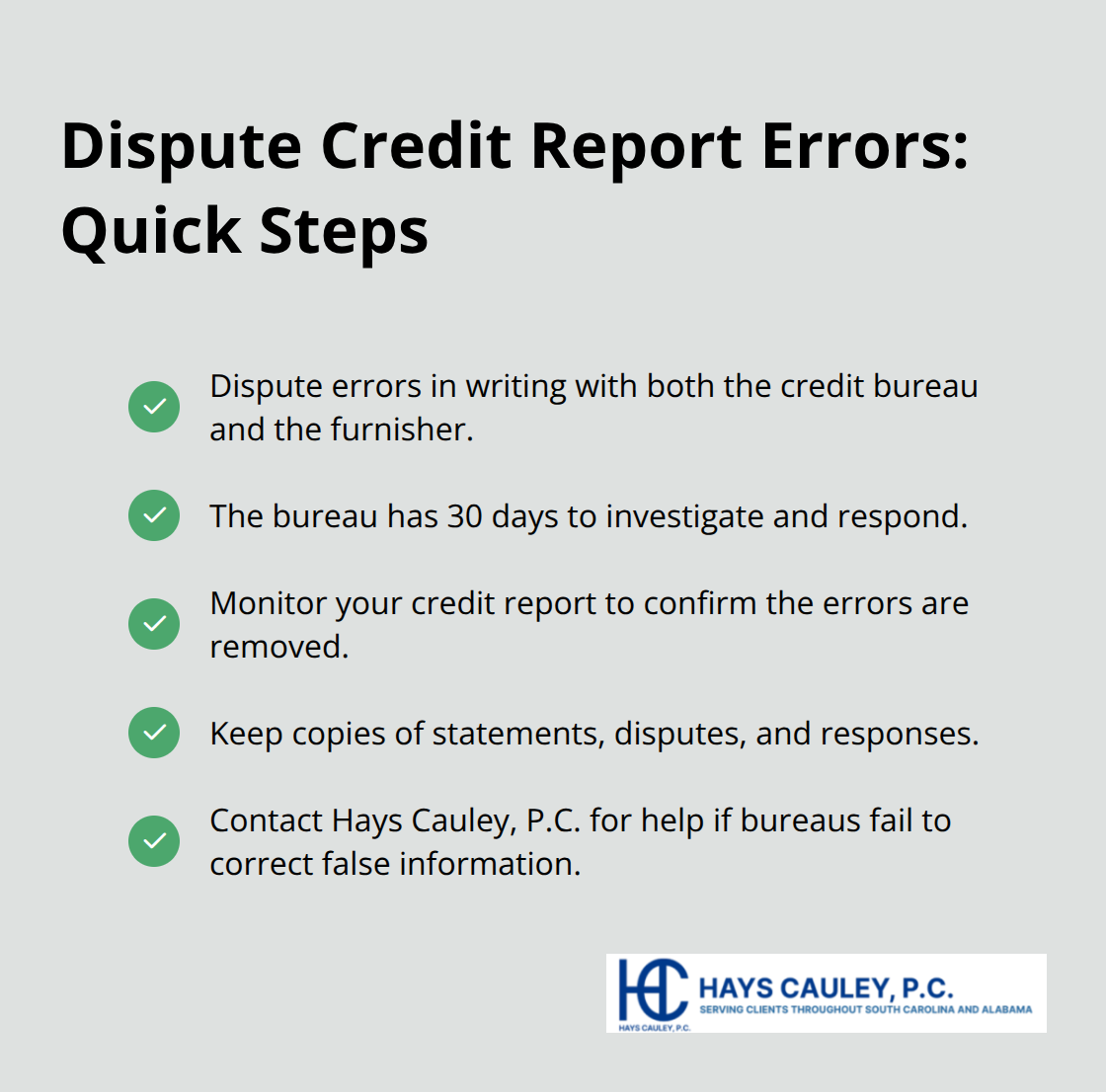

Credit reporting violations account for about 17 percent of CFPB complaints, and inaccurate entries directly destroy your ability to borrow money at fair rates. If your credit report contains errors, you have the right to dispute them with both the credit bureau and the company that reported the information. This process must happen in writing, and the bureau has 30 days to investigate and respond. You should monitor your credit report after disputes are filed to confirm the errors are actually removed. Hays Cauley, P.C. helps South Carolina residents challenge credit reporting violations and recover damages when bureaus fail to correct false information.

Unauthorized Charges and Debt Collection Abuse

If a lender or debt collector violates the Fair Debt Collection Practices Act, you can sue for actual damages plus up to $1,000 in statutory damages per case. Unauthorized charges on credit cards must be reported within 60 days of the statement, and your liability caps at $50 per card under federal law. You should document every conversation with debt collectors-get names, dates, times, and what was said-because this evidence proves harassment when collectors call repeatedly or threaten you illegally. Send written disputes to debt collectors demanding they validate the debt, which stops collection efforts while they investigate. These violations often overlap with identity theft, which requires immediate action to protect your financial future.

Financial Violations You’re Likely Missing

Credit Report Errors That Wreck Your Score

Credit reporting errors appear on roughly 1 in 5 credit reports, yet most people never dispute them because they don’t know the violation exists. Wrong account statuses, fraudulent accounts opened in your name, and balance discrepancies silently destroy your credit score and lock you out of favorable interest rates. The moment you spot an error-a closed account showing as open, a paid-off debt still marked as delinquent, or an account you never opened-you must dispute it in writing with both the credit bureau and the company that reported it. This written dispute triggers a 30-day investigation period, and the bureau must remove the error if it cannot verify accuracy. Many people skip this step and assume the error will fade on its own, which is a costly mistake that costs you thousands in higher interest rates over time.

Identity Theft and Unauthorized Charges

Unauthorized charges and identity theft often hide in plain sight because victims don’t review statements carefully. The Federal Trade Commission reports consumer fraud costs Americans over $10 billion annually, and identity theft represents a massive chunk of that damage. You have 60 days from the date a fraudulent charge appears on your credit card statement to report it and cap your liability at $50 per card. Beyond that window, you lose protections and the liability shifts to you. Many people discover identity theft months or years later when applying for a mortgage or car loan and finding accounts they never opened. You must document the exact date you discovered the fraud, preserve all statements showing the unauthorized activity, and file a report with the Federal Trade Commission immediately-this creates an official record that helps you dispute false debts later.

Debt Collection Violations and Your Rights

Aggressive debt collection tactics often cross legal lines because collectors operate under pressure to extract payments fast. The Fair Debt Collection Practices Act prohibits calling before 8 a.m. or after 9 p.m., contacting your employer or family members, threatening arrest or wage garnishment they cannot legally pursue, and collecting on debts you do not owe. The Consumer Financial Protection Bureau received over 200,000 debt collection complaints in a recent year, with the most common violation being attempts to collect debts the consumer does not actually owe. Your first move when a debt collector calls is to request written validation of the debt within 30 days-this stops collection efforts temporarily and forces the collector to prove you actually owe the money. You should send this validation request via certified mail with return receipt so you have proof the collector received it. You must record the collector’s name, the date and time of the call, and exactly what they said, because this documentation becomes critical evidence if they violate the law. If a collector ignores the validation request, calls repeatedly after you request they stop, or misrepresents the debt, you have grounds for a lawsuit. Violations of the Fair Debt Collection Practices Act can result in statutory damages up to $1,000 per case, which means the financial stakes are real when collectors break the rules.

These violations often overlap and compound your financial damage, which is why identifying them early matters. The next section walks you through the specific warning signs that tell you whether you have a valid consumer protection claim worth pursuing.

When a Consumer Rights Lawyer Should Handle Your Case: Serving South Carolina, Including Greenville, Columbia and Charleston

Recognizing a Valid Consumer Protection Claim

The hardest part of fighting financial violations is knowing when you actually have a case worth pursuing. Most people assume their problems are too small or too complicated to warrant legal action, but that assumption costs them thousands in damages they could recover. You have a valid consumer protection claim if a financial company or debt collector violated federal law in a way that harmed you financially or emotionally. Fair Debt Collection Practices Act violations alone entitle you to statutory damages up to $1,000 per case, meaning you don’t need to prove massive financial losses to win. Credit reporting errors that tank your credit score qualify as damages because they directly cost you higher interest rates on mortgages, auto loans, and credit cards. Identity theft and unauthorized charges create actionable claims if you reported them within the required timeframe and can document the fraudulent activity.

Evaluating your case requires reviewing your contracts, statements, communications with the company, and the specific law that was broken. If a lender buried fees in fine print instead of disclosing them upfront under the Truth in Lending Act, that’s a violation. If a debt collector called you before 8 a.m., after 9 p.m., or contacted your employer after you requested they stop, that’s a violation. If your credit report contains an error that the bureau refused to remove after you disputed it in writing, that’s a violation.

Understanding Filing Deadlines and Statutes of Limitations

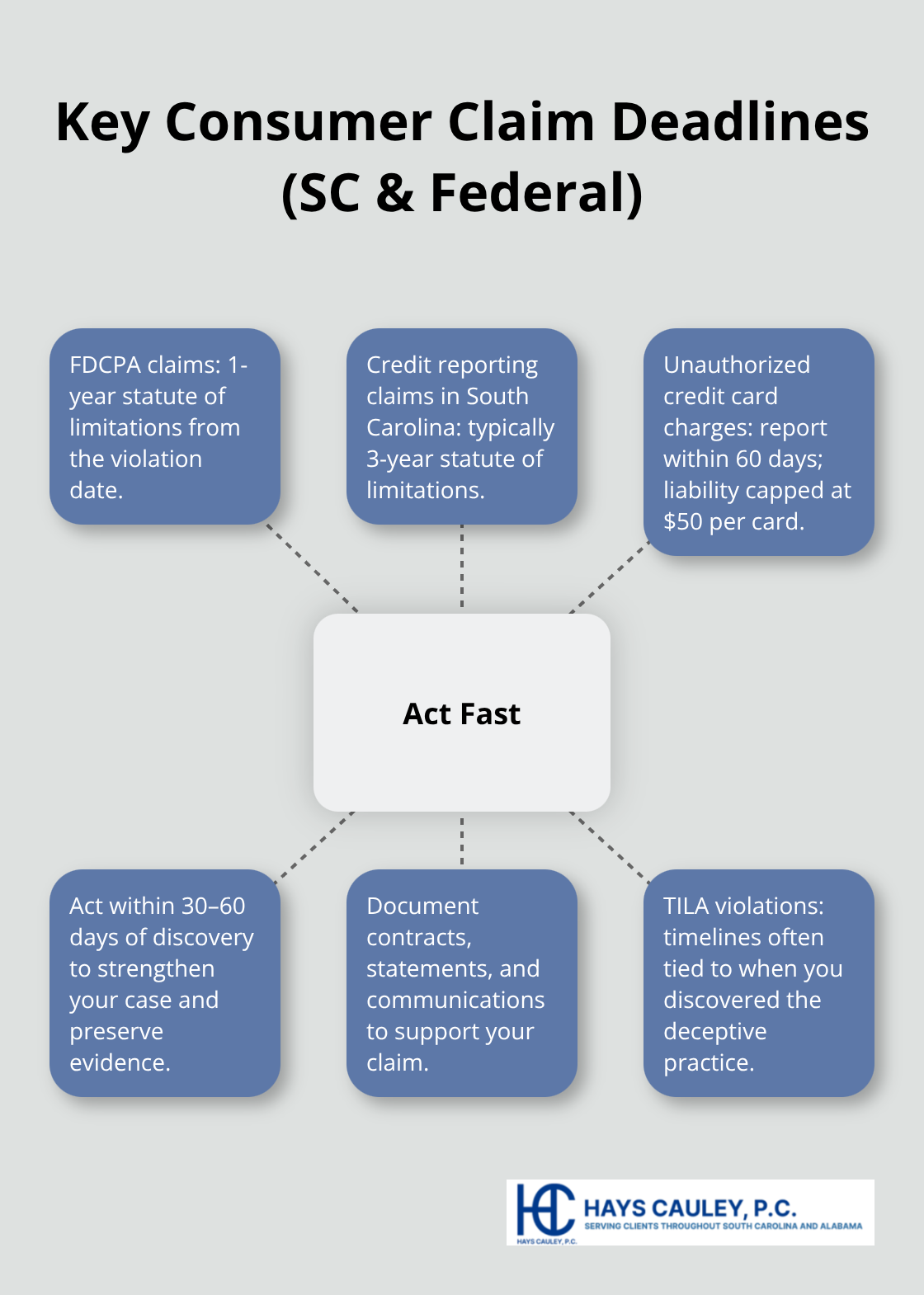

The timeline matters significantly because consumer protection claims have strict filing deadlines that vary by violation type. Credit reporting disputes must be filed within a specific window after you discover the error, and Fair Debt Collection Practices Act claims typically have a one-year statute of limitations from the date of the violation. Identity theft claims and unauthorized charge disputes have their own timelines tied to when you discovered the fraud. Acting within 30 to 60 days of discovering a violation strengthens your case because evidence remains fresh and your memory of events stays accurate. Waiting six months or a year weakens your position because documentation may be lost, memories fade, and you risk missing filing deadlines altogether.

Debt collection violations have a one-year statute of limitations from the date the violation occurred, so if a collector called you illegally today, you have one year to file suit. Credit reporting violations typically fall under a three-year statute of limitations in South Carolina, giving you more time but still requiring prompt action. Truth in Lending Act violations have their own timeframes, often tied to when you discovered the deceptive practice. The moment you identify a violation, contact an attorney because waiting costs you legal leverage and risks missing deadlines entirely.

Types of Damages You Can Recover

Legal action recovers multiple types of damages, not just the money you lost directly. Actual damages include the direct financial harm like overbilling, higher interest rates caused by credit reporting errors, and funds stolen through identity theft. Statutory damages under the Fair Debt Collection Practices Act reach up to $1,000 per violation, and credit reporting violations can result in similar statutory awards. Emotional distress damages compensate you for the stress, anxiety, and time wasted resolving disputes caused by the company’s misconduct.

Many cases settle before trial because companies prefer to avoid the expense and publicity of litigation, and settlements often exceed what victims could recover on their own. The Consumer Financial Protection Bureau’s enforcement actions have recovered over $20 billion for consumers nationwide, illustrating the real money at stake when companies break the law. A settlement or judgment goes directly to you, not to a government agency, meaning you keep the full recovery.

Final Thoughts

Financial violations happen constantly, and most victims never take action because they underestimate the value of their claims or assume the process is too complicated. Your rights matter in these disputes because federal law exists specifically to protect you from predatory lenders, inaccurate credit bureaus, and aggressive debt collectors. A single credit reporting error can cost you thousands in higher interest rates over the life of a mortgage or auto loan, while unauthorized charges and identity theft compound that damage by destroying your ability to borrow money at all.

Debt collection violations create immediate financial recovery opportunities through statutory damages that don’t require you to prove massive losses. The Consumer Financial Protection Bureau’s enforcement actions have recovered over $20 billion for consumers nationwide, proving that companies pay real money when they break the rules. Taking action now protects your credit and your financial future in measurable ways instead of waiting passively while your score tanks.

Contact a consumer rights lawyer who understands South Carolina law and can evaluate your specific situation. We at Hays Cauley, P.C. help South Carolina residents fight financial violations through credit reporting disputes, identity theft claims, and debt collection lawsuits. Visit Hays Cauley, P.C. to schedule a free consultation and discuss your case with someone who knows how to hold financial companies accountable.