Identity theft can happen to anyone, and the aftermath feels overwhelming. We at Hays Cauley, P.C. understand the stress and confusion victims face when their personal information is compromised.

The good news is that identity theft recovery steps exist, and you can take action immediately to limit the damage. This guide walks you through what to do right now, how to repair your credit, and how to protect yourself going forward.

Act Within 24 Hours of Discovery

The first day after discovering identity theft determines how much damage you’ll face. Contact your bank and credit card companies immediately, not tomorrow or next week. Tell them directly that fraud occurred on your account. Most banks can freeze or close compromised accounts within minutes, stopping unauthorized charges before they accumulate. The Federal Reserve found that victims who reported fraud within one day limited losses significantly compared to those who waited weeks.

Document Everything

Ask each financial institution for a fraud affidavit and keep detailed records of every conversation, including the date, time, and representative’s name. Request written confirmation of the fraud report and what steps they’re taking. This documentation protects you later when you dispute fraudulent accounts or file claims.

Alert the Credit Bureaus

Next, call the three major credit bureaus-Equifax, Experian, and TransUnion-to place a fraud alert on your credit file. A fraud alert tells lenders to verify your identity before opening new accounts in your name. This single step blocks most new credit fraud immediately. You can place an alert by calling just one bureau, and they’re required to notify the others. The alert lasts one year and is free.

Protect Your Tax Identity

If you suspect tax-related identity theft specifically, get an Identity Protection PIN from the IRS to prevent someone from filing a tax return with your Social Security number. This step takes minutes online and provides genuine protection against tax fraud.

File Your Official Report

The FTC’s IdentityTheft.gov site lets you report identity theft and create a personalized recovery plan in under 10 minutes. This report is legally recognized and helps when disputing fraudulent accounts. Print and save this report because you’ll reference it constantly over the next months. Include it with dispute letters to creditors and credit bureaus. The FTC also provides sample letters you can use to communicate with companies about fraudulent accounts, saving you time writing originals.

South Carolina residents can also contact the Identity Theft Unit directly at IDTheftHelp@scconsumer.gov, 800-922-1594 toll-free, or 803-734-4200 for additional state-level support. If your identity theft involves employment fraud or a fraudulent W-2, contact the Social Security Administration separately. With these immediate actions completed, you’re ready to examine the damage more closely and repair your credit records.

Checking Your Credit Reports for Fraud

Start pulling your credit reports from Equifax, Experian, and TransUnion within three to five days of filing your FTC report. You’re entitled to one free report annually from each bureau through AnnualCreditReport.com, the official government site. Third-party sites that claim free reports but charge subscription fees should be avoided. Once you have all three reports, print them and read every single line. Look for accounts you didn’t open, credit inquiries from companies you never contacted, and addresses that aren’t yours. Identity thieves often open store credit cards, payday loans, or cell phone accounts because these approvals happen quickly and with minimal verification.

The Bureau of Justice Statistics found that unauthorized use of existing accounts represented the most common identity theft type, but opening new accounts in your name ranks second. Check both your credit history section and the inquiries section carefully. A hard inquiry from an unknown lender signals that someone applied for credit in your name.

Dispute Fraudulent Entries in Writing

Once you identify fraudulent accounts or charges, dispute them with the credit reporting agencies in writing. Send a dispute letter to each bureau that’s reporting the false information, referencing your FTC report number. The FTC provides sample dispute letters that you can customize with specific account details. Credit bureaus must investigate disputes within 30 days and remove information they can’t verify as accurate. Send your dispute letters via certified mail with return receipt so you have proof of delivery. Written disputes create a legal paper trail that phone calls cannot match. Contact the creditors directly as well, not just the credit bureaus. Tell them the account is fraudulent and include your FTC identity theft report. Creditors often respond faster than bureaus because they want to recover losses and avoid liability. Request written confirmation that they’ve closed the fraudulent account and removed it from your credit report. This dual approach of disputing with both bureaus and creditors accelerates the removal process significantly.

Track Removals and File Second Disputes

After filing disputes, check your credit reports again in 60 days to confirm removals. Some fraudulent accounts disappear quickly while others require multiple dispute rounds. If an item remains after the initial 30-day investigation period, file a second dispute with additional documentation. Keep detailed records of every dispute letter, response, and phone call with dates and names. This documentation becomes essential if you need legal help later. Persistence matters more than speed in credit repair. Some victims give up after one dispute attempt, but the agencies count on this. Stay organized, follow up consistently, and don’t accept the first no from a credit bureau. As you work through credit repair, your attention must shift toward preventing future fraud through account monitoring and security upgrades.

Staying Protected After Recovery

Monitor Your Credit Quarterly

Credit monitoring becomes non-negotiable after identity theft because fraudsters often strike twice. Set up free credit monitoring through AnnualCreditReport.com, which lets you pull one report every four months from each bureau instead of waiting a full year. This rotating schedule catches new fraud faster than waiting for your annual report. The Federal Trade Commission also offers free credit monitoring for one year to identity theft victims through IdentityTheft.gov when you file your report. Check your reports quarterly and look specifically for new hard inquiries, unfamiliar accounts, or address changes. Many victims miss second waves of fraud because they assume the problem ended after the first discovery.

Freeze or Lock Your Credit

Credit freezes and credit locks provide stronger protection than fraud alerts because they block all new credit applications, not just those requiring verification. South Carolina residents can place a free credit freeze through each bureau by submitting a request online or by mail. A freeze remains active until you remove it, making it ideal for long-term protection. Credit locks work similarly but through subscription services like Equifax Lock, Experian IdentityWorks, or TransUnion TrueIdentity, which typically cost between 10 and 20 dollars monthly but add extra monitoring and restoration services. South Carolina law does not charge for freezes, so paid locks are optional unless you want the additional monitoring features.

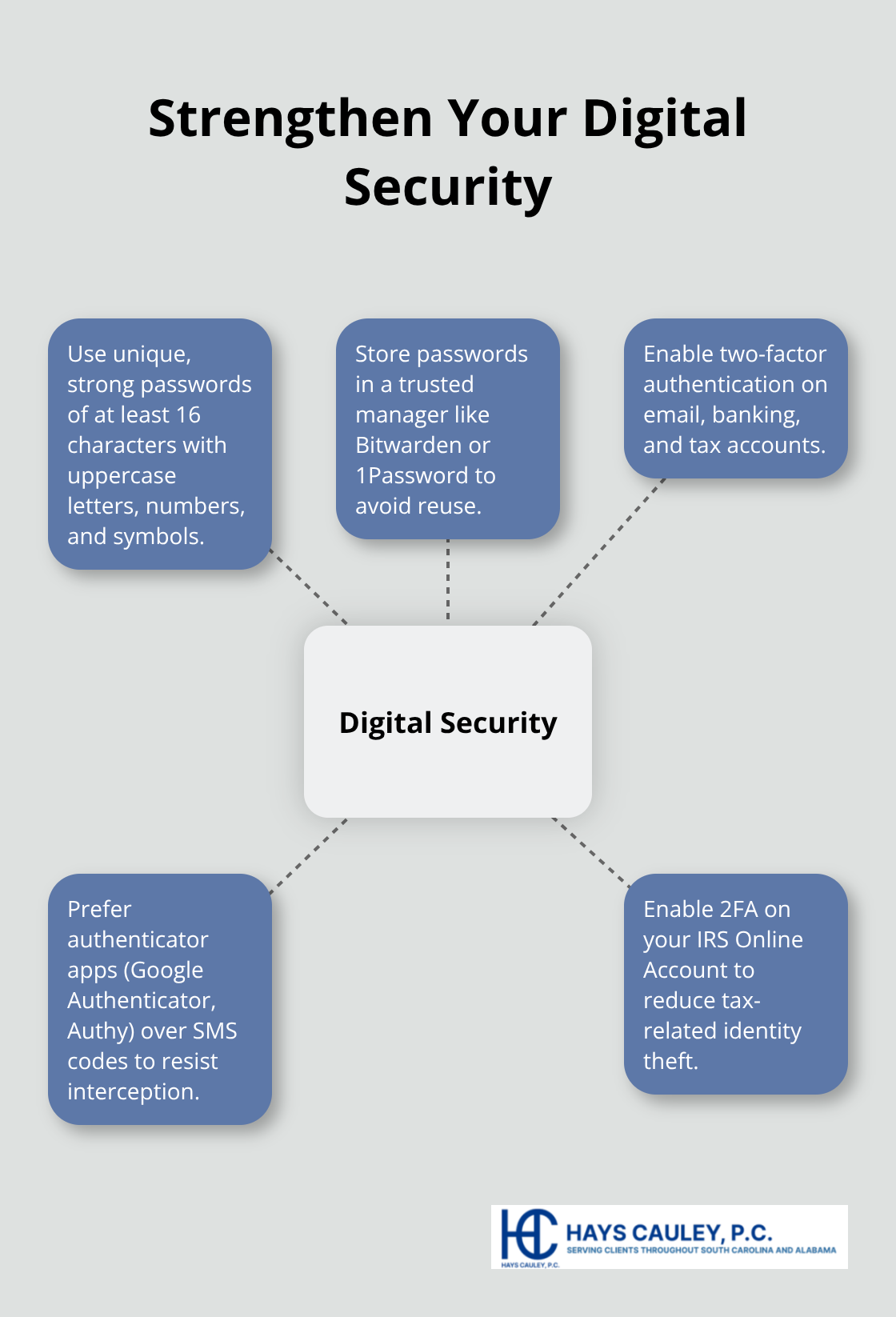

Strengthen Your Digital Security

Your digital security directly impacts identity theft risk because weak passwords and single-factor authentication create easy entry points for criminals. Change all passwords for financial accounts, email, and sensitive services to unique combinations of at least 16 characters that include uppercase letters, numbers, and symbols. Use a password manager like Bitwarden or 1Password to store these securely instead of reusing passwords across accounts. Enable two-factor authentication on every account that offers it, particularly your email, banking, and tax accounts. Two-factor authentication requires a second verification step beyond your password, typically through an authenticator app like Google Authenticator or Authy rather than text messages, which hackers can intercept.

The IRS specifically recommends enabling two-factor authentication on your IRS Online Account to prevent tax-related identity theft.

Secure Your Mobile Devices

Update your smartphone security by enabling automatic lock after five minutes and using a strong PIN or biometric unlock instead of predictable patterns. Mobile devices represent a common entry point for attackers, so this foundational security work prevents future incidents more effectively than any monitoring service alone. Review your financial accounts and passwords immediately after identity theft recovery completes to catch any remaining vulnerabilities before criminals exploit them.

Final Thoughts

Identity theft recovery steps span weeks and months, not days. The immediate actions you took in the first 24 hours stopped the bleeding, but the real work happens as you repair your credit and rebuild your defenses. Most victims complete the core recovery process within 60 to 90 days, though monitoring and vigilance continue indefinitely.

Ongoing vigilance isn’t paranoia-it’s practical protection. Check your credit reports quarterly using the rotating schedule through AnnualCreditReport.com, monitor your financial accounts weekly for unauthorized activity, and review your tax account annually before filing season. Set phone reminders for these tasks because consistency prevents second waves of fraud that many victims miss, and the criminals who stole your information once know your vulnerabilities and may try again months or years later.

Resources remain available throughout your recovery journey, and Hays Cauley, P.C. helps consumers navigate credit reporting, identity theft, and related issues when disputes stall or complications arise. The FTC’s IdentityTheft.gov site provides updated guidance and sample letters for disputes, while South Carolina’s Identity Theft Unit continues supporting you at IDTheftHelp@scconsumer.gov or 800-922-1594. You don’t have to handle this alone, and professional guidance accelerates recovery when you need it most.