Your credit report shapes whether you get approved for loans, what interest rates you’ll pay, and even whether landlords will rent to you. Errors on your report can linger for years and cost you thousands in higher rates and denied applications.

SC credit report repair doesn’t have to be complicated. We at Hays Cauley, P.C. walk you through the exact steps to dispute inaccuracies, improve your score, and take control of your financial future.

Why Your Credit Report Matters in South Carolina

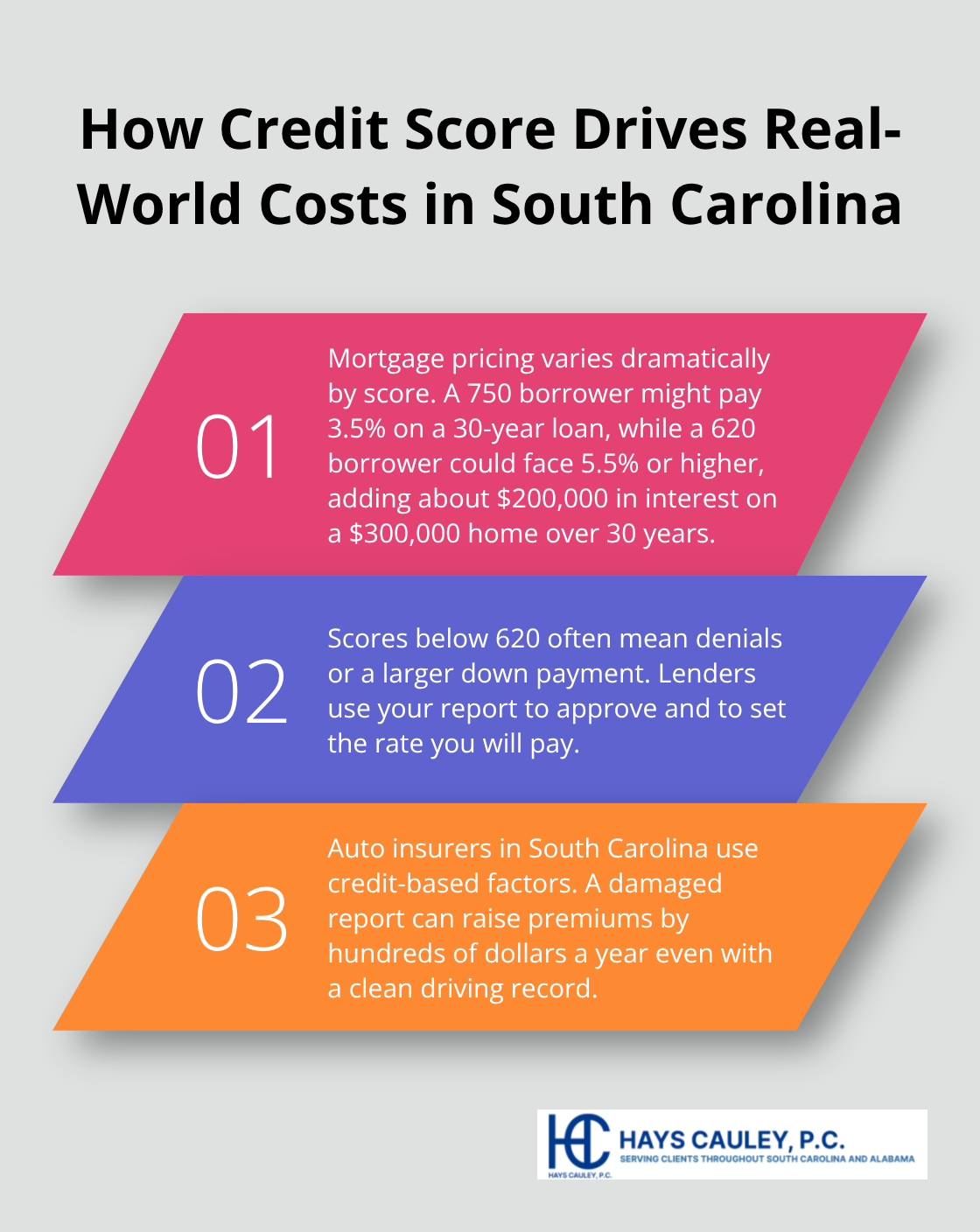

How Your Credit Score Affects Borrowing Costs

A low credit score in South Carolina directly raises your borrowing costs. When you apply for a mortgage, auto loan, or credit card, lenders pull your report to decide whether to approve you and at what interest rate. A score below 620 often triggers loan denials or requires a larger down payment. For those approved, the difference is substantial: a borrower with a 750 score might pay 3.5% on a 30-year mortgage, while someone with a 620 score could face 5.5% or higher. Over 30 years, that 2% difference costs roughly $200,000 more on a $300,000 home.

Auto insurance companies in Charleston and elsewhere also use credit-based factors to set premiums, meaning a damaged report can increase your insurance costs by hundreds of dollars annually even if you’ve never had an accident.

Inaccuracies on Your Report Cost Real Money

Inaccuracies on your credit report are far more common than most people realize. A single wrong late payment, a duplicate collection account, or a balance reported incorrectly can tank your score and stay there for years if you don’t fight it. The Fair Credit Reporting Act requires bureaus to investigate disputes within 30 to 45 days, and inaccurate items must be removed. Yet many people never check their reports and never file disputes, meaning they pay premium rates on every loan they take out. You can pull your credit reports for free once per week from each of the three major bureaus-Equifax, Experian, and TransUnion-through AnnualCreditReport.com. This free weekly access, made permanent during the COVID-19 pandemic, gives you no reason to skip monitoring.

Landlords and Employers Check Your Credit History

In South Carolina, landlords routinely pull credit reports before approving tenants, and a poor report can mean rejection or a demand for a larger security deposit. Some employers also check credit with your written permission, particularly for positions involving financial responsibility or access to sensitive data. A collections account or series of late payments signals to these decision-makers that you’re unreliable with obligations. The South Carolina Department of Consumer Affairs encourages reviewing your report at least once a year to verify accuracy before applying for housing or employment. This simple step protects you from surprises and gives you time to address errors before they influence a landlord’s or employer’s decision about your application.

Now that you understand what’s at stake, the next step is taking action. Pulling your reports and identifying errors is where the repair process begins.

SC Credit Report Repair: A Step-by-Step Plan to Clean Credit – How to Get Your Credit Reports and File Disputes

Pull Your Reports from All Three Bureaus

Start by obtaining your credit reports from all three bureaus at AnnualCreditReport.com or by calling 877-322-8228. The permanent weekly access program allows you to check one bureau per week, rotating through all three over a month, or pull all three at once. This costs nothing and requires only your name, address, Social Security number, and date of birth. Open each report with the mindset of a detective. Verify that your personal information is correct, scan for accounts you don’t recognize, and look for duplicate entries or mixed files where someone else’s debt appears under your name.

Review Your Reports Quarterly for Accuracy

The South Carolina Department of Consumer Affairs recommends reviewing your report at least once yearly, but checking quarterly makes more sense. Inaccuracies are common and stay on file for years without dispute. When you spot an error-a late payment that wasn’t yours, a balance listed higher than it actually is, a charge-off marked when you paid the account, or a collection account you’ve already settled-document it immediately with supporting evidence. Gather bank statements, payment confirmations, receipts, or correspondence showing the correct information. Photograph or scan these documents, then create a clear list noting the specific error, the account number, the date of the mistake, and the correct information. This preparation strengthens your dispute and saves time.

File Disputes with Both the Bureau and the Creditor

File disputes with both the credit bureau and the original creditor who reported the error. Send a dispute letter to the bureau via certified mail with return receipt requested; the CFPB provides sample dispute letter templates on its website that you can adapt with your specific account details. In your letter, clearly identify each inaccuracy, explain why it’s wrong, and request removal or correction. Mail copies of your supporting documents alongside the letter-never send originals. Simultaneously, send a separate dispute notice to the creditor or collection agency that reported the item.

Track Your Dispute Timeline and Follow Up

Bureaus investigate within 30 to 45 days and must provide results within five business days after concluding their investigation. If they find the item inaccurate, it gets deleted or corrected; if they verify it as accurate, you can request a short dispute statement be added to your report. Many people skip notifying the furnisher directly and wonder why their dispute stalls-the dual-notice approach increases the odds of removal. Track all correspondence: keep copies of your letters, document the certified mail tracking numbers, and note the dates you sent each notice. Organized record-keeping separates successful disputes from forgotten ones. If a bureau doesn’t respond within 45 days or if you receive a verification letter you believe is wrong, follow up immediately with another certified letter referencing your original dispute date and demanding a status update.

What Happens After Disputes Are Filed

Once your disputes are filed and investigated, the bureaus will notify you of their findings. Inaccurate items disappear from your report, while accurate but outdated items remain subject to the seven-year reporting limit (ten years for bankruptcy). Understanding how investigations unfold helps you know what to expect during the dispute process. The real power in credit repair comes next: building positive credit history to counterbalance what remains on your file. This is where consistent payment behavior and strategic debt reduction take over from dispute work.

Building Credit That Works for You

Lower Your Credit Utilization Strategically

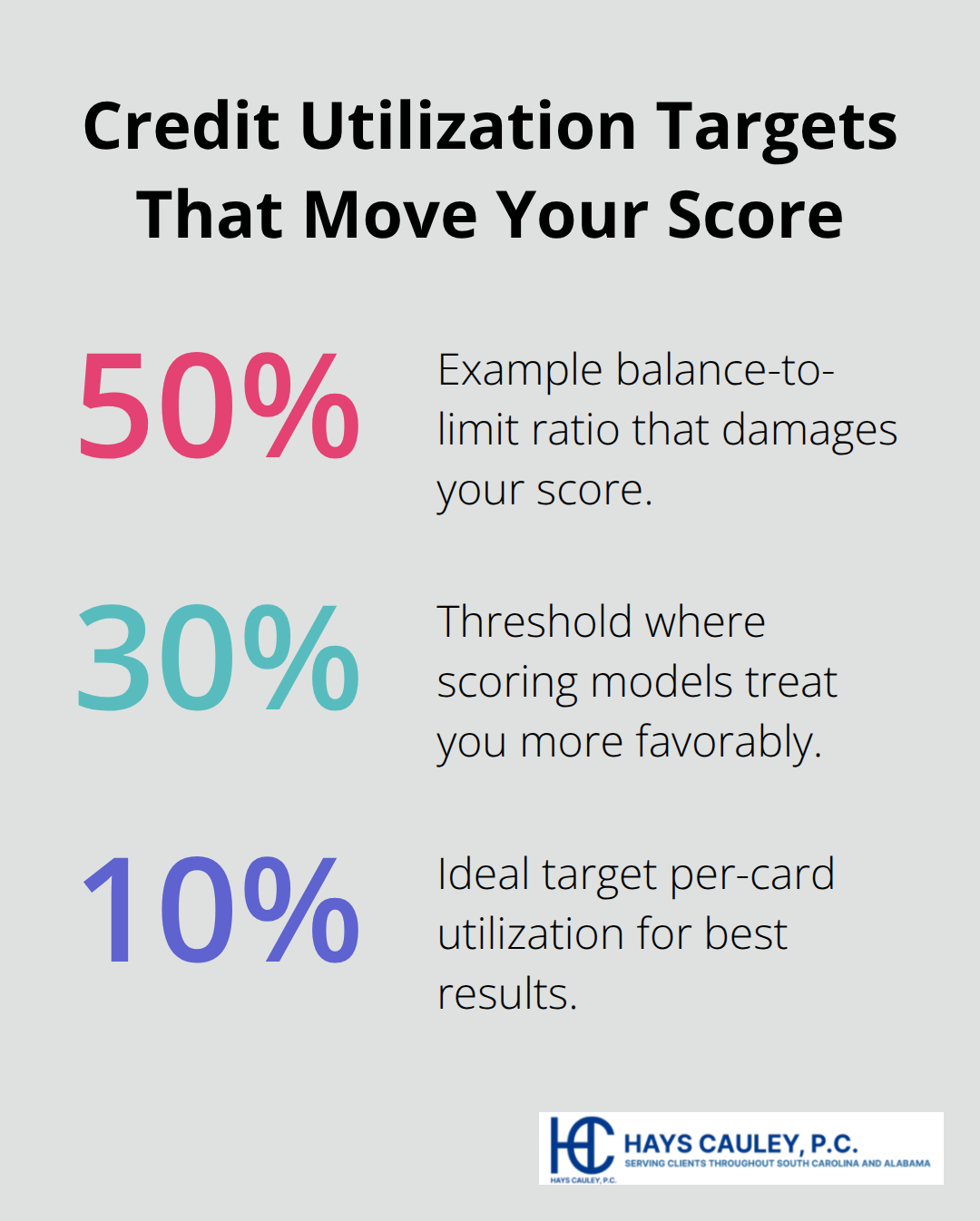

Disputes remove errors, but they don’t build your credit score. The real acceleration comes from strategic debt reduction and consistent payment behavior. Utilization-the percentage of your available credit you actually use-matters far more than most people realize. If you carry a $5,000 balance on a $10,000 credit limit, you sit at 50% utilization, which damages your score. Dropping that balance to $3,000 moves you to 30%, a threshold where scoring models treat you more favorably.

The ideal target sits below 10% utilization on each card, though even reaching under 30% yields noticeable improvements within two to three months.

One practical tactic works immediately: pay your statement balance before the closing date rather than waiting until the due date. This timing prevents the balance from being reported to bureaus in the first place. If you carry balances across multiple cards, focus your payments on the card closest to its limit first. A $7,000 balance on a $10,000 limit damages your score far more than a $3,000 balance on a $15,000 limit, even though the total debt is identical.

Automate Payments to Build History

Automate your payments immediately. The CFPB emphasizes that payment history accounts for 35% of your credit score-the single largest factor-and automation eliminates the human error that causes missed or late payments. Set up automatic transfers from your checking account to cover at least the minimum on every card by the due date. This single change prevents the spiral where one missed payment triggers late fees, higher interest rates, and a negative mark that stays for seven years.

After you establish six to twelve months of on-time payments with low balances, your score will climb noticeably. Consistent payment behavior compounds over time, rewarding discipline with measurable score gains.

Add New Credit Accounts to Accelerate Rebuilding

Some people focus only on paying down debt without adding new positive credit. This approach is slower. Secured credit cards or credit-builder loans accelerate rebuilding because they create fresh tradelines-new accounts with clean payment history. A secured card requires a cash deposit (typically $200 to $2,500) that becomes your credit limit, and monthly payments are reported to all three bureaus. After twelve months of on-time payments, many issuers convert the account to an unsecured card and return your deposit.

Services like Experian Boost allow you to add on-time rent and utility payments to your credit file, though not all lenders factor this data into their decisions. The cost varies, so weigh whether the potential score gain justifies the fee.

Combine Dispute Action with Financial Discipline

Credit repair combines legal action against errors with disciplined financial behavior. Disputes clear the record; consistent payments and low utilization rebuild it. The South Carolina consumer protection landscape offers resources to support your efforts, and we at Hays Cauley, P.C. stand ready to help consumers navigate credit reporting and debt-related challenges when disputes become complex or when creditors resist legitimate removal requests.

Final Thoughts

SC credit report repair produces measurable results within months when you combine dispute action with disciplined financial behavior. Pulling your reports takes one week, identifying errors and gathering documents takes another one to two weeks, and filing disputes triggers 30 to 45-day investigations where most inaccuracies are removed or corrected. Building positive credit through on-time payments and low utilization compounds over six to twelve months, while negative items fall off after seven years-but your score improves substantially long before that timeline ends.

A clean credit report transforms your financial life by lowering interest rates on mortgages and auto loans, securing rental approvals without inflated deposits, and demonstrating financial responsibility to employers and insurers. The process demands attention to detail and persistence, but the payoff-regaining control over your financial future instead of paying penalties for errors you didn’t create-makes the effort worthwhile. When disputes stall, creditors resist removal requests, or complex debt situations demand legal guidance, professional support becomes invaluable.

We at Hays Cauley, P.C. help consumers navigate credit reporting, identity theft, and debt-related challenges when repair efforts hit obstacles. If you need guidance navigating South Carolina’s consumer protection landscape, contact Hays Cauley, P.C. for assistance. Serving South Carolina, including Greenville, Columbia and Charleston, we help you take back control of your credit and your financial future.