A wrong tradeline on your credit report can tank your score and lock you out of loans, better interest rates, and job opportunities. We at Hays Cauley, P.C. help South Carolina residents remove wrong tradelines SC and fight back against inaccurate credit reporting.

The good news: you have legal rights, and these errors are removable. This guide walks you through the process, from spotting mistakes to taking action against credit bureaus that refuse to correct them.

How Wrong Tradelines Damage Your Credit Score

Payment History and Credit Utilization Take the Biggest Hits

A wrong tradeline hits your credit score immediately, and the damage compounds over time. The Fair Credit Reporting Act defines a tradeline as any account reported to credit bureaus, and incorrect ones distort the metrics lenders use to assess risk. Your payment history makes up 35 percent of your credit score according to FICO’s scoring model, so a false late payment or missed payment on an account you never opened can drop your score by 100 points or more. If the wrong tradeline shows a high balance, it inflates your credit utilization ratio, which accounts for 30 percent of your score. A single false account reporting $5,000 in debt when your total available credit is $10,000 jumps your utilization from 0 to 50 percent instantly.

Credit Mix and Inquiry Problems Compound the Damage

Credit mix makes up 10 percent of your score, and fraudulent accounts of the wrong type can skew this ratio. If someone opens a credit card in your name but you only have installment loans, that unexpected revolving account changes your mix and lowers your score further. Credit inquiries and account age combine for 15 percent of your score, and wrong tradelines damage both. A fraudulent hard inquiry from an account opening can stay on your report for two years and signals to other lenders that you recently sought credit desperately. Account age matters because older accounts build your credit history length, but a false account created yesterday carries zero history and drags down your average.

Long-Term Financial Consequences Affect Multiple Areas of Your Life

Mortgage lenders may deny you or charge half a percentage point higher interest, which costs $15,000 more on a $300,000 loan over 30 years. Credit card issuers charge higher APRs to applicants with damaged scores, and some employers in South Carolina run credit checks during hiring. Utility companies, phone providers, and landlords also check credit reports, so wrong tradelines can cost you housing, employment, and basic services (even cell phone activation can be denied). The longer a false tradeline sits on your report, the more financial damage accumulates. This reality makes immediate action far more valuable than waiting to see if it disappears on its own. The steps you take now determine whether you regain control of your financial future or watch opportunities slip away.

Steps to Remove Wrong Tradelines From Your Credit Report, Serving South Carolina, Including Greenville, Columbia and Charleston

Obtain Your Credit Report and Identify Errors

Pull your credit reports from all three bureaus-Equifax, Experian, and TransUnion-at AnnualCreditReport.com, the only federally mandated free source. Many people check only one bureau and miss errors on the others, so obtain all three reports and compare them side by side. Mark every discrepancy with dates and account numbers, then note which bureau reported the error. The Federal Trade Commission found that one in five consumers discovered errors on their credit reports, and roughly 34 percent of those errors were significant enough to affect lending decisions.

File a Dispute With the Credit Bureau

Once you identify a wrong tradeline, file a dispute directly with the credit bureau that reported it. The Fair Credit Reporting Act gives you the right to challenge any inaccurate information, and the bureau must investigate within 30 days. Submit your dispute in writing-not by phone-and include copies of documentation proving the account isn’t yours, such as a police report if identity theft occurred, statements showing you never opened the account, or proof that you paid the account off years ago. Credit bureaus process disputes faster when you provide specific evidence rather than vague claims. Include a cover letter explaining which tradeline is wrong, why it’s wrong, and what correction you’re requesting.

Document Everything and Follow Up Aggressively

Documentation separates successful disputes from rejected ones. Keep copies of everything you send to credit bureaus, including the dispute letter, supporting documents, and the date you mailed it via certified mail with return receipt requested. The credit bureau must respond within 30 days with the results of their investigation. If they correct the error, request written confirmation and verify the change appears on your next credit report. If they refuse to remove the error after your first dispute, file a second dispute with additional evidence, as persistence often succeeds where initial attempts fail. The entire removal process typically takes 60 to 90 days from your initial dispute to final correction, though persistence and strong documentation can accelerate results.

When Credit Bureaus Refuse to Correct Errors

If the credit bureau still refuses after a second dispute and you have solid proof the tradeline is false, you may have grounds for legal action under the Fair Credit Reporting Act. Document any financial harm caused by the wrong tradeline, such as denied loan applications or higher interest rates offered, because this information supports potential legal claims. Do not ignore a wrong tradeline hoping it vanishes-take action immediately to protect your score and your financial future. When your own efforts fail to produce results, understanding your legal rights becomes the next critical step in reclaiming your credit.

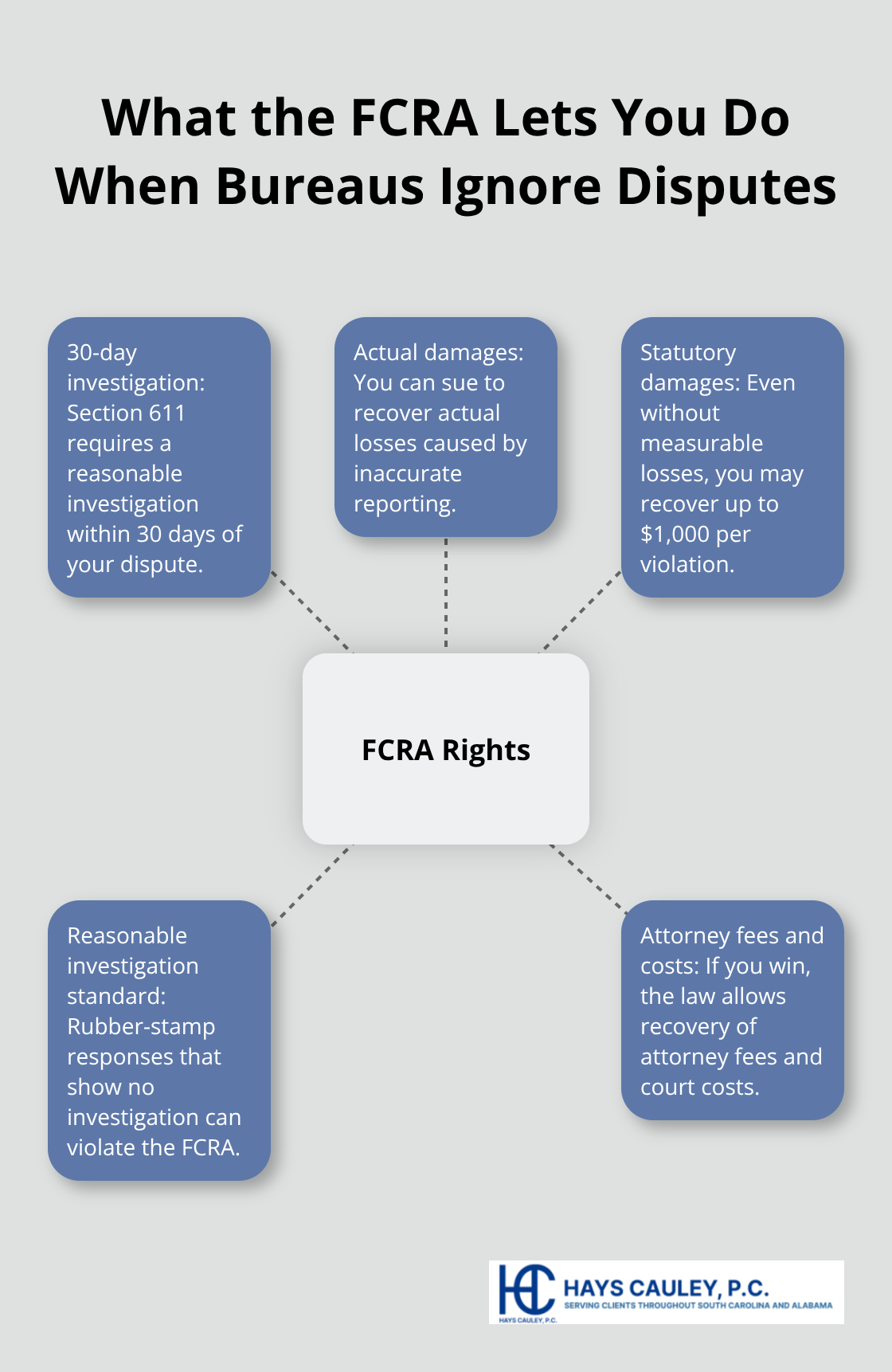

When Credit Bureaus Ignore Your Disputes, Serving South Carolina, Including Greenville, Columbia and Charleston

Your Legal Rights Under the Fair Credit Reporting Act

The Fair Credit Reporting Act gives you specific legal weapons when credit bureaus refuse to correct false tradelines. Section 611 requires bureaus to investigate disputes within 30 days, and if they fail to do so or ignore clear evidence of fraud, you can sue for actual damages plus statutory damages up to $1,000 per violation, regardless of whether you suffered measurable financial harm. This statutory damage provision exists precisely because Congress recognized that some violations cause real injury even when you cannot calculate exact dollar amounts.

Courts have awarded consumers between $500 and $1,000 in statutory damages in cases where credit bureaus knowingly reported false information, and some judgments exceed $10,000 when multiple violations occurred or the bureau showed willful disregard for accuracy. The key is documenting that you provided clear evidence of the error and the bureau either ignored it, conducted no real investigation, or reinvestigated and still refused correction without legitimate reason.

How Credit Bureaus Fail Their Legal Obligations

Credit bureaus often dismiss disputes with form letters that show zero investigation, which creates a strong legal position for consumers. If a bureau claims they investigated but provides no documentation of how they verified the tradeline, that failure itself violates the Fair Credit Reporting Act because the law requires a reasonable investigation, not just a rubber-stamp approval of the original report.

Your initial step should be sending a certified letter to the bureau stating that you are filing a formal dispute under Section 611 of the Fair Credit Reporting Act and demanding written proof of their investigation methodology within 30 days. If they respond with a generic letter or refuse to remove the tradeline without substantive explanation, the next phase involves legal action.

Working With a Consumer Protection Law Firm

A consumer protection law firm handles the legal heavy lifting that credit bureaus count on you not pursuing. Most consumer protection attorneys work on contingency, meaning you pay nothing upfront and the firm recovers fees from the bureau if you win, which removes financial barriers to legal action. The Fair Credit Reporting Act also allows you to recover attorney fees and court costs from the losing party, so bureaus face real financial consequences for fighting cases they should lose.

Hays Cauley, P.C. is a consumer protection law firm dedicated to helping consumers with credit reporting violations. Contact a firm that handles credit reporting cases to evaluate your situation and determine whether you have grounds for legal action.

Building Your Case for Court

Documenting your original dispute, the bureau’s response, any follow-up disputes, and the financial impact of the false tradeline creates the evidence needed to win. A lawsuit typically resolves within six to twelve months, and many bureaus settle rather than defend indefensible positions in court. Strong documentation transforms a rejected dispute into a viable legal claim that puts pressure on the bureau to correct the error or face financial liability.

Final Thoughts

Removing wrong tradelines SC takes 60 to 90 days when you follow the process systematically, from obtaining your credit reports through filing disputes and documenting everything. Your credit score rebounds as false accounts disappear, which means lower interest rates on mortgages, auto loans, and credit cards. A single percentage point reduction on a mortgage saves thousands over the loan term, and improved scores qualify you for better terms across all lending products.

If you haven’t pulled your credit reports yet, start at AnnualCreditReport.com today and identify any wrong tradelines. If you’ve already filed disputes and the bureaus refused correction, legal action becomes your next move because the Fair Credit Reporting Act gives you the right to sue for statutory damages and attorney fees. Beyond borrowing, a clean credit report removes barriers to employment, housing, and utility services that many employers and landlords verify before approval.

If you’re uncertain whether you have grounds for a lawsuit or need guidance navigating the dispute process, contact Hays Cauley, P.C. to evaluate your specific situation at no upfront cost. Your credit report belongs to you, and inaccurate information has no place on it. Take action now rather than watching wrong tradelines damage your financial future for years.