Synthetic identity theft is one of the fastest-growing fraud schemes in America, and it’s harder to spot than traditional identity theft. Criminals build fake identities from scratch using a mix of real and fabricated information, then open accounts and rack up debt in your name.

At Hays Cauley, P.C., we’ve seen firsthand how devastating this crime can be. The good news is that you can take concrete steps to protect yourself before it happens.

Understanding How Synthetic Identity Theft Works

How Criminals Build Fake Identities

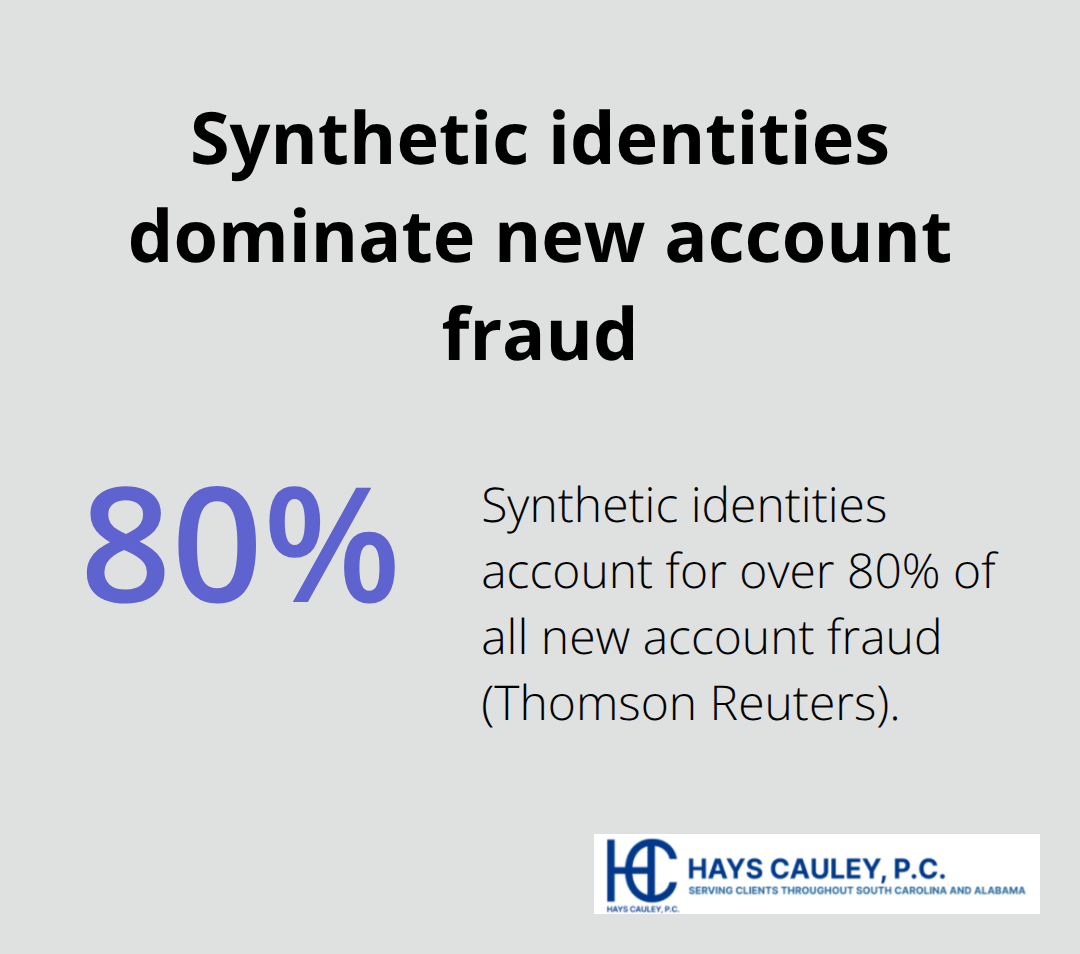

Synthetic identity theft operates differently from traditional identity theft because criminals don’t steal an existing identity-they build a new one from scratch. Thomson Reuters reports that synthetic identities account for over 80% of all new account fraud, making this the fastest-growing form of identity theft. The typical process starts with a stolen Social Security number, often purchased on the dark web or obtained from data breaches at hospitals, banks, or retailers.

Criminals then layer fake information on top: a fabricated name, a different address, and invented employment history. This hybrid approach is deliberately designed to evade detection because the SSN appears legitimate while the surrounding details are entirely fictional.

Some criminals spend months or even years building credit history with this synthetic identity, gradually accumulating positive payment records before maxing out accounts and disappearing. The Federal Trade Commission estimates that synthetic identity fraud causes losses exceeding $20 billion annually, and children, elderly individuals, and homeless people face the highest risk because they’re less likely to monitor their credit regularly.

Why Synthetic Fraud Differs from Traditional Identity Theft

What makes synthetic identity theft particularly dangerous is how it differs from traditional identity theft, where a criminal simply uses your existing name and Social Security number to open fraudulent accounts in your actual identity. With synthetic fraud, you may not realize anything is wrong because the fraudster isn’t using your legitimate identity-they’ve created an entirely new persona. This means unfamiliar accounts won’t appear under your name on your credit report; instead, they’ll show up under the fake name tied to your SSN.

The accounts built on synthetic identities often remain undetected for years because credit bureaus see them as separate profiles with their own credit histories. Unlike traditional identity theft, where damage is immediate and noticeable, synthetic fraud develops slowly and methodically. Losses from synthetic identity fraud reached more than $20 billion per year according to available data, and the crime continues accelerating because automated systems struggle to flag these hybrid identities as fraudulent.

Detection Requires a Different Strategy

You need a different detection strategy than you would for traditional identity theft-monitoring for unfamiliar accounts under your actual name won’t catch a synthetic identity built on your SSN but registered under a completely different person’s details. The fragmented credit files that result from synthetic fraud (mixing legitimate and fraudulent history) make early detection even harder. This is why understanding the warning signs specific to synthetic identity theft matters so much when you’re protecting yourself and your family.

Warning Signs You May Be a Victim: Serving South Carolina, including Greenville, Columbia and Charleston

Debt Collector Calls for Unknown Accounts

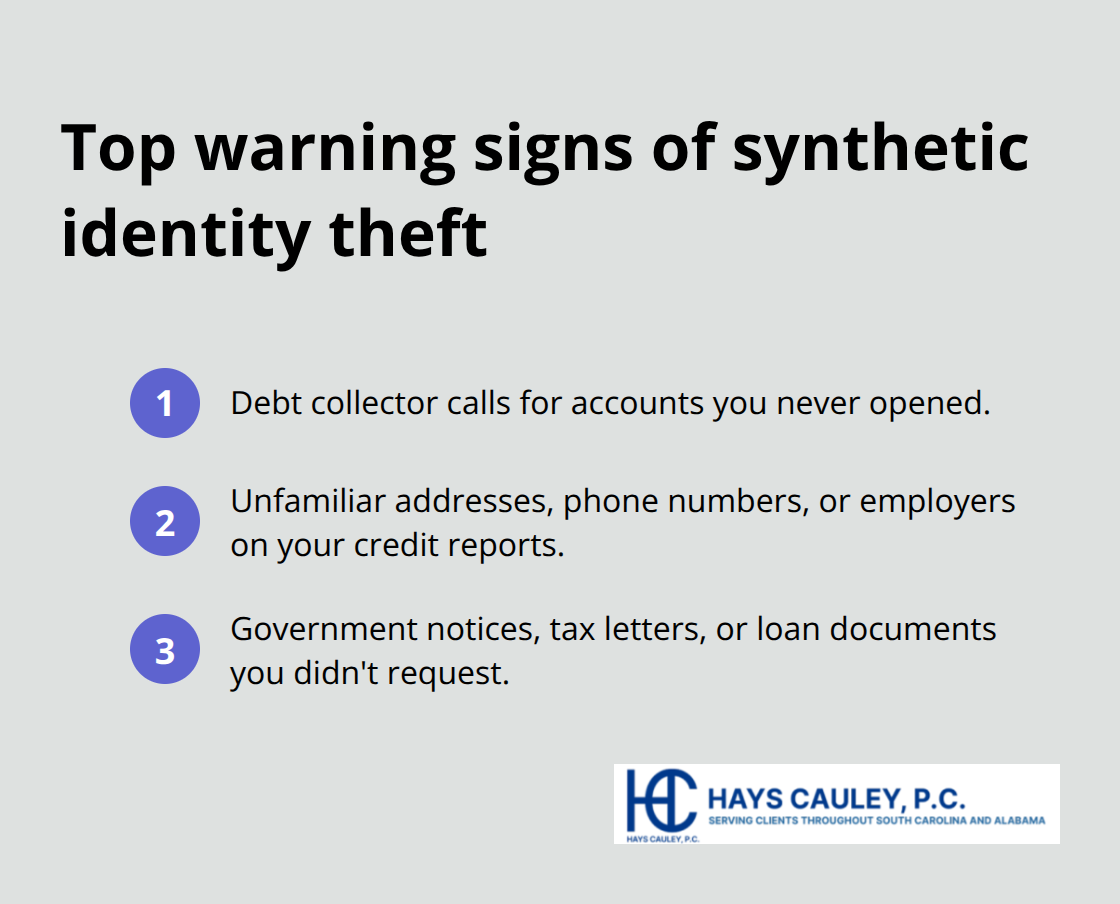

Debt collector calls for accounts you never opened signal that synthetic identity theft may already be underway. If a collector contacts you about a loan, credit card, or line of credit you didn’t apply for, act immediately. The Federal Trade Commission reports that unexpected debt collection activity ranks among the most common warning signs victims notice.

Ask the collector for the account number, creditor name, and details about the alleged debt, then request written verification. Pull your credit reports immediately from AnnualCreditReport.com, which provides free reports from all three bureaus. Look for accounts, inquiries, or payment histories you don’t recognize. Synthetic identities often show up as separate credit profiles or fragmented records mixing legitimate and fraudulent activity under variations of your name or completely unfamiliar names tied to your SSN.

Unfamiliar Addresses and Personal Information

Criminals building synthetic identities register different addresses to establish residency and avoid detection. If your credit report shows an address where you’ve never lived, a phone number you don’t recognize, or employment history you didn’t provide, investigate immediately. These discrepancies appear because fraudsters need to create a convincing profile that passes initial verification checks. Check your report carefully for any variations of your name paired with unfamiliar locations or contact details. Contact the credit bureau to dispute inaccurate information and request an investigation into how these entries appeared on your file.

Government Notices and Unexpected Documents

Government notices you didn’t request also signal trouble. Unexpected IRS letters, benefit statements, or loan documents arriving at your address suggest someone filed applications using your information. Contact the issuing agency to verify whether the activity is legitimate. Some criminals even file business incorporation documents or student loan applications using your SSN and a fabricated identity. Check your name against business registries in your state and monitor tax-related activity closely. These fraudulent filings can damage your credit and create legal complications that take months to untangle.

Taking Action When You Spot Red Flags

If you spot any of these signs, contact IdentityTheft.gov to file a federal identity theft report and start recovery steps immediately. The faster you act, the less damage the fraudster can inflict. Document everything: save copies of debt collection letters, credit reports showing fraudulent accounts, and government notices. This documentation becomes essential when you work with creditors and law enforcement to resolve the fraud. The recovery process requires persistence, but taking swift action limits the scope of the damage and protects your financial future.

Protecting Your Credit and Identity Before Fraud Strikes

Monitor Your Credit Reports Frequently

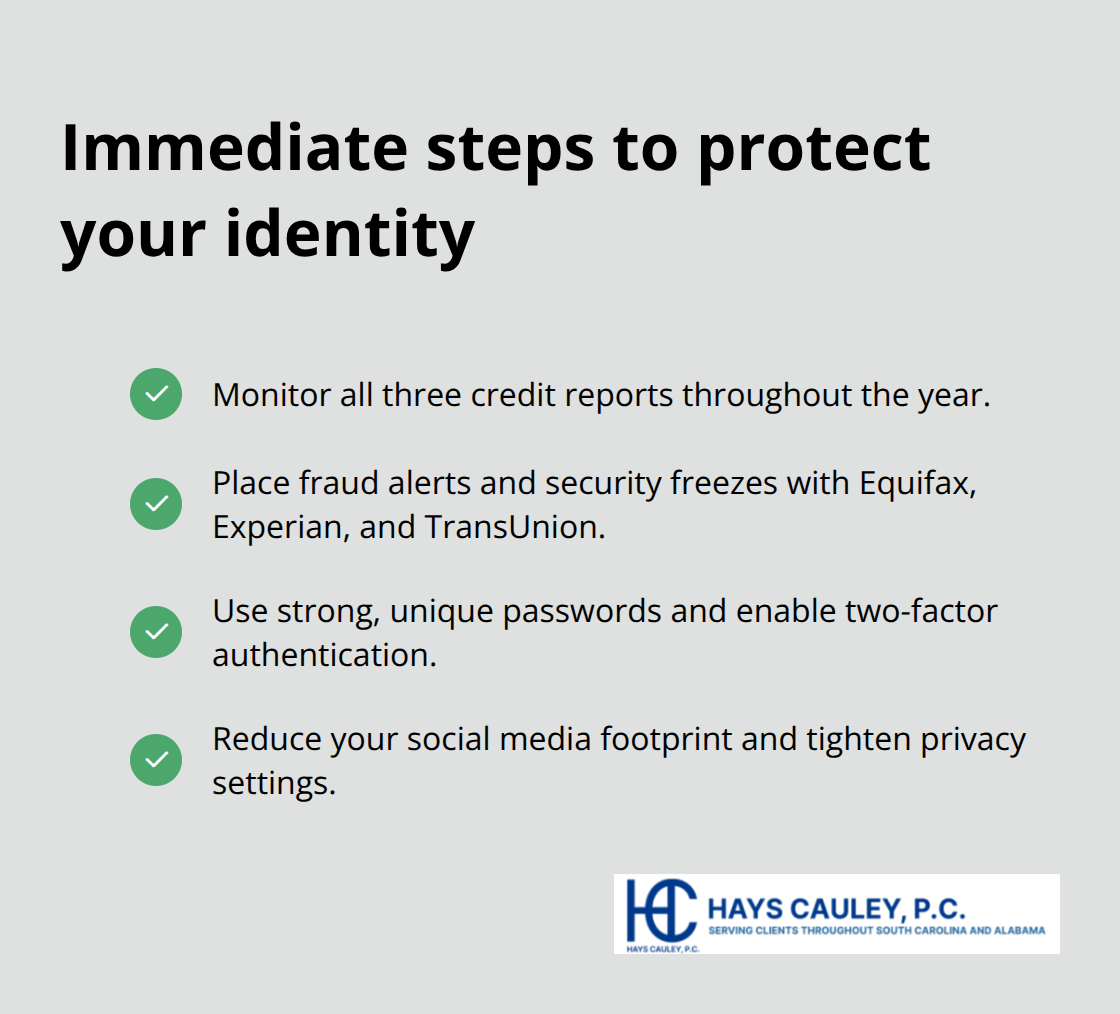

Check your credit reports from all three bureaus at least once every four months instead of waiting for the annual free reports most people rely on. AnnualCreditReport.com provides one free report per bureau per year, but the Federal Trade Commission recommends spacing these checks throughout the year to catch fraudulent accounts faster. Many identity theft protection services now offer weekly or monthly monitoring at reasonable costs, and this frequent oversight catches synthetic identities before they accumulate significant debt.

When you review your reports, examine every address, phone number, employer name, and inquiry listed. Criminals building synthetic identities often leave traces in the form of inquiries from lenders checking credit for accounts you never applied for. These inquiries appear instantly when someone submits an application, so catching them early stops the fraud before accounts open. Once you spot suspicious activity, contact the credit bureau immediately and request a full investigation rather than simply disputing the item. A formal investigation takes time but creates an official record that protects you legally if creditors try to collect on fraudulent debt later.

Use Security Freezes and Fraud Alerts

A fraud alert tells creditors to verify your identity before opening new accounts, which slows down fraudsters but still allows legitimate applications to proceed. A security freeze blocks new credit entirely until you lift it, making it nearly impossible for criminals to open accounts in your name or using your SSN. The Federal Trade Commission states that security freezes are more effective at stopping synthetic identity theft than fraud alerts alone because they eliminate the window of opportunity completely.

You can place a freeze with Equifax, Experian, and TransUnion for free, and the process takes just minutes online. This two-pronged approach (fraud alert plus security freeze) provides the strongest defense against synthetic identity fraud.

Strengthen Your Account Security

Use strong, unique passwords for every financial and email account-a password manager like Bitwarden or 1Password eliminates the temptation to reuse passwords across multiple sites. Enable two-factor authentication on your bank accounts, email, and investment platforms to add a second verification step that hackers cannot bypass even if they steal your password. The National Institute of Standards and Technology recommends authentication apps over text message codes because text-based two-factor authentication remains vulnerable to interception.

Reduce Your Digital Footprint

Limit what you share on social media profiles by reviewing privacy settings and removing personal details like birth date, hometown, phone number, and employer information from your public profiles. Criminals piece together synthetic identities from information scattered across social media, public records, and data breaches, so reducing your digital footprint makes their job substantially harder. This simple step (adjusting your privacy settings) prevents fraudsters from assembling the personal details they need to build a convincing fake identity tied to your SSN.

Final Thoughts

Synthetic identity theft represents a genuine threat to your financial security, but it remains preventable through consistent action. Criminals behind these schemes exploit the gap between account creation and detection, so you must close that window through regular credit monitoring, security freezes, and strong digital habits. Start today by placing a security freeze with all three credit bureaus, enabling two-factor authentication on your email and bank accounts, and scheduling your first credit report review for this week.

These initial steps create immediate protection while you establish longer-term habits like quarterly credit monitoring and privacy adjustments to your social media profiles. Security freezes eliminate the ability to open new credit entirely, strong passwords and two-factor authentication protect your existing accounts from compromise, and reducing your social media footprint removes the raw material criminals use to construct convincing fake identities. The actions that take the least time deliver the most impact, so prioritize them first.

If you discover signs of synthetic identity theft or need guidance navigating recovery, Hays Cauley, P.C. can help you protect your rights and resolve credit reporting issues. We work with consumers facing identity theft and debt-related problems throughout South Carolina, including Greenville, Columbia, and Charleston. Contact us to learn how we support your recovery and safeguard your financial future.