The Fair Credit Reporting Act statute of limitations determines how long negative information can remain on your credit report. Most items disappear after seven years, but some exceptions extend this timeline to ten years.

We at Hays Cauley, P.C. see many South Carolina residents confused about when outdated information should be removed from their reports. Understanding these timeframes protects your financial future and credit score.

FCRA Time Limits for Different Types of Information

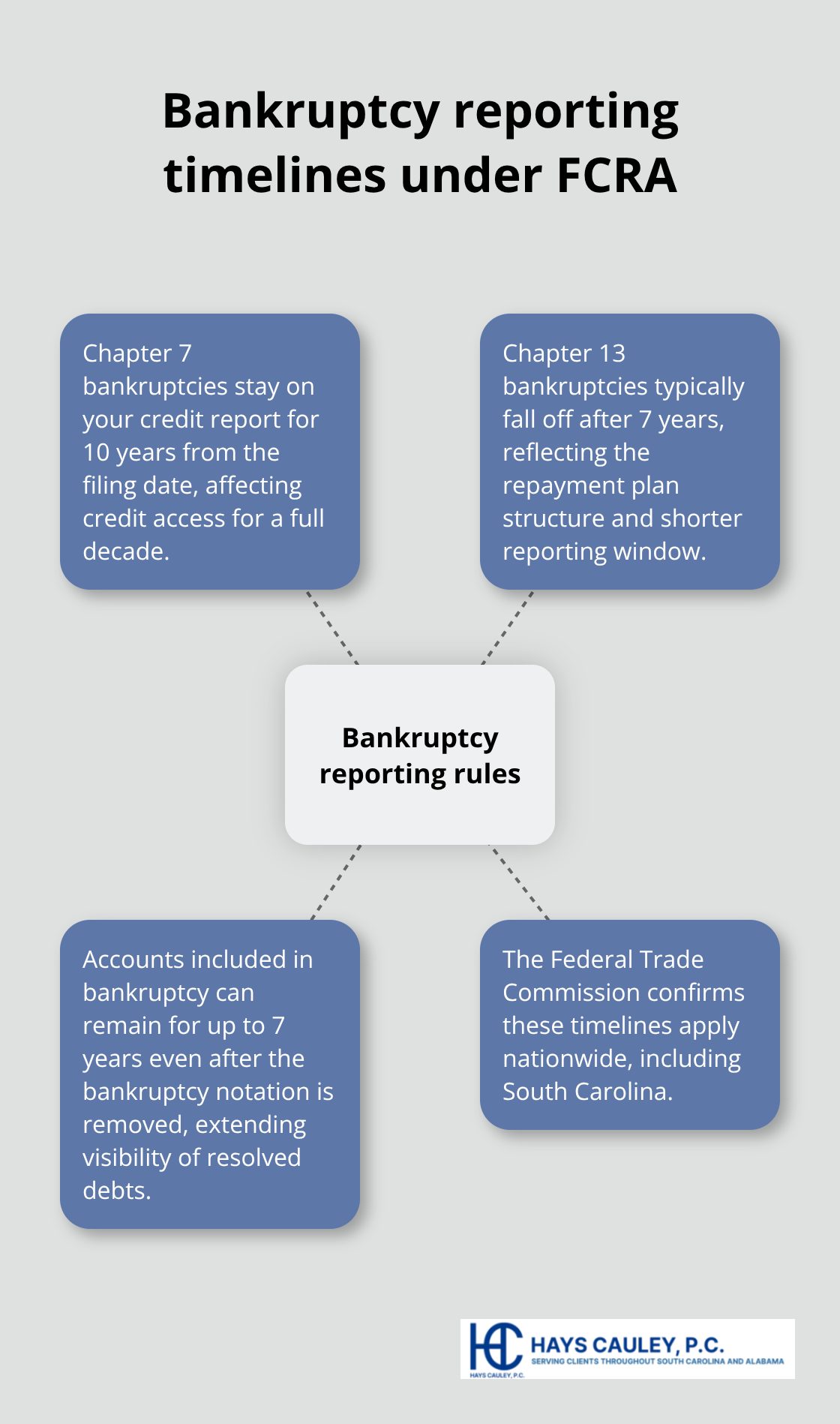

Bankruptcy Records Follow Strict Federal Guidelines

Chapter 7 bankruptcies stay on credit reports for exactly 10 years from the filing date, while Chapter 13 bankruptcies vanish after 7 years. The Federal Trade Commission confirms these timeframes apply nationwide (including South Carolina). Individual accounts included in bankruptcy can remain for the full 7-year period even after the bankruptcy notation drops off.

This creates a situation where your credit report shows resolved debts longer than the actual bankruptcy case.

Civil Judgments and Tax Liens Have Complex Rules

Civil judgments previously stayed on credit reports for 7 years, but the three major credit bureaus stopped reporting most civil judgments in 2017 due to accuracy concerns. Tax liens follow different patterns: paid tax liens must be removed after 7 years, while unpaid liens can remain indefinitely until resolved. South Carolina state tax liens operate under the same federal reporting rules as IRS liens (both follow identical federal guidelines).

Criminal Records Appear Only in Background Checks

Criminal convictions never appear on standard credit reports from Equifax, Experian, or TransUnion. Background check companies can report criminal records indefinitely for most purposes, with no federal time limits under the Fair Credit Reporting Act. However, South Carolina employers cannot consider arrests that did not lead to convictions when those arrests are more than one year old.

Medical Debt Gets Special Treatment

Medical collections receive different treatment than other debts on credit reports. Paid medical collections disappear immediately from most credit reports as of July 2022. Unpaid medical debt cannot appear on credit reports until it reaches 365 days past due (giving patients time to resolve insurance issues). These changes significantly reduce the impact of medical debt on South Carolina consumers’ credit scores.

These time limits become more complex when certain exceptions apply, particularly for high-value transactions and employment situations. Under the FCRA, you generally have two years from discovering the error-or five years from its occurrence-to file suit.

When FCRA Time Limits Don’t Apply in South Carolina

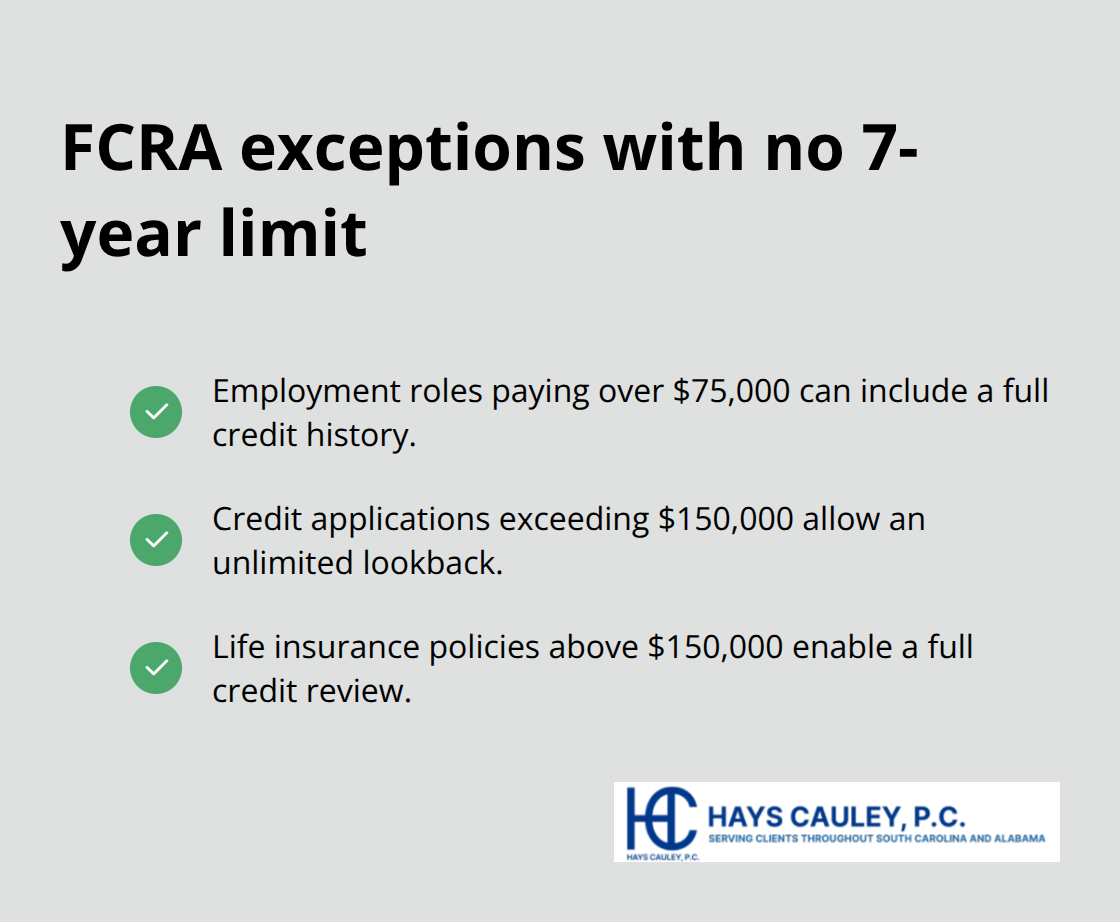

The Fair Credit Reporting Act allows credit bureaus to ignore standard seven-year limits in three specific situations that directly affect South Carolina consumers. These exceptions mean negative information can stay on your credit report indefinitely, which makes it vital to understand when they apply and how to protect yourself.

Employment Positions Above $75,000 Annual Salary

Employers can access your complete credit history without time restrictions when the position pays more than $75,000 annually. The Federal Trade Commission confirms this exception applies to any role that meets this salary threshold, which includes management positions, sales roles with commission potential, and professional services jobs common in Charleston and Columbia.

South Carolina has no state law that limits this practice, so employers routinely pull full credit reports for positions like bank managers, financial advisors, and corporate executives. Your 15-year-old bankruptcy or decade-old collection account becomes visible to potential employers and potentially affects job opportunities.

We recommend that you obtain your employment credit report before job interviews to understand what employers will see. The three major credit bureaus provide employment-specific reports that show exactly what information appears during background checks.

Credit Applications That Exceed $150,000

Credit applications above $150,000 trigger unlimited credit periods. Mortgage lenders, business loan officers, and insurance underwriters can see your entire credit history when they process these applications. This means your Chapter 7 bankruptcy from 2010 remains visible to mortgage lenders in 2025, even though it disappeared from standard credit reports.

South Carolina residents who apply for jumbo mortgages or significant business loans should expect comprehensive credit scrutiny. Banks and credit unions use this exception frequently when they evaluate large loan applications.

Life Insurance Policies Above $150,000

Insurance companies can access unlimited credit history when they write life insurance policies above $150,000. These companies use this exception frequently, as they assess long-term financial stability over decades. Your old financial mistakes remain visible to insurance underwriters regardless of how much time has passed.

This exception affects many South Carolina families who purchase substantial life insurance coverage to protect their dependents. Understanding what information appears on these reports helps you prepare for the underwriting process and address potential concerns before they affect your coverage or premiums.

Your Rights When Information Stays Too Long

The Fair Credit Reporting Act gives you powerful tools to remove information that exceeds legal time limits, but success depends on the right steps at the right time. Most South Carolina consumers wait too long to act or fail to provide adequate documentation, which leads to unsuccessful disputes and continued credit damage.

Start With Direct Credit Bureau Disputes

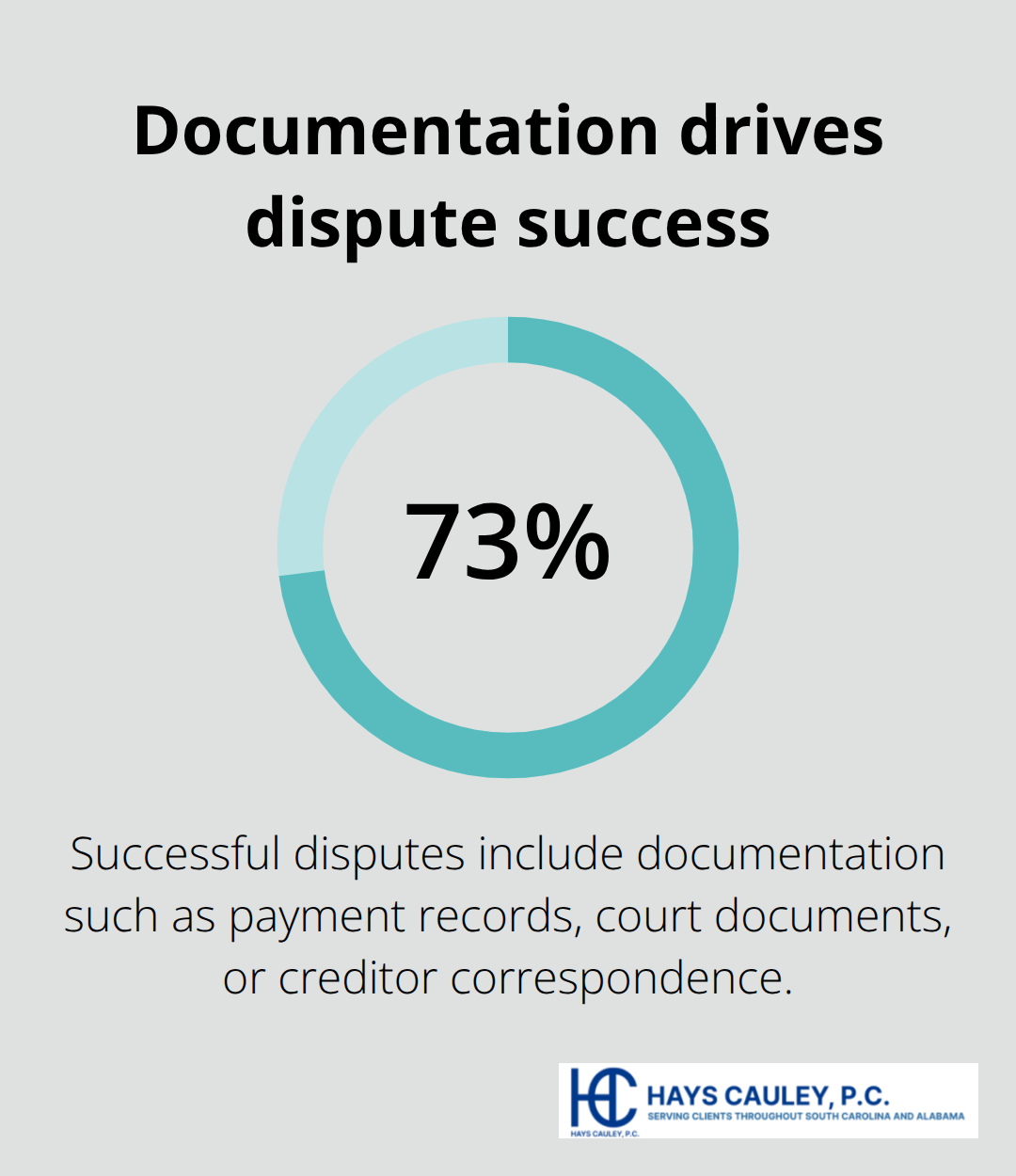

Credit bureaus must investigate disputes within 30 days under federal law, but they reject most disputes that lack specific details or evidence. The Consumer Financial Protection Bureau reports that 73% of successful disputes include documentation like payment records, court documents, or correspondence from creditors.

Submit separate disputes to all three bureaus because they maintain independent databases and may respond differently to identical claims. Use certified mail for paper disputes or keep screenshots of online submissions, as credit bureaus sometimes claim they never received dispute requests.

File disputes immediately after you discover outdated information because the Fair Credit Reporting Act’s two-year statute of limitations starts when you discover the violation, not when it occurred.

Document Everything Before You File Legal Claims

Federal courts dismiss most FCRA lawsuits due to insufficient documentation, so gather evidence before you contact any attorney. Save copies of your credit reports that show the outdated information, correspondence with credit bureaus, and any responses to your disputes.

The Federal Trade Commission requires credit bureaus to provide written results of their investigations, so keep these letters as proof of their actions. Calculate your actual damages from the outdated information, such as higher interest rates, denied credit applications, or lost employment opportunities.

Know Your Legal Options Under FCRA

Courts award up to $1,000 per violation for willful FCRA violations, but you must prove the credit bureau knew the information was outdated and chose to keep it anyway. You can also recover actual damages (like higher loan costs) plus attorney fees if you win your case.

The statute of limitations gives you two years from discovery or five years from the violation date (whichever comes first) to file suit. This tight timeline makes immediate action necessary when credit bureaus refuse to remove outdated information after proper disputes.

Final Thoughts

The Fair Credit Reporting Act statute of limitations protects South Carolina consumers by removing most negative information after seven years, with bankruptcies extending to ten years. These protections disappear for employment positions above $75,000, credit applications exceeding $150,000, and life insurance policies over $150,000. Credit bureaus must follow these federal time limits regardless of state location.

Regular credit monitoring prevents outdated information from harming your financial opportunities. Check your reports annually through AnnualCreditReport.com and dispute any information that exceeds legal time limits immediately. The two-year statute of limitations for FCRA violations starts when you discover the error (making prompt action necessary).

Credit bureaus sometimes refuse to remove outdated information despite proper disputes, which makes legal action necessary. Document all correspondence and calculate actual damages before you pursue litigation. We at Hays Cauley, P.C. help South Carolina consumers navigate credit reporting violations and protect their financial rights through legal representation when credit bureaus ignore disputes or continue reporting information beyond legal time limits.