A mistake on your credit report can cost you thousands of dollars in higher interest rates or denied loan applications. Yet most people don’t know they have the legal right to dispute credit report errors and get them removed.

At Hays Cauley, P.C., we help South Carolina residents, including those in Greenville, Columbia, and Charleston, fight back against inaccurate information that damages their financial lives. This guide walks you through your dispute credit report rights and the concrete steps to reclaim your credit score.

Where Credit Report Errors Come From and Why They Stick Around, Serving South Carolina, Including Greenville, Columbia, and Charleston

How Errors Enter Your Credit File

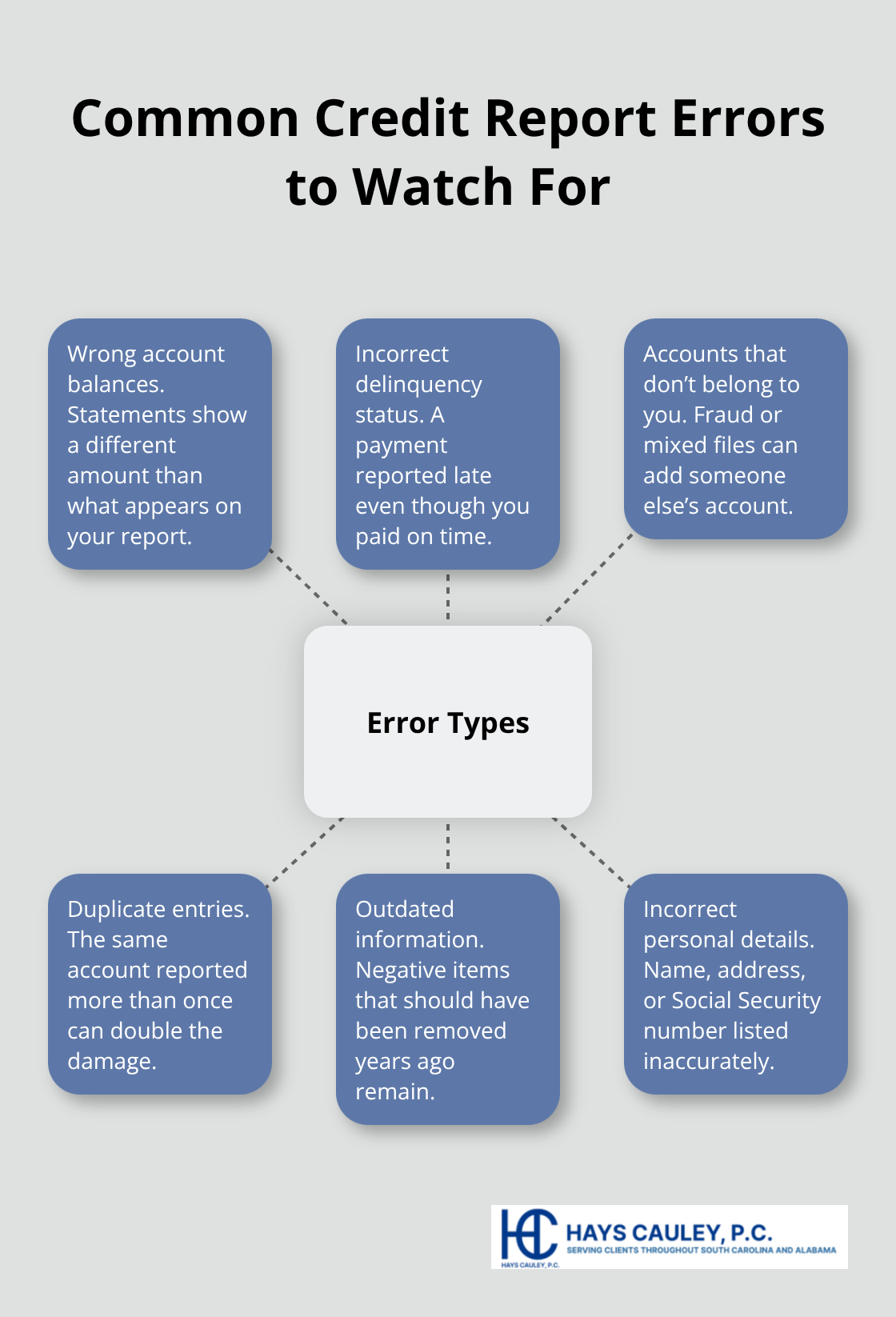

Credit bureaus process hundreds of millions of transactions daily, and with that volume comes inevitable mistakes. The three major credit reporting agencies-Equifax, Experian, and TransUnion-compile data from creditors, lenders, employers, and public records. When any of these sources reports information incorrectly, your credit file suffers. Common errors include wrong account balances, delinquency status that doesn’t match reality, accounts that don’t belong to you, duplicate entries of the same account, outdated information that should have been removed years ago, and incorrect personal information like your name, address, or Social Security number.

The Federal Trade Commission found that credit reports may differ significantly across bureaus, meaning an error on one file might not appear on another. This fragmentation creates real problems because you could face denial based on inaccurate data while maintaining a clean report elsewhere.

The Real Cost of Inaccurate Information

The impact extends far beyond a number on a screen. An error on your credit report directly lowers your credit score, which determines whether you qualify for loans and mortgages and what interest rates you’ll pay. A single misreported late payment can cost you thousands of dollars in higher interest rates over the life of a loan.

Lenders see negative marks and either reject your application outright or offer terms significantly worse than what you deserve. Insurance companies also pull credit reports when underwriting policies-some states allow them to use credit scores in determining premiums, meaning an error could increase your insurance costs. Employers occasionally review credit reports during hiring, and inaccurate delinquencies or accounts in collections can eliminate you from consideration even though you’ve managed your finances responsibly.

Why Bureaus Don’t Fix Errors Without Pressure

The credit bureaus have no financial incentive to remove errors on their own. They generate revenue from selling reports, not from accuracy. This means errors often stay on your file indefinitely unless you actively dispute them.

South Carolina law requires that when you dispute an item, the credit reporting agency must reinvestigate within 30 days at no cost to you. If the item is found inaccurate, they must correct it in their records and notify any creditors or employers that received the report in the last six months. However, this only happens when you take action.

Willful violations of South Carolina’s identity theft and credit reporting laws result in three times your actual damages or at least three thousand dollars per incident, plus attorney’s fees and costs. Negligent violations expose violators to actual damages or at least one thousand dollars per incident, plus attorney’s fees. These penalties exist because credit bureaus have real obligations, but they only enforce them when confronted with disputes backed by documentation.

Getting Results Requires Documentation and Persistence

Contacting the bureau directly through their website or phone line often yields slow results. The process moves faster when you submit a written dispute with supporting documents and follow up persistently. Written disputes create a paper trail that credit bureaus cannot ignore, and documentation transforms your complaint from a casual inquiry into a formal legal claim.

Understanding where errors originate and why bureaus resist correction sets the stage for effective action. Your next step involves learning exactly what rights the Fair Credit Reporting Act grants you and how to exercise them.

Your Legal Rights Under Federal Law, Serving South Carolina, Including Greenville, Columbia, and Charleston

What the Fair Credit Reporting Act Guarantees You

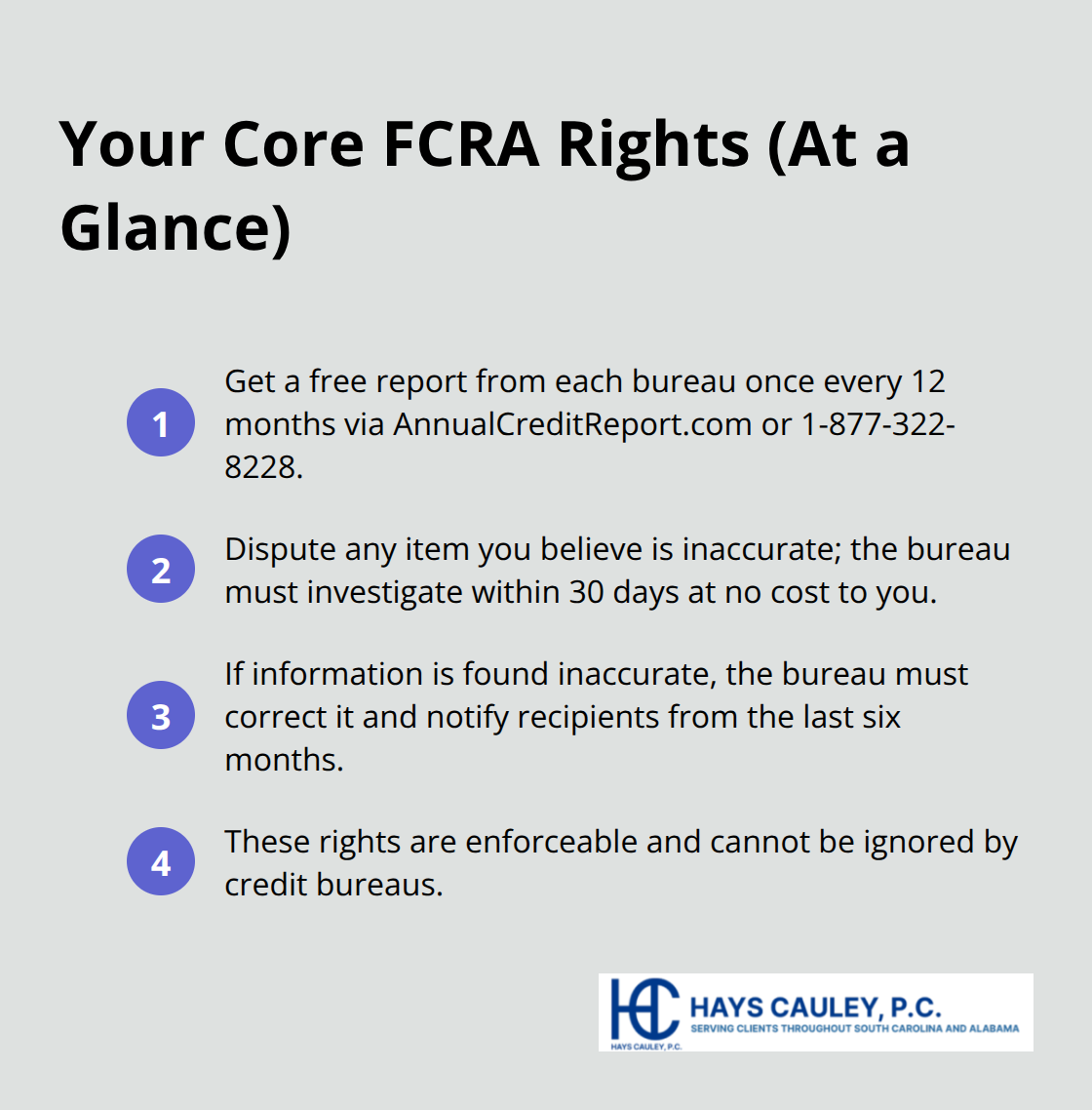

The Fair Credit Reporting Act grants you specific, enforceable rights that credit bureaus cannot ignore. You have the right to access your credit report from each of the three major agencies once every 12 months for free through the Annual Credit Report Request Service at www.annualcreditreport.com, or by calling 1-877-322-8228. You also have the right to dispute any information you believe is inaccurate, and the credit reporting agency must investigate your claim within 30 days at no cost to you. If the agency finds the information inaccurate during reinvestigation, they must correct it in their records and notify any creditors or employers that received the incorrect report within the last six months.

South Carolina law reinforces these protections, requiring credit bureaus to follow the same 30-day investigation timeline. The law also protects you if you are a victim of identity theft-you can initiate a law enforcement investigation by reporting to a local agency, which must take your report and provide you with a copy. If an identity thief was arrested or convicted under your identity, you can petition for an expedited judicial determination of factual innocence, potentially leading to expunction of the erroneous conviction. These rights exist because credit bureaus hold enormous power over your financial life, and federal law recognizes that without enforcement mechanisms, errors would persist indefinitely.

How to File a Written Dispute That Gets Results

Phone calls and online forms move slowly. Submit your dispute in writing to the credit bureau by certified mail with return receipt so you have proof of delivery. Include your contact information, the confirmation number from your credit report, the exact account numbers with errors, a clear explanation of what is wrong and why, and copies of supporting documents like bank statements or payment receipts. Request removal or correction of the information explicitly.

The Federal Trade Commission recommends using their dispute letter template to guide your submission. Send the same dispute to the furnisher-the original source who reported the data, such as your bank, credit card company, or landlord-using their specified dispute address. Furnishers generally have 30 days to investigate and respond. If they determine the information is inaccurate or cannot verify it, they must update or remove it and notify all three credit bureaus.

What Happens When the Furnisher Disagrees

If the furnisher finds the information accurate and refuses to change it, you can request that the credit bureaus include a brief statement in your file describing your dispute so future readers understand your position. Throughout this process, keep copies of every letter you send and every response you receive, and document the dates and names of anyone you speak with.

Willful violations by credit bureaus carry penalties of three times your actual damages or at least three thousand dollars per incident, plus attorney’s fees and costs. Negligent violations expose violators to actual damages or at least one thousand dollars per incident, plus attorney’s fees. These penalties mean bureaus have genuine financial incentive to resolve disputes correctly, and they also mean you have legal recourse if a bureau ignores your rights.

When Professional Help Becomes Necessary

The dispute process works for many people, but some situations require more aggressive action. If a credit bureau continues to report inaccurate information after you’ve submitted documentation, or if a furnisher refuses to investigate your claim, you may need legal representation to enforce your rights. We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, pursue claims against credit bureaus and furnishers that violate federal and state law. Understanding your rights and the dispute process positions you to take the next critical step: gathering the specific documentation that transforms a complaint into a winning case.

Practical Steps to Remove Errors from Your Credit Report, Serving South Carolina, Including Greenville, Columbia, and Charleston

Obtain and Review All Three Credit Reports

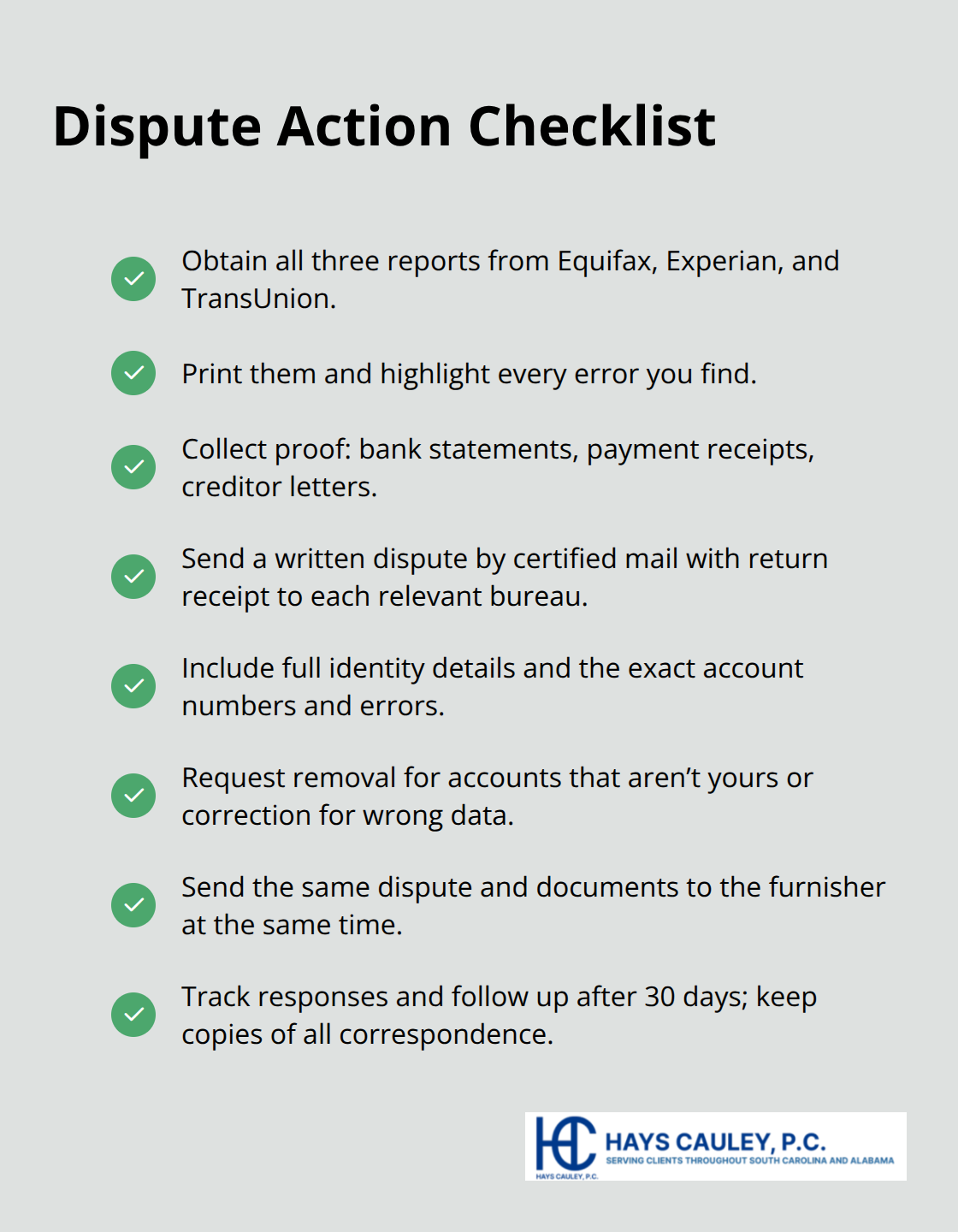

Start by obtaining copies of all three credit reports from Equifax, Experian, and TransUnion through www.annualcreditreport.com or by calling 1-877-322-8228. Print these reports and highlight every error you find. Credit reports often differ across bureaus, so reviewing all three ensures you catch errors that appear on one file but not another. This step takes less than an hour and costs nothing, yet most people skip it entirely.

Gather Documentation That Proves the Error

Next, collect documentation that proves the error exists. If a late payment is reported incorrectly, pull bank statements showing on-time payments from your account. If an account appears that isn’t yours, gather any correspondence from the creditor or your own account records proving you never opened it. If a balance is wrong, collect recent statements from the actual creditor showing the correct amount. The Federal Trade Commission recommends keeping originals in a safe place and sending only copies with your dispute letter. Organize this documentation chronologically so the timeline of your payments or account activity becomes immediately clear to whoever reviews your case.

Write Your Dispute Letter with Specific Details

Submit your dispute in writing via certified mail with return receipt to create an official record. Address your letter to the dispute department of each credit bureau that reports the error. Include your full name, current address, date of birth, and Social Security number so they can locate your file quickly. Reference the specific account number and creditor name, then explain exactly what is wrong. Instead of writing the account shows a late payment, write the account shows a 60-day late payment dated March 2024, but my bank statements prove I paid on February 15, 2024. This specificity forces the bureau to investigate the exact claim rather than dismissing it as vague. Request removal if the account doesn’t belong to you, or correction if the information is simply wrong. Keep a copy of everything you send and note the date you mailed it.

Send Your Dispute to the Furnisher Simultaneously

Send the same dispute with your documentation to the furnisher-the original creditor or debt collector who reported the information. Furnishers have 30 days to investigate under federal law. If they cannot verify the information as accurate, they must correct it or remove it entirely. Many people skip this step and only dispute with the bureau, which slows resolution significantly.

The furnisher investigation often moves faster than the bureau investigation because furnishers have direct access to their own records. If the furnisher corrects the information, they notify all three bureaus automatically, which updates your reports across the board.

Track Your Progress and Document Responses

After 30 days, contact the furnisher in writing to ask for proof they investigated your claim. Document every response you receive with dates and names of representatives. This documentation becomes critical if you later need to pursue legal action against a bureau or furnisher that violates your rights under federal law. Keep copies of every letter you send and every response you receive throughout the entire process.

Final Thoughts

Credit report errors will not fix themselves, and waiting only extends the damage to your financial life. The steps outlined in this guide provide you with concrete tools to challenge inaccurate information and reclaim your credit score. Written disputes with supporting documentation force credit bureaus and furnishers to investigate your claims seriously, and most people who follow this process successfully remove errors within 60 to 90 days.

Some situations demand more than a DIY approach. If a credit bureau continues reporting inaccurate information after you submit documentation, or if a furnisher refuses to investigate your dispute credit report rights claim, you need someone who understands federal law and knows how to hold violators accountable. We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, pursue claims against bureaus and furnishers that violate your rights under the Fair Credit Reporting Act and South Carolina law (many cases qualify for contingency representation, meaning you pay nothing unless we recover damages on your behalf).

Your dispute credit report rights exist because Congress recognized that credit bureaus hold too much power over your financial life without enforcement mechanisms. Contact Hays Cauley, P.C. today for a free consultation about your situation.