A mistake on your credit report can wreck your financial life. Wrong information tanks your credit score, costs you thousands in higher interest rates, and opens the door to identity theft.

We at Hays Cauley, P.C. help South Carolina residents-including those in Greenville, Columbia, and Charleston-fight back against credit reporting errors. This guide shows you how to spot inaccurate data and use your FCRA data accuracy rights to fix it.

How Inaccurate Credit Reports Damage Your Financial Life

A Single Error Costs Thousands

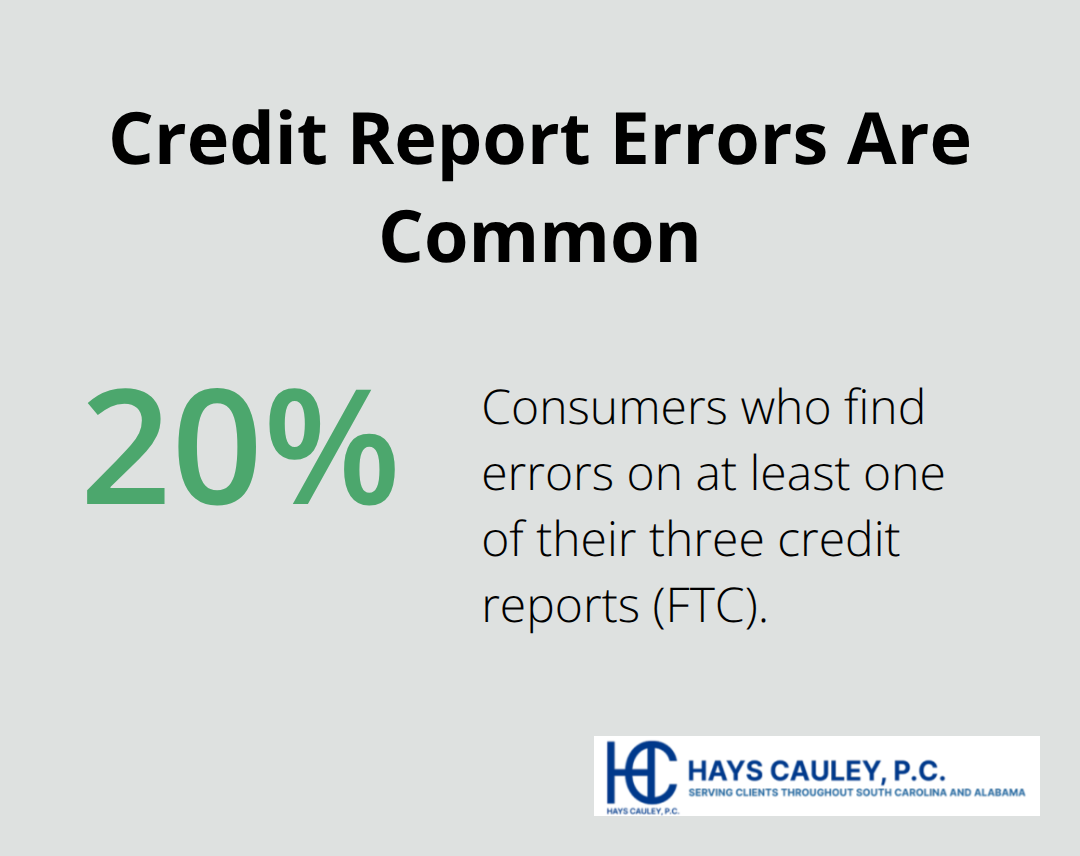

A mistake on your credit report can cost you tens of thousands of dollars over your lifetime. The Federal Trade Commission found that roughly 20% of consumers find errors on at least one of their three credit reports, yet most never take action to fix them. When inaccurate information stays on your file, lenders view you as a riskier borrower than you actually are.

A late payment that was never late, a closed account still showing as open, or a fraudulent account opened in your name-each of these errors damages your creditworthiness in the eyes of creditors.

How Your Score Determines Your Financial Future

Your credit score determines whether you qualify for loans, what interest rates you pay, and sometimes even whether you get hired for a job. Moving from a 650 credit score to a 750 score on a $200,000 mortgage could save you roughly $68,000 in interest over the life of the loan. That single 100-point improvement comes directly from correcting errors that never belonged on your report in the first place. Lenders deny credit applications based on false information, and employers reject candidates due to inaccurate reports.

Identity Theft Compounds the Damage

Inaccurate credit data also creates a pathway for identity theft to wreck your finances. When fraudulent accounts appear on your report, they tank your score while you remain unaware someone is borrowing in your name. South Carolina law recognizes this harm-under the state Consumer Protection Code Title 37, you can recover actual damages plus statutory damages up to $1,000 per violation, with treble damages possible for willful violations. Most people check their credit report once every few years, if at all, which means errors compound for months before discovery.

Your Legal Rights Protect You

The Fair Credit Reporting Act gives you the right to dispute errors, but only if you know they exist. You can recover financially from these mistakes, though the process requires action on your part. South Carolina residents in Greenville, Columbia, and Charleston who face credit reporting errors have legal protections available to them. Understanding what those protections are and how to use them is the first step toward fixing your report.

What the Fair Credit Reporting Act Actually Gives You

The FCRA Requires Bureaus to Investigate and Correct Errors

The Fair Credit Reporting Act is not a suggestion-it’s a federal law with teeth. Under the FCRA, credit reporting agencies must investigate disputed items within 30 days and provide you with written results. If they find an error, they must correct it and send updated reports to anyone who received your inaccurate file within the last six months. This matters because most people don’t realize they have this power. The CFPB maintains a Consumer Complaint Database where you can file formal complaints if a bureau refuses to fix verified mistakes, and those complaints get tracked and reported back to you with a tracking number.

Access Your Reports and Know What’s There

You have the right to know exactly what’s in your report. You can pull a free copy from each of the three major bureaus annually through AnnualCreditReport.com, or call 1-877-322-8228. South Carolina law goes further than federal protections: under the state Consumer Protection Code Title 37, you can sue for actual damages plus statutory damages of at least $1,000 per violation, and treble damages if the violation was willful. The statute of limitations is two years from discovery or five years from the violation, whichever comes first.

This means if you discover an error today that appeared three years ago, you still have legal recourse as long as you act within two years of finding it.

Creditors Must Verify Before They Report

Creditors furnishing information to bureaus must also follow rules. Before reporting negative information, they verify it’s accurate and belongs to you. When you dispute an item directly with a furnisher-the creditor or company reporting the information-they must investigate within 30 days. Many people skip this step and only dispute with the bureau, but going straight to the furnisher often works faster because they control the source data.

Build Your Case With Documentation and Certified Mail

Gather supporting documents first: statements, payment records, creditor letters, or police reports if identity theft is involved. Send your dispute via certified mail with return receipt so you have proof of delivery. The CFPB offers sample dispute letters on their website that show exactly how to structure your complaint. If a bureau or furnisher drags their feet or refuses to correct clear errors, legal action becomes your next option-and that’s when you need to understand what steps come next.

How to Spot and Fix Errors on Your Credit Report

Request Your Free Credit Reports

Start by pulling your actual credit reports from all three bureaus through AnnualCreditReport.com or by calling 1-877-322-8228. Most South Carolina residents rotate checking one bureau every four months rather than pulling all three at once, which spreads out your free annual pulls and gives you continuous monitoring throughout the year. This approach costs nothing and takes about 15 minutes per bureau.

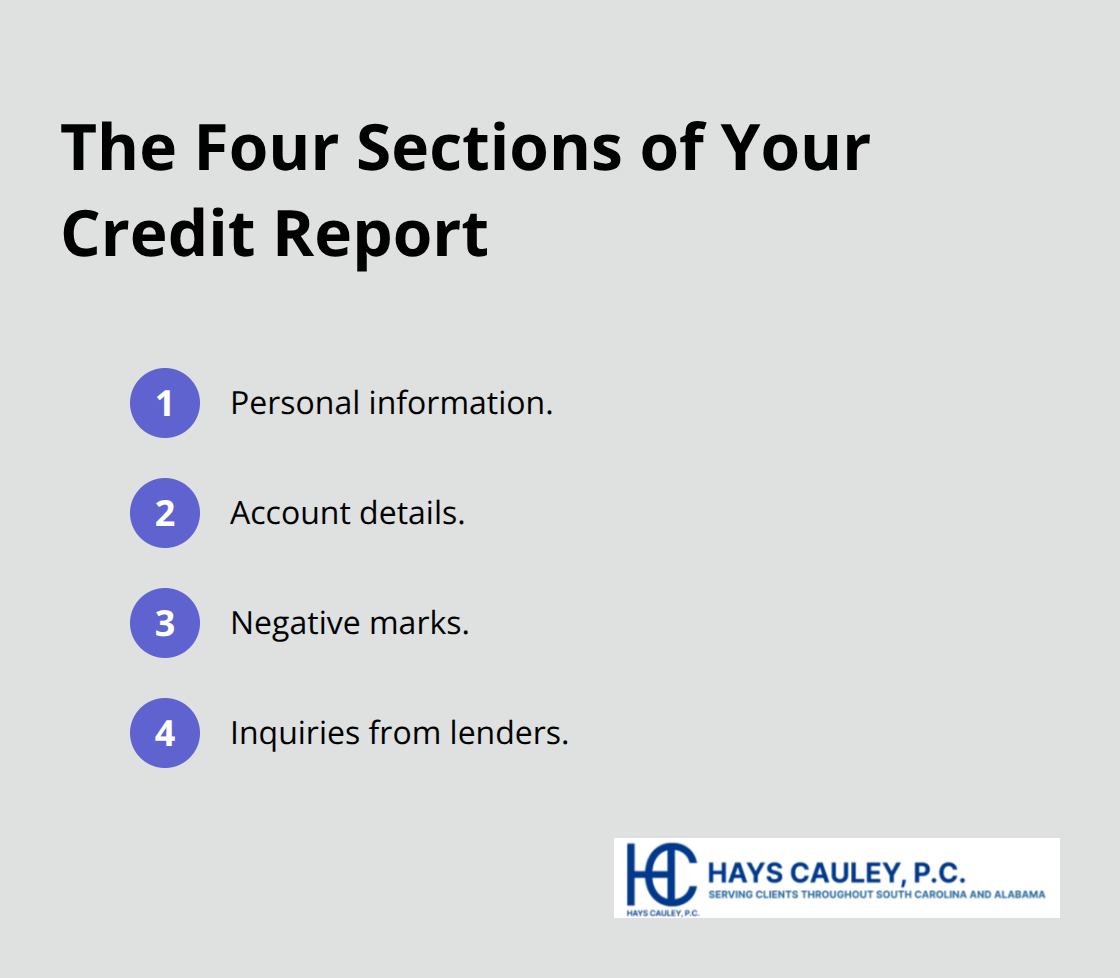

Review All Four Sections of Your Report

Your credit report contains four distinct sections: personal information at the top, followed by account details, negative marks like late payments or collections, and finally inquiries from lenders. The Federal Trade Commission estimates that about 20% of consumers find errors on at least one of their three reports, so approach this review with the expectation that you’ll likely find something that needs correction.

Start with personal information for identity errors like a wrong name, phone number, or address. Look for mixed files where accounts belonging to another person with a similar name appear in your file, which happens more often than you’d think. Then move to account details: verify that a closed account isn’t mistakenly showing as open, confirm whether you’re listed as the owner or merely an authorized user, and check that balances and credit limits match your records.

Identify Inaccurate Dates and Duplicate Items

Incorrect dates cause real damage to your score, so confirm the last payment date, date opened, and date of first delinquency for any negative items. Watch for duplicate debt items reported more than once under different names, which is surprisingly common and easy to fix once you spot it. These duplicates artificially lower your score and make your financial situation appear worse than it actually is.

File Your Dispute and Track the Investigation

Once you identify an error, gather supporting documents immediately: statements, payment records, creditor letters, or police reports if identity theft is involved. Send your dispute via certified mail with return receipt to both the credit reporting agency and the furnisher (the creditor reporting the information). The CFPB offers sample dispute letters on their website that show exactly how to structure your complaint, and using their template increases your chances of a successful investigation.

Credit bureaus must reinvestigate within 30 days and notify you of results in writing. If they find an error, corrected reports must be sent to recipients who received your inaccurate file in the last six months. After submitting disputes, monitor for changes and request new copies to confirm corrections took effect across all three bureaus.

Escalate if Bureaus Refuse to Correct Errors

If a bureau refuses to correct a verified mistake after 30 days, you can file a complaint with the CFPB, which forwards your issue to the company and provides a tracking number so you can monitor progress. If disputes stall or bureaus refuse to fix clear errors, a consumer protection attorney can help you enforce your rights under the Fair Credit Reporting Act and state law. The statute of limitations is two years from discovery or five years from the violation, so acting promptly preserves your legal options.

Final Thoughts

Inaccurate credit reports damage your score, tank your loan prospects, and create openings for identity theft to wreak havoc on your finances. You now understand what errors look like, how to access your reports for free, and what steps you must take when you spot mistakes. The Fair Credit Reporting Act protects your right to dispute inaccurate information, and South Carolina law backs those protections with statutory damages and attorney’s fees if legal action becomes necessary.

Pull your three credit reports today through AnnualCreditReport.com or call 1-877-322-8228 to start your review. Spend time examining each report for identity errors, incorrect account details, wrong dates, and fraudulent accounts that don’t belong to you. Send certified dispute letters to both the credit bureau and the furnisher when you find errors, then monitor the 30-day investigation period closely and follow up if corrections fail to appear.

Correcting even one error often raises your credit score by 50 points or more, which translates into lower interest rates and better loan terms on major purchases. If bureaus refuse to correct verified mistakes or identity theft has damaged your file, we at Hays Cauley, P.C. help South Carolina residents in Greenville, Columbia, and Charleston enforce their FCRA data accuracy rights and hold credit bureaus accountable. Contact us today to discuss your situation and explore your legal options.